Grayscale: How to add crypto investments to a diversified portfolio?

Reprinted from jinse

01/15/2025·22days agoSource: Grayscale; Compiler: Deng Tong, Golden Finance

summary

-

Cryptocurrencies are a unique, high-volatility alternative asset class that may help enhance risk-adjusted returns when added to a traditional investment portfolio.

-

A little goes a long way when including cryptocurrencies in a portfolio: Traditional portfolio optimization techniques suggest that an allocation of around 5% maximizes expected risk-adjusted returns. However, allocating to cryptocurrencies may also increase portfolio risk.

-

Allocations to cryptocurrencies may displace other assets used to enhance returns or diversify, including gold and other commodities, small-cap and international stocks or technology stocks. The crypto asset class may also replace some private investments because it can provide more liquidity.

-

Investors should consider their own circumstances and financial goals before investing in cryptocurrencies. This asset class should be considered high risk and may not be suitable for investors with short-term capital needs and/or a high risk aversion.

Constructing a highly diversified portfolio has become increasingly difficult due to greater concentration of returns from traditional assets, changing correlations, and macro risks. At Grayscale, we believe the crypto asset class can be a way to help address these challenges. The crypto asset class includes a variety of technologies with many specific use cases. For example, Bitcoin is a currency system, while Aave is a lending protocol, and Bittensor is a platform for building open source AI. This diversity raises a question for asset allocators: When considering portfolio allocation, should crypto assets be viewed as commodities, technology investments, or something else?

Grayscale Research believes that cryptocurrencies should be viewed as a unique high-volatility alternative asset class that, when included in traditional investment portfolios, may help improve risk-adjusted returns. While the individual assets vary, they are all based on the same underlying technology – a public blockchain – and most can be considered early-stage investments. The main difference with other early-stage investment options, such as venture capital, is the market structure of cryptocurrencies: blockchain-based assets are liquid and traded around the world, including by many retail investors. These characteristics—early-stage investments that trade in liquid public markets and can be purchased by anyone—generate a set of statistical attributes that can be used to guide portfolio construction.

Behavior of Crypto Asset Classes

Over its relatively short history, crypto asset class returns have exhibited four main statistical characteristics: (1) high volatility; (2) returns relative to the volatility of other major asset classes; (3) relative to traditional Assets have low correlation; (4) relatively high momentum (statistical persistence). [1] Additionally, these statistical characteristics tend to evolve over time, especially for more mature digital assets like Bitcoin.

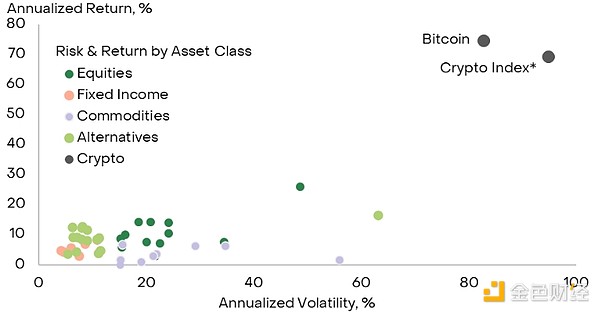

1. High volatility. Cryptocurrencies are a unique major asset class with extremely high volatility. Since the beginning of 2017, the annualized volatility of the market capitalization weighted index [2] of investable digital assets has been 95%; Bitcoin’s volatility over the same period has been 83%. By comparison, the S&P 500's annualized volatility is 16%, and the Nasdaq 100's annualized volatility is 19%. Cryptocurrency volatility is closer to that of certain high price volatility commodities such as natural gas or investment strategies that employ leverage (Figure 1). Therefore, the crypto asset class should be considered high-risk, which is the primary consideration that investors should keep in mind before including crypto assets in their portfolios.

Figure 1: Cryptocurrencies are a unique and volatile major asset class

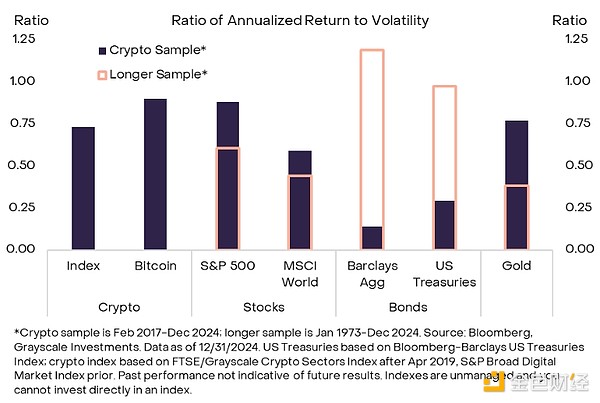

2. Returns are commensurate with volatility. At the same time, Bitcoin and digital assets as a whole (based on market-cap-weighted indexes, for example) generate returns commensurate with their higher volatility. In other words, cryptoassets compensate investors for the higher risks they take with higher returns. For example, since the beginning of 2017, the same market cap-weighted index of investable crypto assets has returned an annualized rate of 69%. Given annualized volatility of 95%, the return-to-volatility ratio is about 0.7. Over the same period, the S&P 500 has annualized returns of 14% and volatility of 16%, giving a return-to-volatility ratio of about 0.9. [3] Over periods of about 10 years or more, return-to-volatility ratios for major asset classes tend to be in the 0.5-1.0 range, and cryptocurrency returns are also in this range (Chart 2). Therefore, given its higher volatility, cryptocurrency returns are comparable to those we observe for other asset classes.

Figure 2: Cryptocurrencies have similar returns and volatility to other asset classes

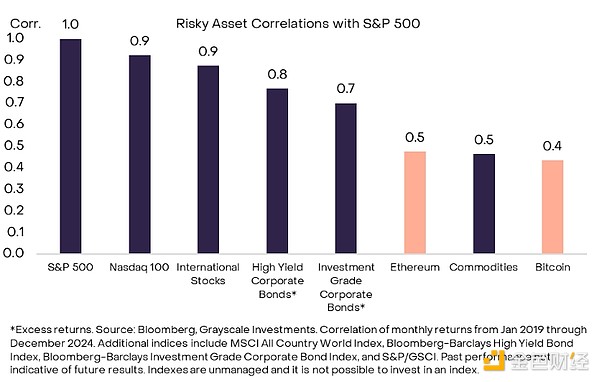

3. Low correlation with traditional assets. Higher volatility and higher returns can be achieved through leverage – investing more capital by borrowing money. However, adding leverage to traditional assets does not affect their correlations and therefore cannot be used to improve risk-adjusted returns. [4] The crypto asset class is unique in that it offers high risk and high potential returns while having low correlation with traditional assets (Figure 3). Lower correlations are the “secret secret” to portfolio diversification and why data-driven portfolio optimization approaches often include the crypto asset class.

Figure 3: Correlation between cryptocurrencies and stock market returns has historically been low

4. High momentum. Historical returns from the crypto asset class have shown relatively high momentum compared to stocks and bonds: gains tend to follow gains and losses tend to follow losses. In this way, digital asset returns are more similar to returns from currency and commodity assets, which also exhibit price momentum. The combination of high volatility and high momentum means that the crypto asset class occasionally produces concentrated periods of sharp gains, as well as periods of sharp declines. Investors who include cryptocurrencies in a diversified portfolio may consider using trend following strategies for risk management.

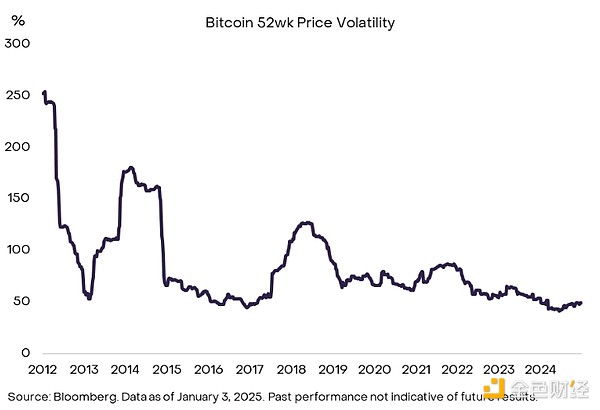

Although the crypto asset class has grown to considerable size, it is still relatively young and its statistical properties may change over time. This is already the case for some more mature assets, such as Bitcoin, where price volatility has declined (Figure 4). Grayscale Research believes that public blockchain can be viewed as a network technology, and economic theory predicts that the value of a network will have a non-linear relationship with the size of the network. Therefore, investors should be prepared for changes in the statistical return behavior of blockchain-based assets as user adoption grows.

Figure 4: Bitcoin volatility decreases over time

Diversification advantage

When constructing a diversified portfolio, investors typically consider the expected risk and expected return of each asset, as well as the expected correlations between assets, to arrive at a combination that maximizes risk- adjusted returns. [5] The inclusion of crypto asset classes is no exception: investors should consider expected risks, returns, and correlations based on historical performance and judgments about how future returns may vary.

As a benchmark example, Grayscale Research considers incorporating Bitcoin into a traditional 60/40 stock and bond portfolio. [6] We simulated hypothetical portfolios containing different amounts of Bitcoin using Monte Carlo methods. We then estimate the expected annualized return and annualized volatility of the portfolio and calculate the expected Sharpe ratio (see Technical Appendix for details). [7] For the baseline example, we assume that the distribution of Bitcoin’s future returns will match actual returns since 2014. Bitcoin is used as a representative digital asset due to its longer history; we will consider portfolios with a wider range of digital assets in the next section.

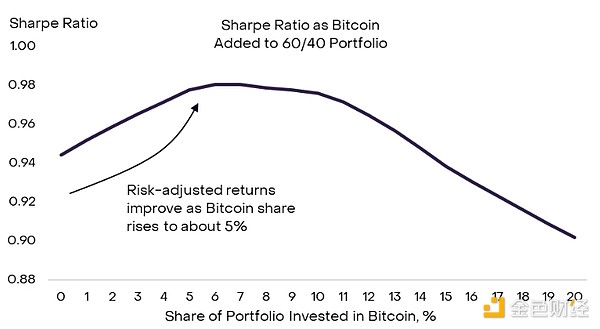

Figure 5 shows the results of our baseline simulation. As Bitcoin is added to a classic 60/40 portfolio in small increments, expect the Sharpe ratio to rise initially. The reason is that although Bitcoin is a volatile asset, it can provide high returns and has low correlation with traditional assets, thus providing diversification advantages. The Sharpe ratio continues to rise until Bitcoin accounts for approximately 5% of the total portfolio, and then begins to level off. After this point, increasing Bitcoin allocations is no longer expected to improve risk-adjusted returns.

Figure 5: Adding Bitcoin to a traditional portfolio may improve risk-adjusted returns

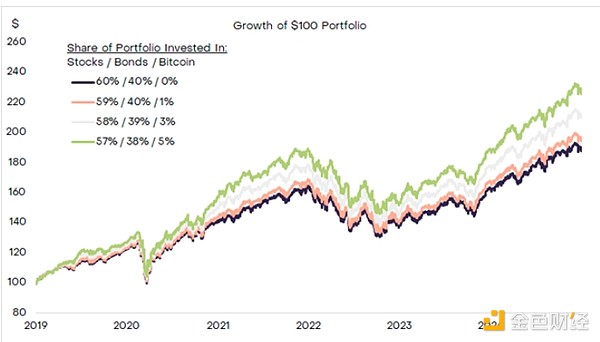

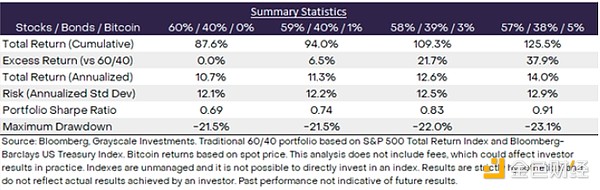

Because cryptocurrencies are a volatile asset class, only a small investment can have a big impact: even a modest allocation to Bitcoin and other digital assets can significantly improve total and risk-adjusted returns. For example, Exhibit 6 shows the hypothetical ex post impact of adding Bitcoin to a traditional 60/40 portfolio in increments of 1%, 3%, and 5%. These results are entirely hypothetical and do not reflect actual results achieved by investors. When adding Bitcoin to a 60/40 portfolio at these amounts, annualized returns increased by 0.6-3.3 percentage points (pp) over the period, and the portfolio Sharpe ratio increased by 0.05-0.22pp. While both total and risk-adjusted returns are increasing, it is important to emphasize that portfolio risk, including maximum drawdowns, are also increasing.

Figure 6: Hypothetical impact of a 1%-5% Bitcoin allocation on a 60/40 portfolio

Of course, this is just a simulation under certain assumptions and there is no guarantee that future returns will match past returns. Investors should consider a range of possible outcomes for crypto asset returns before allocating capital. While an allocation of around 5% may maximize risk- adjusted returns based on historical results, a lower amount may be appropriate if Bitcoin's returns decline in the future or its correlation with other asset classes increases.

FAQ

While traditional portfolio optimization techniques can be a useful starting point, investors often need to address a variety of practical implementation issues when allocating to crypto asset classes. Here are some of the most common questions we receive from investors about incorporating cryptocurrencies into a diversified portfolio:

1. How do portfolio results change when considering cryptoassets other than Bitcoin? Cryptoassets with a lower market capitalization than Bitcoin (traditionally known as "altcoins") generally have higher price volatility and should be considered riskier. Additionally, the asset universe is highly diverse in terms of use cases, market capitalization, and correlation with traditional assets. During the period when broad indices of crypto market performance were available[8], altcoins as a category had slightly lower total and risk-adjusted returns than Bitcoin, although this may not be the case in the future. [9] At a minimum, investors considering an allocation to altcoins should take a diversified approach that reflects higher idiosyncratic risks and may want to consider methods of evaluating token-specific fundamentals. That being said, taking historical data at face value, our Monte Carlo simulations suggest that an allocation of ~5% would also maximize expected risk-adjusted returns on a market-cap-weighted basket of cryptoassets including Bitcoin and altcoins.

2. When adding cryptocurrencies, which parts of my existing portfolio should I reduce from? In a diversified portfolio, crypto asset classes can provide return enhancement, diversification, or both. As such, it may replace existing allocations designed to deliver these attributes, including gold and other commodities, small-cap and international equities or technology stocks. Cryptocurrencies may also replace certain private investments (such as private equity, venture capital, or infrastructure) where it will also provide more portfolio liquidity. Crypto asset classes may offer higher risk and higher potential returns than other asset classes, potentially helping to increase the capital efficiency of the overall portfolio.

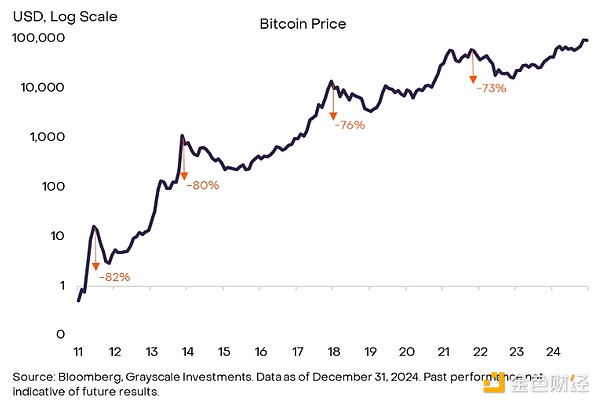

3. What has been the magnitude and frequency of declines in the past? Bitcoin has experienced four long-term declines in its history (Chart 7). Using monthly data, the average peak-to-trough decline over these periods was 77%. As mentioned above, trend following strategies may be used to manage downside risk. There are many more examples of smaller declines. For example, during the latest appreciation phase of the crypto market cycle (from December 2018 to November 2021), the price of Bitcoin increased approximately 21 times. However, during this period, the price of Bitcoin fell by at least 10%, a total of 11 times. During the last appreciation phase of the crypto market cycle (from January 2015 to December 2017), Bitcoin’s price fell by at least 20% a total of 11 times. [10]

Figure 7: Bitcoin has experienced four major declines in its 16-year history

4. Should I view Bitcoin as a defensive asset? Grayscale Research believes that Bitcoin can be considered a store of value: we expect it to retain its real value (i.e. taking inflation into account) over the long term because it is scarce and not tied to any particular institution. Bitcoin today should not be viewed as a defensive asset that can dampen portfolio volatility during recessions or other periods of heightened risk aversion. Bitcoin is a highly volatile asset that is positively correlated with the stock market and typically falls when risk aversion increases. Additionally, gold and short-term U.S. Treasuries tend to outperform Bitcoin when geopolitical risks increase, at least for now.

The role of cryptocurrency

It is important to stress that investing in digital assets may not be suitable for everyone. For this analysis, we consider a representative investor holding a classic 60/40 portfolio. In practice, however, there are many types of investment portfolios that meet different financial needs. For example, some investors hold a portfolio of low-volatility assets because their capital is earmarked for upcoming expenses (such as a home purchase or college tuition). Cryptocurrencies are a highly volatile asset class that can generate strong returns over time, but can also lose significant value in the short term. Additionally, some investors favor income-producing assets such as fixed- income securities or dividend-paying stocks. While some crypto-assets will generate income, in most cases the returns will be low compared to the volatility of the asset - cryptocurrencies are an asset class primarily used for capital appreciation.

While there are some exceptions, Grayscale Research's analysis suggests that a traditional balanced portfolio can achieve higher risk-adjusted returns with a modest allocation to cryptocurrencies, perhaps around 5% of total financial assets. Because cryptocurrencies are a high-risk/high-return potential asset class with low correlation to equities, crypto assets may help investors overcome some of the portfolio construction challenges they currently face. Allocating to cryptocurrencies doesn't change other traditional thinking about portfolio construction, including reducing portfolio volatility as you approach retirement, using tax-advantaged accounts when possible, and avoiding trying to time the market.

Comment

[1] In its early history, Bitcoin also exhibited positive skew. We do not consider the impact of positive skew in this report, but did discuss it in a previous report on cryptocurrencies in portfolios.

[2] In this report, we use a composite index of two market cap-weighted cryptocurrency price indices, with start dates selected based on data availability. The FTSE/Grayscale Cryptocurrency Industry Index Series began in April 2019. Prior to this, the only other available broad market cap-weighted index of cryptocurrency price returns was the S&P Cryptocurrency Broad Digital Market Index, which was launched in February 2017. In this report, our measure of crypto asset class returns is based on the S&P Broad Digital Market Index as of March 2019 and the FTSE/Grayscale Cryptocurrency Industry Index Series since then.

[3] Source: Bloomberg, Grayscale Investments. Data as of December 31, 2024.

[4] Risk parity strategies typically apply leverage to low-volatility asset classes such as Treasuries, which can theoretically improve risk-adjusted returns.

[5] These are the basic concepts of modern portfolio theory, a common approach to portfolio construction.

[6] This is a simplification as many modern portfolios may contain some alternative asset classes.

[7] When calculating the Sharpe ratio, the cash return rate is assumed to be zero.

[8] As noted in footnote #2, this is data from February 2017 to the present.

[9] Source: Bloomberg, Grayscale Investments. Based on the FTSE/Grayscale Crypto Sectors Series Index and the S&P Crypto Broad Digital Market Index.

[10] Source: Coin Metrics, Grayscale Investments. Data as of December 31, 2024.

panewslab

panewslab