Deutsche Bank's full research report floods the screen: China's "Sputnik Moment"

Reprinted from jinse

02/06/2025·18DWritten by: 0xjs@Golden Finance

Deepseek, the technological breakthrough of "national fortune level" will continue to ferment, and the entire Chinese assets may need to be revaluated.

On February 5, 2025, Deutsche Bank published a research report called China eats the World, which flooded the investors. Deutsche Bank said that 2025 is a year for China to surpass other countries, and in 2025, China launched the world's first sixth-generation fighter and low-cost artificial intelligence system "DeepSeek" within a week. Marc Andreessens calls the launch of "DeepSeek" the "Sputnik Moment" of AI, but it is more like China's "Sputnik Moment", marking the recognition of China's intellectual property rights. The field where China performs outstandingly in the field of high value-added and dominates the supply chain is expanding at an unprecedented rate. China has companies that lead almost every industry, and as Chinese companies expand in the global market, China's valuation discount should turn into a premium at some point in the future. Investors must turn significantly to invest in Chinese stocks in the medium term, and Hong Kong/Chinese stocks will usher in a bull market in the medium term.

It is worth noting that the title of its research report borrows the famous quote from a16z founder Marc Andreessens: "Software is eating the world". The first part of the research report "This is China, not AI, 'Sputnik Moment'" is also Borrowing Marc Andreessens' recent comment on DeepSeek: "DeepSeek is AI's Sputnik moment".

The following is the full text of Deutsche Bank’s research report:

Original title: China eats the World

Author: Peter Milliken, CFA, Research Analyst

This is Chinese, not AI, "Sputnik Moment"

We believe 2025 is the year when the investment community realizes that China is surpassing the rest of the world. Nowadays, it is increasingly difficult for people to ignore the fact that Chinese companies are providing higher cost-effectiveness and often better quality in multiple manufacturing fields, even in the increasing number of service fields.

Investors pay the price to take dominance, and we expect the "China discount" to disappear. Furthermore, as policies tend toward consumption rather than production, and possibly due to financial liberalization, we believe that profitability is expected to exceed expectations throughout the cycle. We believe that the bull market for Hong Kong/China stocks began in 2024 and will surpass previous highs in the medium term.

China first emerged in the global dominance of clothing, textiles and toys. Subsequently, it dominated the fields of basic electronics, steel, shipbuilding, and more recently in white appliances, solar energy, and other less eye-catching fields.

China still dominates the complex industries such as telecommunications equipment, nuclear power, national defense and high-speed railways without warning. These technological achievements have not been valued by investors before.

But by the end of 2024, China has attracted attention for its rapid rise to become a global leader in automobile exports, with a large number of electric vehicles with advanced functions, attractive prices and lower prices than existing models pouring into the global market.

In 2025, China launched the world's first sixth-generation fighter and low- cost artificial intelligence system "DeepSeek" within a week.

Marc Andreessens calls the launch of "DeepSeek" the "Sputnik Moment" of AI, but it is more like China's "Sputnik Moment", marking the recognition of China's intellectual property rights. The field where China performs outstandingly in the field of high value-added and dominates the supply chain is expanding at an unprecedented rate.

We believe that global investors tend to significantly under-allocate Chinese assets, just as they avoided fossil fuels a few years ago until the market punishes investors who take non-market-oriented decisions. We see that the fund's exposure to China is now extremely small. Investors who prefer leading companies that have moats cannot ignore this: Chinese companies now have broad and deep moats, not Western companies that they consider economically superior.

China's manufacturing industry is obvious, with its commodity exports twice that of the United States. China contributes 30% of the world's manufacturing value added, and its share in the service industry is also increasing rapidly. People avoid China as an investment destination due to concerns about a weak economy, but despite a cyclical slowdown in China, China's growth rate is more than twice that of most developed markets.

With companies that lead almost every industry, China 's share of global market value is unlikely to remain in single digits for a long time. We believe that people are gradually realizing that China today is like Japan in the early 1980s, when Japanese companies were climbing the value chain, with higher product quality and continuous emergence of innovation. Many Western companies and industries may face potential survival crises, so their portfolios need to be readjusted to reflect this.

To survive, Western businesses will need to: 1) large-scale automation; and/or 2) set up trade barriers. In the past, the second road was a downhill for economies, and while this is happening, it doesn’t necessarily help the West. For example, in the automotive field, China's main export market is often about 7 billion people outside the G10 countries.

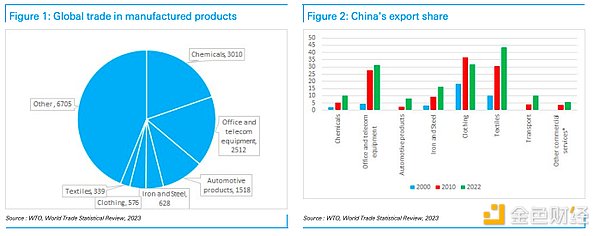

Figure 1: Global Trade in Manufacturing Products Figure 2: China's Export Share

Looking at the main categories of international trade, China is taking a share in all categories except clothing (which China dominated the field before expanding its business overseas). In key commodity categories, China is larger than the United States and is usually many times larger. The only exception is cars (value rather than quantity is mentioned here), but China is likely to be ahead as well - Ford CEO drives Xiaomi cars, it is hard to see that this trend will change. Even in the service industry, China is catching up, for example, in terms of transportation services, its share has increased by about 0.5 percentage points per year.

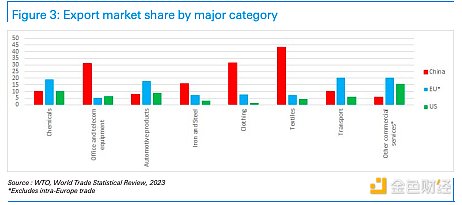

Figure 3: Main categories of export market share

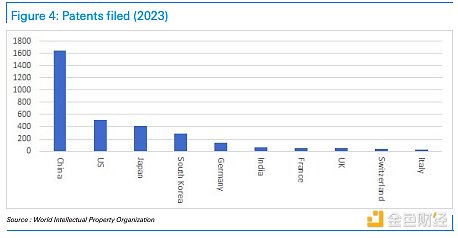

Patents as agent indicators for intellectual property rights

China has a complete value chain and forms a local professional cluster, has multiple Silicon Valley-like professional fields in key industries, and works closely with domestic universities in research.

In the electric vehicle field, China has about 70% of patents, and 5G and 6G telecommunications equipment fields are in a similar position.

In 2023, China 's patent applications accounted for nearly half of the world. This trend may continue as China has more science and engineering graduates than the rest of the world's total except India. In addition, it should be considered that many graduates from other countries are also Chinese. Therefore, unless special circumstances occur, the rise in Chinese business dominance is unlikely to be stopped in the short term.

China does face trade barriers, and the U.S. and the EU impose tariffs on electric vehicles is an obvious example, but the West is restricted when taking action because they need to consider the more serious consequences that may come with (such as inflation, decreased competitiveness and retaliation) ). In the 1980s, the United States tried to curb Japan's development and achieved some results, but we believe that China's current situation is not Japan in 1989, but more like Japan in previous years.

Figure 4: Number of patent applications in 2023

China vs. Japan in the 1980s

Throughout the 1970s, Japan ranked second in the world in terms of GDP (GNP), second only to the United States. After checking Wikipedia, we were surprised to find that Japan's actual GDP growth rate in the 1980s was only 4%, but this is still regarded as an important part of its economic "miracle". By contrast, people are anxious about whether China's economic growth rate is 4% or 5%, and think that growth is "slow", but in hindsight, this view may evolve into seeing it as a "miracle ”.

The Plaza Accord requires the yen to appreciate by 40%, slowing Japan's industrial leading edge. This led to an economic slowdown, and the Japanese government responded through loose monetary policies. From 1987 to 1989, economic growth recovered to 5%, and during this period the stock market rose strongly and a bubble appeared. The rebound in economic growth has driven the recovery of the steel and construction industries, raising wages and increasing employment. In the late 1980s, domestic demand rather than exports became the driving force for economic growth. This situation can also happen in China.

Japan in the 1980s

According to Wikipedia, Japan's economic growth is achieved through the investment of large amounts of cheap labor, the intensive use of capital and the increase in productivity. Domestic investment accounts for more than 30% of GDP, and financial suppression keeps interest rates at a low level, which has promoted investment. Japan acquires new technology through joint ventures. In the early 1970s, Japan's savings rate reached 40% of GDP and dropped to nearly 30% by the early 1980s. In the 1970s, Japan began to set up factories overseas to avoid trade frictions. And China has only recently begun to take similar measures.

The question is: What stage is China in this development path? Like Japan, China has also experienced a real estate bubble, but the degree is far less than that of Japan. In addition, it has been six years since the tightening of self-confidence credit and the real estate industry began to decline. House prices have fallen by one-third, mortgage rates have dropped by half, and nominal GDP has grown by about one-third, so affordability for home purchases has returned to levels not seen in years. Stock market valuations are also at low levels due to lower profit margins and lower P/E multiples. So, this is not Japan, which was in a bubble in 1989 (at that time, the market value of Japanese stocks increased 50 times in the past 20 years).

It is generally believed that China will not embark on the economic development path dominated by consumption like Japan, and will only fall into an economic downturn like Japan. But in fact, China is walking a path that the United States, Japan, Singapore, Hong Kong, Taiwan, South Korea, Spain and many Eastern European countries and regions have taken. Some other countries and regions are struggling with the middle-income trap, but unlike them, China has become a leader in global manufacturing and increasingly service industries.

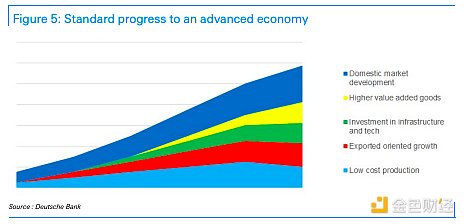

Figure 5: Standard Process toward Advanced Economy

At around this time, Japan achieved liberalization of its financial

system

In Chapter 12 of the 2013 International Monetary Fund report, "China's Economic Transformation", it was mentioned that Japan in the 1980s had similarities with China's future development path. Before the Plaza Accord, Japan's financial system was highly regulated, interest rates were regulated, and capital controls were strict. Due to the abundant capital of enterprises, the demand for bank credit was limited. Japanese investors hold a large amount of US assets, coupled with the depreciation of the yen, prompted the outside world to call on Japan to open up its financial markets and increase the attractiveness of yen-denominated assets. This in turn led to capital flows into Japan and increased money supply, which drove economic growth and asset bubbles.

China may be moving in a similar direction. President Trump may follow President Reagan's approach to promote China's financial liberalization in the trade deal, and China may also be ready to accelerate the process of internationalization of the RMB. We think this is good news for the stock market, as the yuan may depreciate, which will enhance the profitability of companies and the attractiveness of Chinese assets from a foreign exchange perspective. Why does the United States push this? Reasons may include: 1) political considerations for reaching an agreement; 2) believe that the depreciation of the RMB can offset the impact of tariffs, allowing trade to continue and impose tariffs, rather than excluding trade; 3) believe that financial liberalization will make the RMB appreciate, This will weaken China's competitiveness.

Regardless of external pressures, if China wants to promote consumption, liberalization of the financial system will help, ending the transfer of wealth from depositors to businesses by normalizing interest rates. This will reduce excessive investment and vicious competition, as capital will be allocated reasonably, which will help improve corporate profitability and alleviate fiscal pressures, as the returns of state-owned enterprises will increase. We expect large enterprises, investment companies and households to increasingly pressure the government to ease vicious competition to enhance stock market value. Just as the government has previously slowed down overinvestment in infrastructure and real estate, curbing overinvestment in industry will obviously be the next step, and may come faster than expected. We expect this to be a key topic in 2025, which will both appease the United States and the situation requires, and we expect this to drive a big bull market.

But what impact does China's population decline have?

China 's decline in population poses a drag on economic growth, but many countries are facing this problem. We think this completely ignores an important fact that China has two advantages: 1) automation is leading, and about 70% of the world's industrial robots are installed in China, which brings productivity advantages, thereby increasing per capita wealth; 2) has a huge Potential markets, the Belt and Road Initiative brings Central Asia, West Asia, the Middle East and North Africa into its development track, expanding its market potential.

Although Central Asia has a population of only 80 million, it is rich in resources; West Asia has a population of 310 million, which is generally relatively wealthy. South Asia has 2.1 billion people (although two-thirds of them are in India, which is currently largely restricting trade and investment with China, but this may change in the medium term). There is also Africa, with a population of 1.4 billion. In other words, the potential consumer population in Africa is comparable to that in China, and the potential consumer population in Central Asia, West Asia and South Asia (excluding India) is comparable to that in ASEAN and Latin America. If China-India relations improve, the potential consumer population in India will also be Will become a huge market. Therefore, focusing only on China's domestic population may lead to misconclusions about China's future.

In 2024, China's exports grew by 7%, exports to Brazil, the UAE and Saudi Arabia increased by 23%, 19% and 18% respectively, and exports to ASEAN countries along the Belt and Road Initiative increased by 13%. At present, China's exports to ASEAN and BRICS countries+ have been equivalent to those to the United States and the European Union. In the past five years, the export market share to these destinations has increased by two percentage points per year. Even in Latin America, China is rapidly expanding its market. Therefore, although the United States imposes high tariffs, it will harm China, Deutsche Bank's economic team believes that if the United States imposes 10% tariffs in the first and second half of the year respectively, given that US exports account for 3% of China's GDP, this will It brings downward pressure of 0.5% to China's GDP, which is a controllable impact.

The disadvantage of China's export dominance is that many major countries in the world have adopted protectionist measures even within the BRICS countries, so China's export growth is restricted to a certain extent. However, due to its advantages in intellectual property rights and manufacturing added value, Chinese companies are likely to expand their influence in the international market by setting up factories in other markets or assembling parts in exported to the assembly. The weaponization of the US dollar makes investing in overseas infrastructure and factories more attractive than investing in US Treasury bonds, so the future development direction is quite clear.

Figure 6: China expands its new economy market (unit: millions of people )

Figure 6: China expands its new economy market (unit: millions of people )

Sino-US trade issues may lead to unexpected benefits

The market generally expects that the US tariff levels on China are higher than Deutsche Bank’s expectations (we expect 20% tariffs to be implemented in two steps in 2025, one of which has been announced). But the reality may be much more optimistic than this pessimistic expectation.

The Trump administration is clearly keen on tariffs as a source of fiscal revenue and regards China as its main source of tariff revenue for economic and strategic reasons. However, President Trump seems to place more emphasis on tactical victory, perhaps more than ideological stances that are difficult to gain support. In our industry, there are investors and traders. In recent years, traders' influence has grown increasingly. Perhaps President Trump is more like a political "trader" than an "investor" who sticks to his ideology. If so, he is expected to strictly set the stop loss point.

The emergence of "DeepSeek" breaks the West's fantasy that it can curb China. The United States is best to stimulate business development by reducing regulation, providing cheap energy, and reducing import barriers to intermediate products that cannot be produced domestically. The last point may take longer to come true, but we expect internal demands from the U.S. House of Representatives, Senate members, and business leaders to push the U.S. to return to the traditional Republican stance on trade issues. This may require some recurring negotiations, but this analyst expects a more trade-oriented stance to eventually become part of the “America First” agenda before the midterm elections.

We believe that a political “trader” will seek to lock in results as soon as possible, so it may reach a Sino-US trade agreement in the first half of 2025 and then turn its focus to Western Hemisphere affairs. A fast-resolved agreement could include limited tariffs (as expected by Deutsche Bank), lifting some existing restrictions, and some large contracts between Chinese and American companies. If this happens (which this analyst thinks will), Chinese stock market is expected to rise.

Trade and market conditions are not closely related

Historically, trade and economic strength have been complementary. Therefore, we were surprised to find that few studies link exports to stock market performance. However, China's exports are closely related to the growth of global money supply, which has been rising but are currently slowing down. When we prompted Deutsche Bank's AI platform to look for related research, it told us: "Some studies show that export growth can increase corporate earnings, thereby increasing stock valuations... (but) some studies also show that just focusing on export growth is sometimes It could be at the expense of domestic demand, which could hinder overall economic growth and thus negatively impact the stock market.”

Therefore, paradoxically, the decline in exports may actually drive stock markets up over a period of time. China's rise in various industries is accompanied by excessive investment in many areas. In the solar sector, efforts are currently being made to cut supply, and if other industries follow suit, this may be good news for the stock market and may also release some funds for domestic consumption.

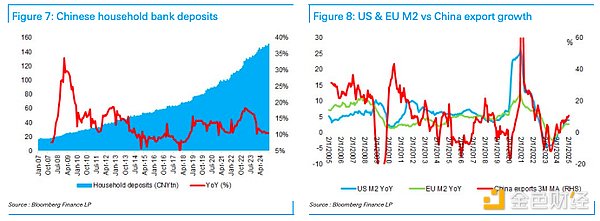

China's household deposit growth has slowed to twice the rate of nominal GDP, but since 2020, Chinese household savings have increased by $10 trillion, and we expect that this savings will be heavily used in consumption and investment in the stock market in the medium term. Therefore, Hong Kong/China stocks have a lot of room for growth in terms of accelerated earnings growth and price-to- earnings ratio revaluation.

Figure 7: Chinese household bank deposits Figure 8: Comparison of US and EU M2 export growth with China

Value market leaders

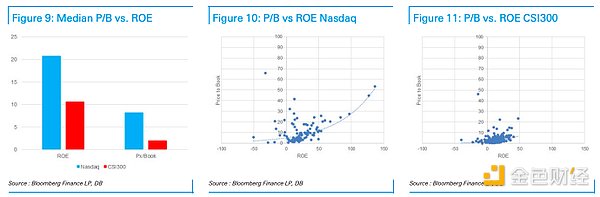

Figure 9: Comparison of median price-to-book ratio and return on equity Figure 10: Comparison of Nasdaq price-to-book ratio and return on equity Figure 11: Comparison of 300 price-to-book ratio and return on equity in Shanghai and Shenzhen 300 price-to-book ratio and return on equity in Shanghai and Shenzhen 300 price-to-book ratio and return on equity

The problem with investing in the tech industry is that profits are often concentrated in the hands of market leaders, so companies will compete fiercely for this position. Chinese investors are fully aware of the problem, but leading tech stocks like Amazon have faced the same situation. If we compare the CSI 300 index with the Nasdaq index, both of these indexes include global leaders in their respective fields. We found that the return on equity (ROE) of American companies is twice that of Chinese companies, but the price- to-book ratio (P/B) paid by investors for American companies is four times that of Chinese companies (8.2 times vs. 2.0 times) . Most Chinese large-cap stocks are also listed in Hong Kong, where their stock prices are usually around 40% cheaper, close to a 1-fold price-to-book ratio. If you look at the MSCI China Index, its price-to-earnings ratio discount reaches a record 10 percentage points compared to the world index, and it is also close to the lower limit of its valuation range.

As Chinese companies expand in the global market, this valuation discount seems to turn into a premium at some point in the future. We believe that investors must turn sharply to Chinese stocks in the medium term, and it may be difficult to obtain them without pushing up the stock price. We have always been optimistic about the Chinese stock market, but have been troubled by the fact that the world can’t awaken and buy Chinese stocks, and we believe that China’s “Sputnik Moment” (or events such as the dominance of the electric vehicle sector) This is the factor. We expect the Hong Kong/China stock market to continue to lead in the medium term, just like in 2024.

Figure 12: Comparison of expected price-to-earnings ratios between MSCI China Index and MSCI World Index

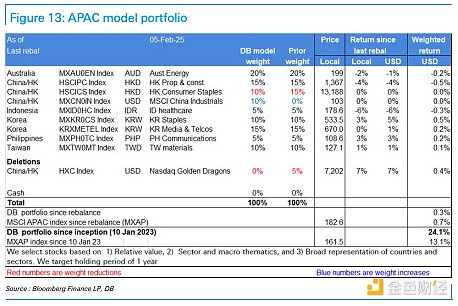

Figure 13: Asia-Pacific Portfolio Model

panewslab

panewslab