Arthur Hayes' new article: The Fed's policy shift signal is showing. Can Bitcoin exceed $250,000 by the end of the year?

Reprinted from panewslab

04/01/2025·28D

Original text:Arthur Hayes

Compiled by: Yuliya, PANews

Within the global central bank circle, Jerome Powell and Haruhiko Kuroda have established a deep friendship. Since Kuroda Haruhiko stepped down as president of the Bank of Japan (BOJ) a few years ago, Powell has often sought advice or chatted with him. Powell's meeting with new U.S. Treasury Secretary Scott Bescent had plagued him in early March. This meeting left a psychological shadow on him, prompting him to seek a partner to express his feelings. You can imagine:

During a conversation, Powell confides his troubles to Kuroda. Through the conversation, Kuroda recommended to him the "Jung Center" that specializes in serving the central bank's governor. This institution originated from the Deutsche Imperial Banking era and was founded by the famous psychologist Carl Jung, aiming to help top central bankers cope with the pressure. After World War II, the service expanded to London, Paris, Tokyo and New York.

The next day, Powell came to the office of Justin, a psychologist at 740 Park Avenue. Here, he experienced an in-depth psychological counseling. Justin keenly realized that Powell was facing a dilemma of "financial domination". During the consultation, Powell revealed his humiliating experience when he met with Treasury Secretary Becent, a experience that severely hit his self-esteem as the chairman of the Federal Reserve.

Justin comforted him that this was not the first time. She suggested that Powell read Arthur Burns’ speech The Dilemma of the Central Bank to help him understand and accept the situation.

Fed Chairman Powell hinted in his latest meeting in March that quantitative easing (QE) may soon resume, with the focus on the U.S. Treasury market. This statement marks a major change in the global dollar liquidity pattern. Powell has drawn a possible path for this, and the policy shift is expected to begin as early as this summer. Meanwhile, while the market is still discussing the pros and cons of tariff policies, this could be good news for the cryptocurrency market.

This article will focus on the political, mathematical and philosophical reasons for Powell’s concessions. First, we will discuss President Trump's consistent campaign commitment and why this mathematically requires the Federal Reserve and the U.S. commercial banking system to print money to buy Treasury bonds. Then, it will be discussed why the Fed never had a chance to maintain sufficiently tight monetary conditions to reduce inflation.

The promise has been made and will be fulfilled

Recently, macroeconomic analysts have discussed Trump's policy intentions. Some believe that Trump may adopt a radical strategy and will not adjust until the approval rating falls below 30%, while others believe that Trump's goal in his last term is to reshape the world order and rectify the financial, political and military system of the United States. In short, he is willing to tolerate significant economic pain and plunge in support to achieve what he believes is good for the United States.

However, for investors, the key is to abandon the subjective judgment of the policy's "right or wrong" and instead focus on probability and mathematical models. Portfolio performance depends more on changes in fiat currency liquidity around the world than on the strength of the United States compared to other countries. Therefore, instead of trying to guess Trump's policy tendencies, it is better to focus on relevant data charts and mathematical relationships to better grasp market trends.

Since 2016, Trump has continued to emphasize that the United States has experienced unfair treatment over the past few decades because of its trading partners. Although there is controversy over its policy implementation, its core intentions have not changed. As for the Democratic Party, although its statements on adjusting the global order are not as strong as Trump, it basically agrees with this direction. During his tenure as U.S. President, Biden continued Trump's policy of restricting China's access to semiconductors and other key areas of the U.S. market. Vice President Kamala Harris also used tough rhetoric toward China in his previous presidential campaign. Although there may be differences between the two parties on the rhythm and depth of specific implementation, they have a consistent position on promoting changes to this point.

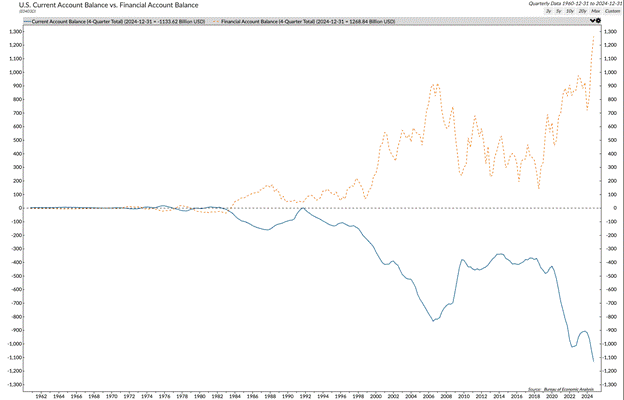

The blue line represents the U.S. current account balance, which is basically the trade balance. It can be seen that since the mid-1990s, the United States imported far more goods than exports, and this trend accelerated after 2000. What happened during this period? The answer is China's rise.

In 1994, China depreciated significantly and began its journey as a mercantilist export power. In 2001, US President Bill Clinton allowed China to join the World Trade Organization, significantly reducing tariffs on Chinese exports to the United States. As a result, the US manufacturing base was transferred to China, and history changed.

Trump’s supporters are those who have been negatively affected by the relocation of American manufacturing. These people do not have college degrees, live in the interior of the United States, and have few financial assets. Hillary Clinton calls them "deplorables". Vice President JD Vance affectionately called them and themselves "hillbillies".

The orange dotted lines and the upper panel in the chart are the balance of US financial accounts. As can be seen, it is almost a mirror of the current account balance. China and other exporters can continue to accumulate huge trade surpluses because when they make dollars by selling goods to the United States, they do not invest these dollars back home. Doing so means they have to sell US dollars to buy their own currency such as RMB, causing their own currency to appreciate, thereby increasing the price of exported goods. Instead, they use these dollars to buy U.S. Treasury bonds and U.S. stocks. This allows the United States to maintain a massive deficit without disrupting the Treasury market and have the best-performing stock market in the world over the past few decades.

The yield on the 10-year U.S. Treasury bonds fell slightly, while the total outstanding debt (yellow) increased by 7 times over the same period.

Since 2009, the MSCI U.S. Index (white) has performed 200% more than the MSCI Global Index (yellow).

Trump believes that by bringing manufacturing jobs back to the United States, he can provide good jobs for about 65% of the population without a college degree, strengthen military strength (as weapons, etc. will be produced in sufficient quantities to deal with equal or near equivalent opponents), and bring economic growth above trend levels, such as reaching 3% real GDP growth.

There are some obvious problems with this plan:

-

First, if China and other countries do not have the US dollar to support the Treasury bonds and stock markets, prices will fall. U.S. Treasury Secretary Scott Bessett needs buyers to buy the huge debt that must be rolled out and the ongoing federal deficit in the future. His plan is to reduce the deficit from about 7% to 3% by 2028.

-

The second problem is that the capital gains tax brought about by the rise in the stock market is the government's marginal income driver. When the rich cannot make money through stock trading, the deficit will increase. Trump’s campaign platform is not to stop military spending or cut benefits such as health care and social security, but to grow and eliminate fraudulent spending. So he needs capital gains tax revenue, although the wealthy who own all the stocks, on average, they didn't vote for him in 2024.

The mathematical dilemma of debt growth and economic growth

Assuming Trump successfully reduces the deficit from 7% to 3% by 2028, the administration remains a net borrower year after year and cannot repay any existing debt stocks. From a mathematical point of view, this means interest payments will continue to grow exponentially.

This sounds bad, but the United States can mathematically get rid of problems with growth and deleverage its balance sheet. If real GDP growth is 3%, long-term inflation is 2% (although unlikely), which means nominal GDP growth is 5%. If the government issues debt at a rate of 3% of GDP, but the economy has a nominal growth rate of 5%, then mathematically, the debt-to-GDP ratio will decline over time. But one key factor is missing here: what interest rates can the government use to raise funds for itself?

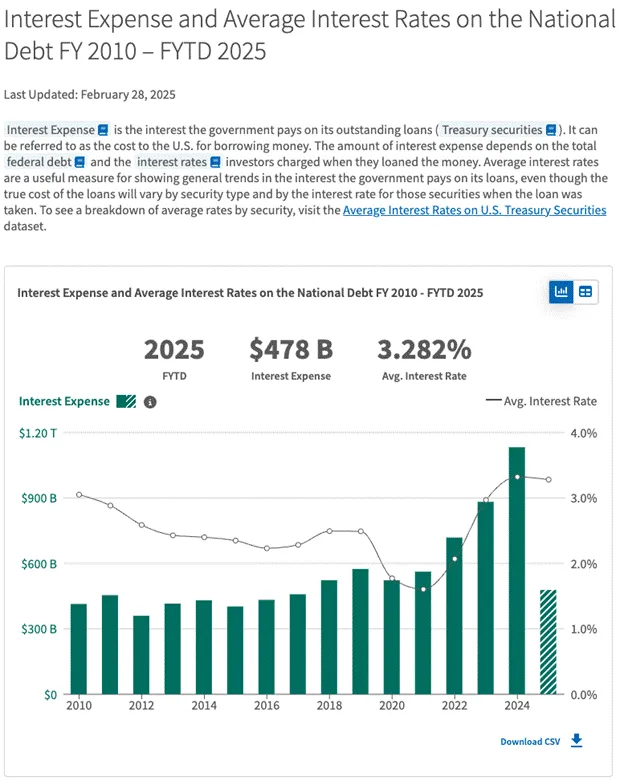

In theory, if the U.S. economy is nominally growing by 5%, Treasury investors should demand at least a 5% return. But this will significantly increase interest costs, as the Treasury currently pays a weighted average rate of 3.282% on its approximately $36 trillion (and growing) debt.

Unless Bessett can find buyers who buy Treasury bonds at unreasonably high prices or low yields, mathematical calculations cannot be true. As Trump is busy reshaping the global financial and trade system, China and other exporters cannot and will not buy government bonds. Neither will, private investors, because the yield is too low. Only commercial banks and the Fed have the firepower to buy debt at levels that the government can afford.

The Fed can print money to buy bonds, which is called quantitative easing (QE). Banks can print money to buy bonds, which is called partial reserve banking business. However, the actual operation is not that simple.

The Fed is ostensibly busy with its unrealistic tasks, about to be manipulated and false inflation indicators down to below their fictitious 2% target. They are removing currency/credit from the system by shrinking their balance sheets, which is called quantitative austerity (QT). As banks performed extremely poorly in the 2008 Global Financial Crisis (GFC), regulators required them to pledge more owned capital on the Treasury bonds they purchased, called supplemental leverage ratio (SLR). Therefore, banks cannot use unlimited leverage to provide financing to the government.

However, changing this situation and turning the Fed and banks into inelastic buyers of Treasury bonds is very simple. The Fed can decide to end the quantitative tightening at least to restart QE. The Fed can also exempt banks from SLR compliance, allowing them to use unlimited leverage to buy Treasury bonds.

The question becomes why would Jerome Powell-led Fed help Trump achieve his policy goals? The Fed significantly helped Harris' campaign by cutting interest rates by 0.5% in September 2024, and after Trump's victory, he showed a stubborn requirement to increase the amount of currency to lower long-term Treasury yields. To understand why Powell ended up doing what the government asked him to do, perhaps it was back to the historical background of 1979.

The chairman who was overturned

Now, Powell is in a very awkward position, watching the dominant force of fiscal policy undermine the Fed's credibility in fighting inflation.

Simply put, when government debt is too large, the Fed has to give up independence and finance the government at low interest rates instead of really fighting inflation.

This is not a new problem. Former Federal Reserve Chairman Burns encountered a similar situation in the 1970s. In his 1979 speech, The Pain of the Central Bank, he explained why central banks struggle to control inflation:

" Since the 1930s, political and philosophical trends in the United States and elsewhere have changed economic life and created a sustained tendency to inflation."

Simply put: politicians asked me to do this.

Burns pointed out that the government has become increasingly active in the economy, not only relieving suffering, but also subsidizing "value" activities and limiting "harmful" competition. Despite the growth of national wealth, American society was unrest in the 1960s. Groups such as ethnic minorities, poor, elderly, and disabled people feel unfair, and middle-class young people have begun to reject existing systems and cultural values. At that time, as now, "prosperity" was not distributed evenly, and people asked the government to solve this problem.

Government actions and people's needs interact and are constantly escalating. When the government began to address "unfinished tasks" such as reducing unemployment and eliminating poverty in the mid-1960s, it awakened new expectations and needs.

Now, Powell faces a similar dilemma, wanting to be a tough anti-inflation hero like Volcker, but may actually be forced to succumb to political pressure like Burns.

The history of the government's direct intervention in trying to solve the problem of key voter groups can be traced back decades. The actual effects of this intervention often vary from situation to situation and the results are different.

Many of the results of active participation in the interaction between government and citizens have indeed had a positive impact. However, the cumulative effect of these actions injected a strong inflationary tendency into the U.S. economy. The surge in government programs has led to a gradual increase in tax burdens for individuals and businesses. Even so, the government's willingness to tax is significantly lower than its tendency to spend.

Society has generally formed a consensus: solving problems is the responsibility of the government. The main way for the government to solve the problem is to increase spending, which deeply embedded inflation factors into the economic system.

In fact, the expansion of government spending is largely driven by commitment to full employment. Inflation has gradually been widely seen as a temporary phenomenon—or as long as it remains mild, it is considered an acceptable state.

Fed's inflation tolerance and policy contradiction

Why does the Fed tolerate 2% inflation per year? Why does the Fed use the term "temporary" inflation? A 2% inflation compounded over 30 years will result in an 82% increase in price levels. But if the unemployment rate rises by 1%, the sky will collapse. These things are worth thinking about.

Theoretically, the Fed system has the ability to stifle inflation at the beginning of its germination, or end inflation at any point afterwards. It could have restricted money supply, created enough tension in the financial and industrial markets, and quickly ended inflation. However, the Fed did not take such action, because it itself was influenced by philosophical and political trends that changed American life and culture.

The Fed is ostensibly independent, but as a government agency that is philosophically inclined to solve a wide range of social problems, it neither does nor can it stop inflation requiring intervention. The Fed has actually become a cooperator, in the process, creating the inflation it should have controlled.

Faced with political reality, the Fed did adopt austerity monetary policy at some point—such as in 1966, 1969 and 1974—but its restrictive position was not long enough to completely end inflation. Overall, monetary policy began to be dominated by the principle of "low nourishing the inflation process while still adapting to most of the market pressures."

This is exactly the path Powell took to monetary policy during his current Fed chairmanship. This reflects the so-called "financial dominance" phenomenon. The Fed will take necessary measures to provide financial support to the government. The pros and cons of policy goals can have different opinions, but Burns’ message is clear: When a person becomes the chairman of the Federal Reserve, he implicitly agrees to do whatever is necessary to ensure that the government can finance itself at an affordable level.

Current policy shift

Powell showed signs that the Fed continues to succumb to political pressure at a recent Fed press conference. He has to explain why the pace of quantitative tightening (QT) should be slowed down while the U.S. economy is strong and monetary conditions are loose. The current unemployment rate is at a low level, stocks are at an all-time high, and inflation remains above the 2% target, which should support a tighter monetary policy.

"The Fed said on Wednesday that it will slow down its balance sheet shrinking starting next month as government borrowing limits issues remain unresolved, and the shift could continue for the rest of the process," Reuters reported.

Although former Fed Chairman Paul Volcker is known for his strict monetary policy, he chose to relax his policies in the summer of 1982 when facing recession and political pressure, according to historical Fed archives. At that time, U.S. House Majority Leader James C. Wright Jr. met with Volcker several times to try to understand the impact of high interest rates on the economy, but did not see significant results. However, by July 1982, data showed that the recession had bottomed out. Volcker then told members of Congress that he would abandon the previously set monetary policy targets and predict a "highly likely" recovery in the second half of the year. This decision also echoes the long-standing recovery expectations of the Reagan administration. It is worth noting that although Volcker is regarded as one of the most respected Fed chairs, he has also failed to completely withstand political pressure. At that time, the debt situation of the US government was far better than the current one, and the proportion of debt to GDP was only 30%, but now it is as high as 130%.

Financially dominant evidence

Powell proved last week that fiscal dominance still exists. Therefore, the QT for Treasury bonds will be stopped in the short- to medium-term period. Going further, Powell said that while the Fed may maintain a natural reduction in mortgage-backed securities, it will buy Treasury bonds in net. Mathematically, this keeps the Fed's balance sheet constant; however, this is actually quantitative easing for Treasury bonds. Once officially announced, the price of Bitcoin will rise sharply .

In addition, the Fed will provide SLR exemptions to banks due to requirements from banks and the Treasury Department, another form of quantitative easing for Treasury bonds. The ultimate reason is that the above mathematical calculations would not work otherwise, and Powell could not stand by and let the US government fall into trouble even if he hated Trump.

Powell mentioned the balance sheet adjustment plan at a FOMC press conference on March 19 . He said the Fed will stop the reduction of its net assets at some point, but no relevant decision has been made yet. At the same time, he stressed his hope that MBS (mortgage-backed securities) can be gradually withdrawn from the Federal Reserve's balance sheet in the future. However, he also mentioned that the Fed may let MBS mature naturally while keeping the overall balance sheet size unchanged. The specific time and method of these adjustments have not yet been determined.

Treasury Secretary Bescent said in a recent podcast about Supplementary Leverage (SLR) that if SLR is removed, this policy could become a constraint for banks and could cause U.S. Treasury yields to fall by 30 to 70 basis points. He noted that each basis point change is equivalent to an economic impact of about $1 billion per year.

In addition, Federal Reserve Chairman Powell said at a press conference after the Federal Open Market Committee (FOMC) meeting in March that he believes that the inflationary effect may be "temporary" in response to the possible inflationary impact of tariff policies proposed by the Trump administration. He believes that while tariffs may trigger inflation, the impact is not expected to last too long. This judgment on "temporary" inflation gives the Federal Reserve still room to continue to adopt a loose policy when facing inflation caused by tariff hikes. Powell pointed out that the current benchmark view is that the driving effect of tariffs on prices will not last long , but he also stressed that there is still uncertainty in the future. Analysts believe that this statement means that the impact of tariffs on asset prices may be weakening, especially those that rely solely on statutory liquidity.

Federal Reserve Chairman Powell said at the FOMC meeting in March that the inflationary effect triggered by tariffs could be "short-term". He believes that this "temporary" inflation expectation allows the Federal Reserve to continue to implement loose policies even if inflation rises sharply due to tariffs.

At the post-conference press conference, Powell stressed that the current basic expectation is that the price increase caused by tariffs will be temporary, but he also added, "We cannot determine the specific situation in the future." Market analysts pointed out that the impact of tariffs may have gradually weakened for assets that rely on fiat liquidity.

In addition, the "liberation day" announced by Trump on April 2 and the potential tariff increase did not seem to have a significant impact on market expectations.

US dollar liquidity calculation

What is important is forward-looking changes in US dollar liquidity relative to previous expectations.

-

Previous pace of quantitative bond tightening (QT) : $25 billion per month

-

After April 1, the pace of Treasury bond QT : $5 billion per month

-

Net effect : positive change in USD liquidity annualized USD 240 billion

-

The effect of QT reversal : up to $35 billion in MBS reduction per month

-

If the Fed 's balance sheet remains unchanged, you can buy : up to $35 billion per month Treasury bonds or $420 billion annualized

Starting April 1, an additional $240 billion in relative dollar liquidity will be created. In the near future, at the latest in the third quarter of this year, the $240 billion will rise to an annualized $420 billion. Once quantitative easing begins, it won’t stop for a long time; it will increase as the economy needs more money printing to maintain the status quo.

How the Ministry of Finance manages its general account (TGA) is also an important factor affecting US dollar liquidity. TGA is currently about $360 billion, down from about $750 billion at the beginning of the year. TGA is used to maintain government spending due to debt ceiling constraints.

Traditionally, once the debt ceiling is raised, the TGA is refilled, which negatively affects the liquidity of the dollar. However, maintaining an excessively high cash balance is not always economically reasonable; the target TGA balance was set at $850 billion during the term of former Treasury Secretary Yellen.

Given that the Fed can provide liquidity support as needed, the Treasury Department may adopt a more flexible TGA management strategy. Analysts expect the Treasury Department may not significantly increase TGA targets relative to current levels in the quarterly refinancing announcement (QRA) in early May. This will alleviate the possible negative dollar liquidity shocks after the debt ceiling is raised, providing a more stable environment for the market.

2008 Financial Crisis Case Study

During the 2008 Global Financial Crisis (GFC), gold and S&P 500 showed different responses in the face of increased fiat currency liquidity. As an anti-establishment commodity financial asset, gold reacts faster when liquidity is injected, while the S&P 500 relies on legal support from the state system, so it may react slowly when the solvency of the economic system is questioned. Data shows that gold outperformed the S&P 500 during the worst stages of the crisis and subsequent recovery periods. This case study shows that even if the current US dollar liquidity has increased significantly, the negative economic environment may still have an adverse impact on the price trends of Bitcoin and cryptocurrencies.

On October 3, 2008, the U.S. government announced the launch of the "Problem Asset Relief Program" (TARP) to deal with market turmoil caused by Lehman Brothers' bankruptcy. However, the plan failed to stop the continued decline in financial markets, with both gold and U.S. stocks falling. Subsequently, Federal Reserve Chairman Ben Bernanke announced the launch of a large-scale asset purchase plan (that is, later quantitative easing policy QE1). Affected by this, gold began to rebound, while US stocks continued to fall, and it did not bottom out and rebounded until the Federal Reserve officially launched the money printing operation in March 2009. As of early 2010, gold prices rose 30% compared with Lehman Brothers when they went bankrupt, while U.S. stocks rose only 1% during the same period.

Bitcoin Value Equation

Bitcoin did not exist in the 2008 financial crisis, but now it has become an important financial asset. The value of Bitcoin can be simplified to:

Bitcoin Value = Technology + Fiat currency liquidity

Bitcoin’s technology works well, with no major changes in the near future, for better or worse. Therefore, Bitcoin trading is based entirely on the market's expectations for future fiat currency supply. If the analysis of the Fed's major shift from quantitative tightening to quantitative easing in Treasury bonds is correct, Bitcoin hit a local low of $76,500 last month and will begin to climb towards its year-end target of $250,000. Although this prediction is not an accurate scientific conclusion, referring to gold's performance patterns in similar circumstances, Bitcoin is more likely to hit $110,000 first rather than falling $76,500 again. Even if the U.S. stock market continues to fall due to tariff policies, corporate earnings expectations collapse or weaker foreign demand, Bitcoin still has a high possibility of continuing to rise. Investors should deploy funds with caution, not use leverage, and purchase small positions relative to the total size of the portfolio.

However, Bitcoin is still likely to reach $250,000 by the end of the year, an optimistic expectation based on multiple factors, including the possibility that the Fed may drive the market by releasing liquidity and the possibility that the Chinese central bank will relax monetary policy to maintain the stability of the yuan against the dollar. In addition, European countries' increased military spending due to security concerns may be achieved through printing the euro, which may also indirectly stimulate market liquidity.