In-depth analysis of Usual: The “trick” behind USD0++ de-anchoring and revolving loan liquidation

Reprinted from panewslab

01/16/2025·19days agoAuthor: Bai Ding&Shew, GodRealmX

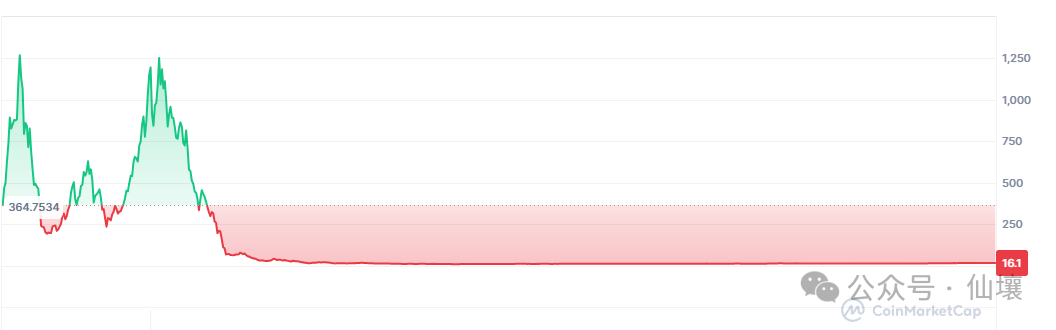

The recent unanchoring of USD0++ issued by Usual has become a hotly discussed keyword in the market and has also caused panic among many users. The project increased more than 10 times after being listed on the top CEX in November last year. Its RWA-based stablecoin issuance mechanism and Token model are quite similar to Luna and OlympusDAO in the previous cycle, plus French Congressman Pierre Person Endorsed by the government, Usual once gained widespread attention and heated discussion in the market.

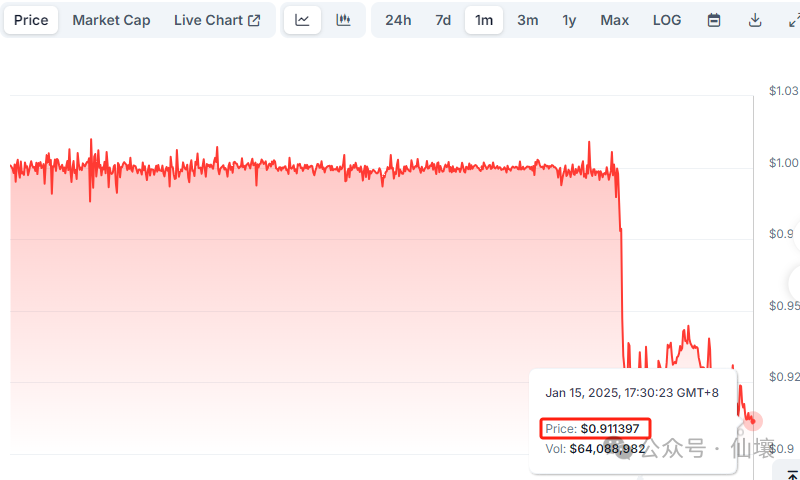

Although the general public once had good hopes for Usual, the recent "farce" has brought Usual down from the altar. As Usual officials announced on January 10 that they would modify the early redemption rules for USD0++, USD0++ was once detached to nearly $0.9. As of the evening of January 15, 2025, when this article was published, USD0++ was still hovering around $0.9.

The current controversy surrounding Usual has reached its peak, and dissatisfaction in the market has completely erupted, causing an uproar. Although Usual's overall product logic is not complicated, it involves many concepts and trivial details. One project is divided into many different Tokens, and many people may not have a systematic understanding of the causes and consequences.

The author of this article aims to systematically sort out the causal relationship between Usual product logic, economic model and the USD0++ de-anchoring from the perspective of Defi product design, so as to help more people deepen their understanding and thinking about it. Here we also first throw out a point of view that seems a bit "conspiracy theory":

In a recent announcement, Usual set the unconditional guaranteed floor price of USD0++ against USD0 to 0.87. The purpose is to blow up the USD0++/USDC revolving loan position on the Morpha lending platform and eliminate the main users in the mining and selling, but not to let USDC++/ There are systemic bad debts in the USDC vault (liquidation line LTV is 0.86).

Below we will elaborate on the relationship between USD0, USD0++, Usual and their governance tokens to help everyone truly understand the tricks behind Usual.

Understand its products from the Token issued by Usual

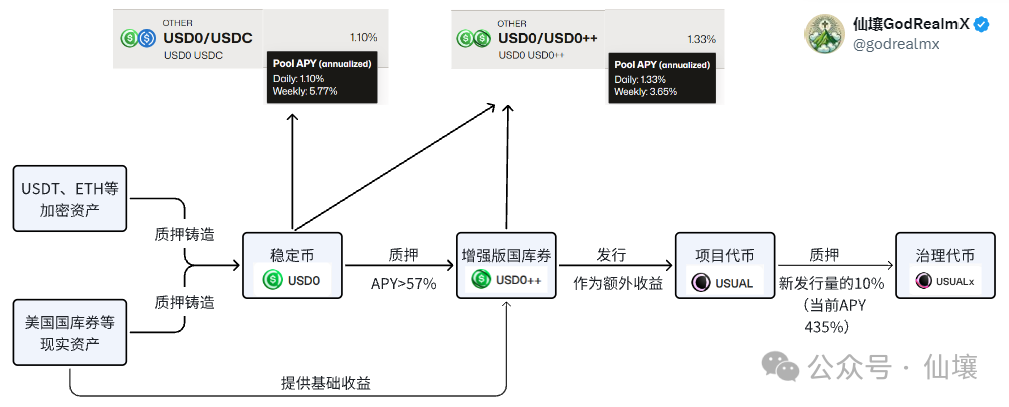

There are four main types of Tokens in Usual 's product system, namely the stable currency USD0, the bond token USD0++, and the project token USUAL. In addition, there is also the governance token USUALx, but since the latter is not important, Usual's product logic mainly follows The first three types of Token are divided into three layers.

The first layer: stable currency USD0

USD0 is an equally mortgaged stablecoin that uses RWA assets as collateral. All USD0 is backed by RWA assets of equal value. But currently most USD0 is minted with USYC, and some USD0 uses M as collateral. (USYC and M are both RWA assets secured by U.S. short-term Treasury bonds)

It can be found that the collateral on the USD0 chain is located at

The address 0xdd82875f0840AAD58a455A70B88eEd9F59ceC7c7 holds a huge amount of USYC assets.

Why does the vault used to store underlying RWA assets contain a large amount of USD0? This is because when a user destroys USD0 to redeem RWA tokens, part of the handling fee will be deducted, and this part of the handling fee will be stored in the vault in the form of USD0.

The minting contract address of USD0 is 0xde6e1F680C4816446C8D515989E2358636A38b04. This address allows users to mint USD0 in two ways:

1. Directly mint USD0 with RWA assets. Users can inject Usual-supported tokens such as USYC into the contract to mint USD0 stable coins;

2. Transfer USDC to the RWA provider and mint USD0.

The first option is relatively simple. The user inputs a certain number of RWA tokens, and the USUAL contract will calculate how many US dollars these RWA tokens are worth, and then issue the corresponding USD0 stable currency to the user. When the user redeems, the corresponding value of RWA tokens will be returned based on the USD0 amount entered by the user and the RWA token price. During this process, the USUAL protocol will deduct part of the handling fee.

It is worth noting that most of the current RWA tokens are automatically compounded and will continue to generate interest through additional issuance or value growth. RWA token issuers tend to hold a large number of interest-earning assets off-chain, the most common of which are U.S. Treasury bonds, and then return the interest on the interest-earning assets to RWA token holders.

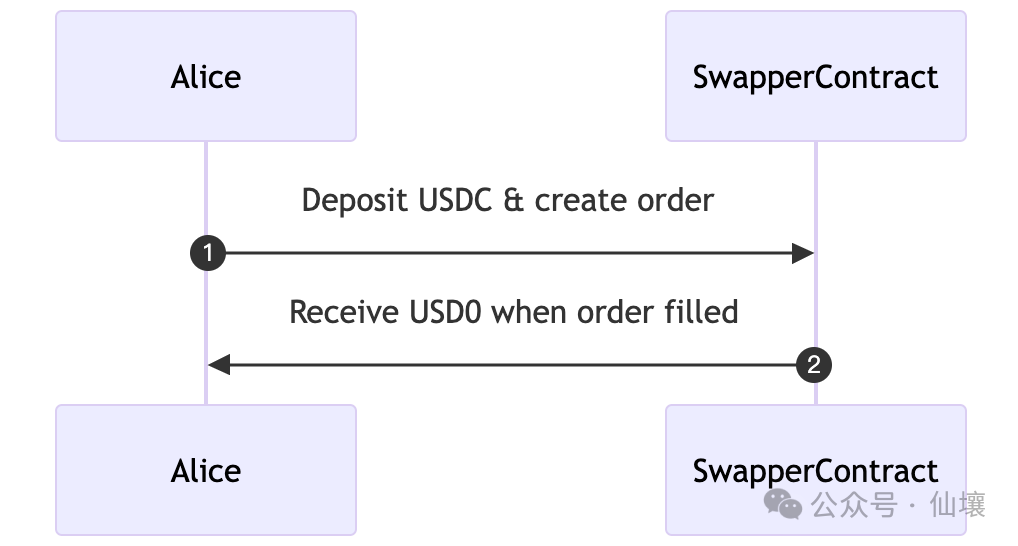

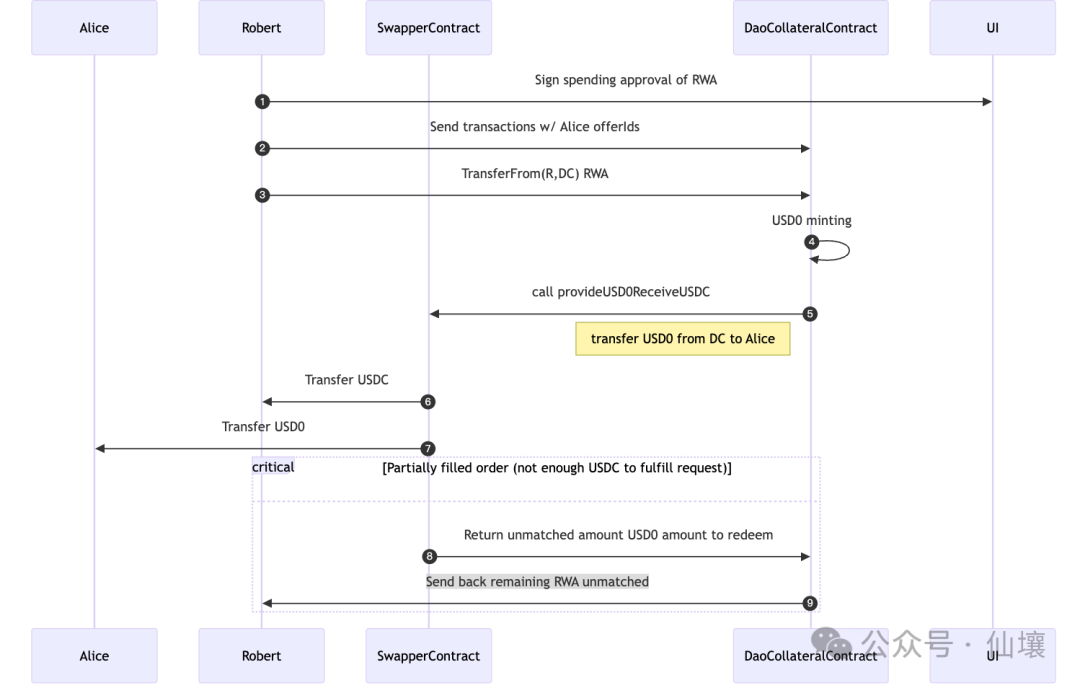

The second option for minting USD0 is more interesting, as it allows users to mint USD0 directly with USDC. However, the RWA provider/payer must participate in this link. To put it simply, users need to place orders through the Swapper Engine contract, declare the amount of USDC paid, and send the USDC to the Swapper Engine contract. When the order is matched, the user can automatically obtain USD0. For example, for user Alice, the perceived process is as follows:

However, the actual process involves the participation of RWA providers/payers. For example, in the figure below, Alice's request to exchange USDC for USD0++ is responded to by RWA provider Robert, who directly mints USD0 with RWA assets, then transfers USD0 to the user through the Swapper Engine contract, and then takes away the USDC assets paid by the user when placing an order. .

Robert in the picture below is the RWA provider/payer. It is not difficult to see that this model is essentially similar to Gas payment. When you want to use a Token you do not have to trigger some operations, you use other Tokens to find someone to replace you. Trigger the operation, and the latter will try to transfer the "earnings" after the trigger operation to you, and collect some handling fees from it.

The figure below shows the series of transfer actions triggered when the RWA provider accepts the user's USDC assets and mints USD0 tokens for the user:

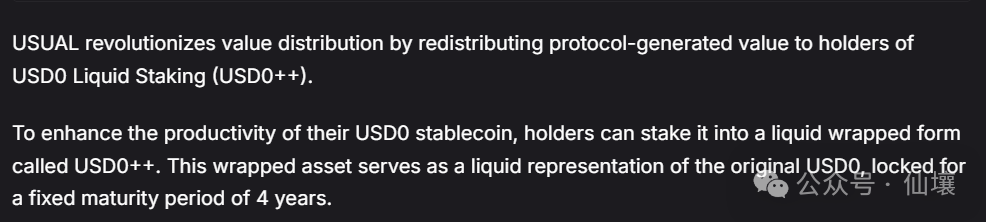

Second level: Enhanced version of treasury bills USD0++

In the above, we mentioned that users need to pledge RWA assets when minting USD0 assets, but the interest generated automatically by RWA assets will not be directly distributed to the people who mint USD0, so where does this part of the interest ultimately go? The answer is that it flows to the Usual DAO organization, and then the interest on the underlying RWA assets will be distributed twice.

USD0++ holders can share the interest income. If you pledge USD0 to mint USD0++ and become a USD0++ holder, you can share the interest of the bottom RWA assets. But please note that only the underlying RWA interest corresponding to the portion of USD0 that mints USD0++ will be distributed to USD0++ holders.

For example, if the underlying RWA assets currently used as collateral to mint USD0 are US$1 million, US$1 million of USD0 is minted, and then US$100,000 of USD0 is minted into USD0++, then these USD0++ holders will only receive US$100,000. The interest income from the RWA assets and the interest from the other $900,000 RWA assets became the income of the Usual project party.

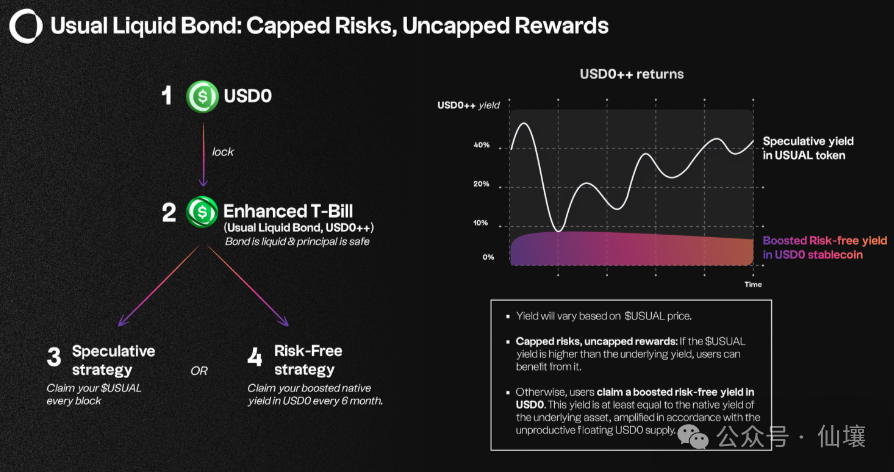

In addition, USD0++ holders can also receive additional USUAL token incentives. USUAL will issue additional tokens and distribute them through a specific algorithm every day, and 45% of the new tokens will be distributed to USD0++ holders. In summary, the income of USD0++ is divided into two parts:

- The income from the underlying RWA assets corresponding to USD0++;

- Earnings from daily new USUAL token distribution;

The above chart shows the revenue source of USD0++. Holders can choose to receive income denominated in USUAL every day, or receive income denominated in USD0 every 6 months.

With the support of the above mechanism, the pledged APY of USD0++ is usually maintained above 50%, and it was still 24% after the incident. But as mentioned above, a large part of the income of USD0++ holders is issued in USUAL tokens, and there is a lot of moisture as the price of Usual fluctuates. Under Usual's recent troubles, this rate of return is most likely not guaranteed.

According to Usual's design, USD0 can be pledged to mint USD0++ at a ratio of 1:1, and the default lock-up period is 4 years. So USD0++ is similar to a tokenized four-year floating rate bond. When users hold USD0++, they can earn interest denominated in USUAL. If the user cannot wait 4 years and wishes to redeem USD0, he can first exit through secondary markets such as Curve and directly go to the USD0++/USD0 trading pair to redeem the latter.

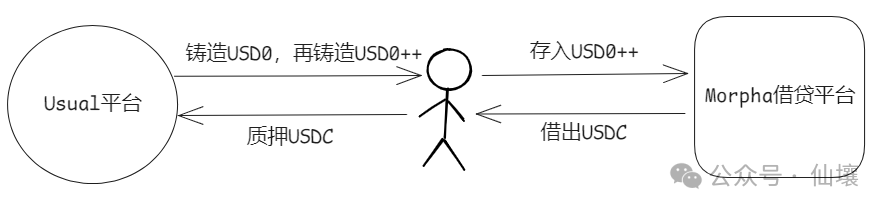

In addition to Curve, there is another solution, which is to use USD0++ as collateral in lending protocols such as Morpho to lend assets such as USDC. At this time, the user needs to pay interest. The picture below shows Morpho's lending pool using USD0++ to lend USDC. You can see that the current annualized interest rate is 19.6%.

Of course, in addition to the above-mentioned indirect exit path, USD0++ also has a direct exit path, which is also the inducement that led to the recent de-anchoring of USD0++. But we plan to elaborate on this part later.

The third layer: project tokens USUAL and USUALx

Users can obtain USUAL by pledging USD0++ or purchasing directly from the secondary market. USUAL can also be used for pledge to mint the governance token USUALx at a 1:1 ratio. Whenever USUAL is issued, holders of USUALx can receive 10% of it. Currently, according to the documentation, USUALx also has an exit mechanism for converting to USUAL, but it requires a certain handling fee to be paid when exiting.

At this point, the entire three-tier product logic of Usual is as follows:

In summary, the RWA assets underlying USD0 gain interest income, and part of the income is distributed to USD0++ holders. With the empowerment of USUAL tokens, the APY income of holding USD0++ is further increased, which can encourage users to further mint USD0. Mint it as USD0++, and then obtain USUAL, and the existence of USUALx can prompt USUAL holders to lock up their positions.

Unanchoring Incident: The "Conspiracy Theory" Behind the Modification of Redemption Rules - The Revolving Loan Burst and the Morpha Liquidation Line

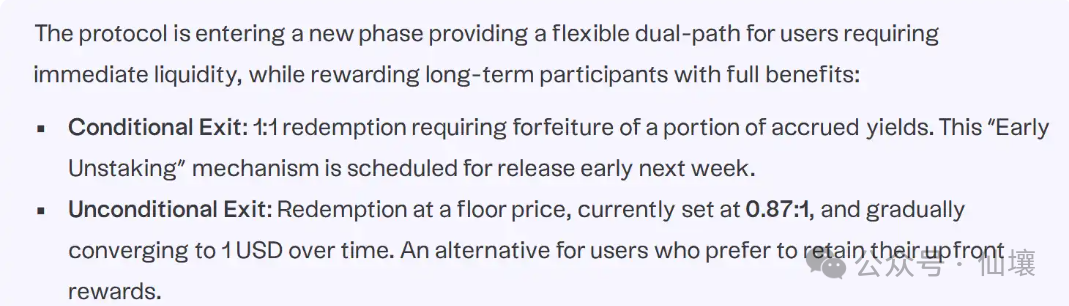

Usual's previous redemption mechanism was to exchange USD0++ for USD0 on a 1:1 basis, which was a guaranteed redemption. For stablecoin holders, the APY of more than 50% is very attractive. The guaranteed redemption provides a clear and safe exit mechanism. Coupled with the background endorsement of the French government, Usual has successfully attracted many large investors. However, on January 10th, the official announcement changed the redemption rules so that users can choose 1 of the following two redemption mechanisms:

1. Conditional redemption. The redemption ratio is still 1:1, but a considerable portion of the proceeds issued in USUAL will be paid. 1/3 of this income will be distributed to USUAL holders, 1/3 will be distributed to USUALx holders, and 1/3 will be burned;

2. Unconditional redemption, no deduction of income, but no minimum guarantee, that is, the proportion of USD0 redeemed is reduced to a minimum of 87%. Officials say that the proportion may return to 100% over time.

Of course, users can also choose not to redeem and lock USD0++ for 4 years, but this involves too many variables and opportunity costs.

So back to the point, why did Usual come up with such an obviously unreasonable clause?

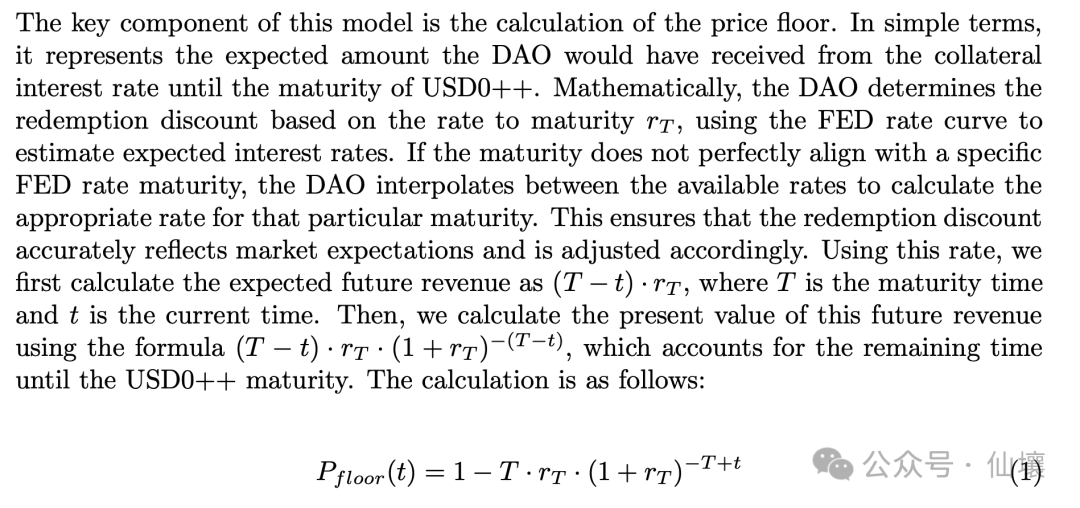

As we mentioned earlier, USD0++ is essentially a tokenized 4-year floating interest rate bond. Direct withdrawal means forcing Usual officials to redeem the bond in advance. The USUAL protocol believes that users promise to lock USD0 for four years when minting USD0++, and quitting midway is a breach of contract and requires payment of a penalty.

According to the USD0++ white paper, if a user initially deposits 1 USD of USD0, and when the user wants to exit early, he or she needs to make up for the interest income of the 1 USD in the future. The assets ultimately redeemed by the user are:

$1 — future interest income. As a result, the mandatory redemption floor price of USD0++ is lower than US$1.

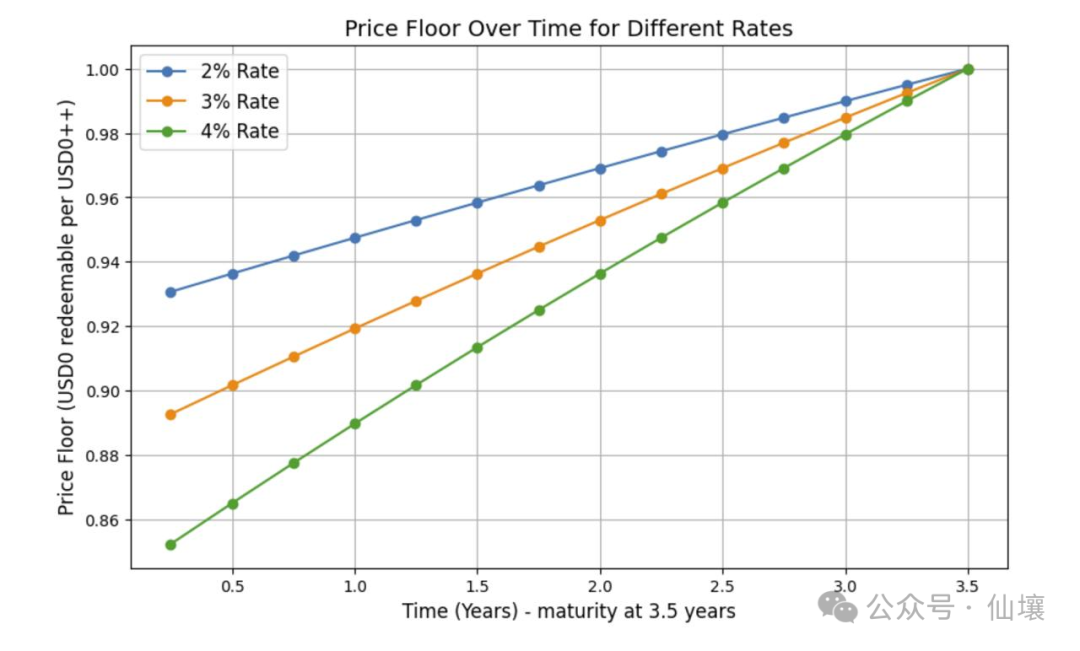

The figure below shows the USD0++ floor price calculation method from USUAL official documents (it seems to have some gangster logic at the moment):

Usual’s announcement will not take effect until February 1, but many users began to flee immediately, causing a chain reaction. It is generally believed that according to the redemption mechanism in the announcement, it is no longer possible for USD0++ to maintain rigid redemption with USD0, so USD0++ holders began to withdraw early;

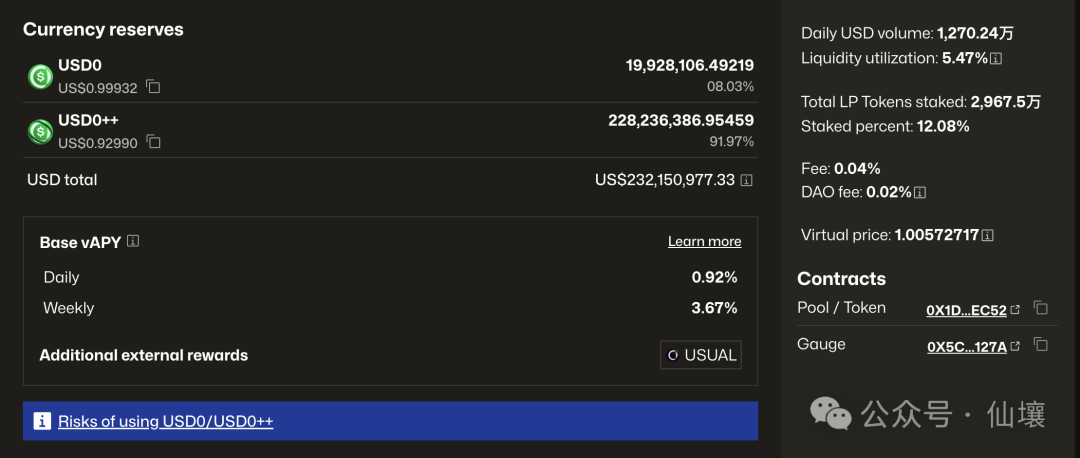

This panic naturally spread to the secondary market, and people sold USD0++ crazily, causing a serious imbalance in the USD0/USD0++ trading pair in Curve, with the ratio reaching an exaggerated 9:91; in addition, the price of USUAL plummeted along with the trend. Due to market pressure, Usual decided to advance the announcement to take effect next week, in order to increase the cost of users abandoning USD0++ to redeem USD0 as much as possible, and play a role in protecting the price of USD0++.

Of course, some people say that USD0++ is not a stable currency, but a bond, so there is no such thing as de-anchoring. While this view is theoretically correct, we would like to object here.

First, the unspoken rule of the crypto market is that only stablecoins will have “USD” in their names. Second, USD0++ is originally exchanged for stablecoins on Usual at a ratio of 1:1, and people assume that its value is equivalent to stablecoins; thirdly, Curve’s stablecoin trading pool has trading pairs that include USD0++. If USD0++ does not want to be considered a stable currency, you can change its name and ask Curve to delist USD0++, or change it to a non-stable currency pool.

So what is the motive of the project team to obscure the relationship between USD0++ and bonds and stablecoins? There may be two points. (Note: The following opinions contain conspiracy theory elements and are speculations based on some clues. Do not take them seriously)

1. The first is to accurately blast the revolving loan. Why is the underpinning ratio coefficient of unconditional redemption set at 0.87, which is just a little higher than the liquidation line of 0.86 on Morpha?

This involves another decentralized lending protocol: Morpho. Morpho is famous for creating an exquisite DeFi protocol with 650 lines of minimalist code. One fish eats more is a DeFi tradition. In order to increase the utilization rate of funds after minting USD0++, many users put USD0++ in Morpho and lend USDC, and the loaned USDC was used to re-mint USD0 and USD0++, thus forming a revolving loan.

Revolving loans can significantly increase users’ positions within the lending agreement, and more importantly, the USUAL protocol will allocate USUAL token incentives to positions within the lending agreement:

The revolving loan has brought better TVL to Usual, but as time goes by, there is an increasing risk of leverage chain rupture, and these revolving loan users rely on repeated minting of USD0++ to obtain a large amount of USUAL tokens, which is a mining and selling method. The main force, if Usual wants to develop in the long term, this problem must be solved.

Let’s briefly talk about the leverage ratio of revolving loans. Suppose you lend USDC, mint USD0++, deposit USD0++, lend USDC back and forth as shown in the picture above, cycle this process and maintain a fixed deposit/lending value ratio (LTV) in Morpha.

Assume LTV = 50%, your initial capital is 100 USD0++ (assumed to be worth 100 US dollars), the value of the USDC loaned each time is half of the deposited USD0++, according to the geometric series summation formula, wait until you can finally lend USDC tends to infinite hours, and the total amount of USDC you lend on a recurring basis tends to $200. It is not difficult to see that the leverage ratio is almost 200%. The leverage ratio of revolving loans under different LTVs follows the simple formula in the figure below:

For those who previously participated in Morpha to Usual revolving loans, the LTV may be higher than 50%, and the leverage ratio is even more alarming. It is conceivable how high the systemic risk behind it is. If it develops like this for a long time, sooner or later there will be mines.

Here we talk about the liquidation line value. In the previous Morpha protocol, the liquidation line LTV of USD0++/USDC was 0.86. That is to say, when the ratio of the USDC you lent/the USD0++ you deposited is higher than 0.86, liquidation will be triggered. For example, if you lend 86 USDC and deposit 100 USD0++, as long as USD0++ falls below 1 US dollar, your position will be liquidated.

In fact, Morpha's liquidation line of 0.86 is very subtle, because the redemption ratio of USD0++ and USD0 announced by Usual is 0.87:1, and there is a direct correlation between the two.

We assume that many users, recognizing the idea of USD0++ stable currency, directly choose the LTV that is extremely high or even close to the liquidation line of 86% for the above-mentioned revolving loan, thus maintaining a huge position with extremely high leverage and obtaining a large amount of interest income. . However, using an LTV of nearly 86% means that as long as USD0++ is unanchored, the position will be liquidated. This is also the main reason for the large liquidation on Morpho after USD0++ is unanchored.

But it should be noted here that even if the revolving loan user's position is liquidated at this time, there will be no loss for the Morpha platform, because at this time 86% < LTV of the liquidated position < 100%, if priced in US dollars, the lent USDC It is still lower than the value of the collateral USD0++, and the platform still has no systematic bad debts (this is very important).

After understanding the above conclusion, it is not difficult for us to understand why the liquidation line of USD0++/USD0 on Morpha was deliberately set at 86%, which is just a little lower than the 0.87 in the later announcement.

From the perspective of the two versions of the conspiracy theory, the first version is that Morpha is the effect and Usual is the cause: the setter of the USD0++/USDC vault on the Morpha lending platform is MEV Capital, which is the manager of Usual. They know the future. The guaranteed floor price will be set at 0.87, so the liquidation line was set slightly lower than 0.87 early on.

First of all, after the Usual protocol was updated and announced, it was stated that the guaranteed redemption price of USD0++ is 0.87, and the reasons were explained in the USD0++ white paper with specific discount formulas and charts. After the announcement, USD0++ began to lose its anchor and was once close to $0.9, but it was always higher than the guaranteed floor price of 0.87. Here we believe that the redemption ratio of 0.87:1 in the announcement is not set arbitrarily, but has been carefully calculated and is more affected by the interest rates in the financial market.

The coincidence is that the liquidation line on Morpha is 86%. As we mentioned earlier, if the guaranteed floor price is 0.87, there will be no systemic bad debts in the USD0++/USDC treasury on Morpha, and the revolving loan position can be easily exploded to achieve Deleverage.

Another version of the conspiracy theory is that Morpha is the cause, and Usual’s subsequent announcement is the result: the liquidation line of 0.86 on Morpha was determined before the guaranteed floor price of 0.87. Later, Usual took into account the situation on Morpha and deliberately set the guaranteed floor price higher than 0.86. A little higher. However, there is definitely a strong connection between the two.

2. Another motive of the Usual project team may be to save the currency price at the lowest cost.

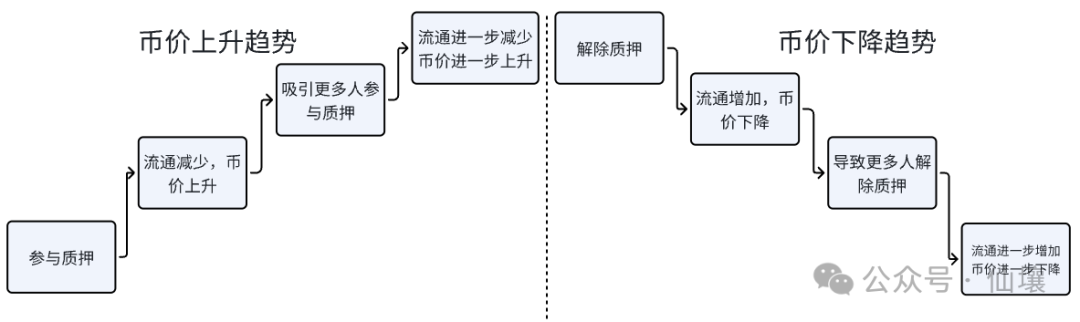

The economic model of USUAL-USUALx is a typical positive feedback flywheel. Its pledge mechanism determines that such tokens usually rise very rapidly, but once there is a downward trend, they will fall faster and faster and enter a death spiral. Once the price of USUAL falls, the staking yield will also be significantly reduced due to the compound effect of the decline in price and additional issuance quantity, triggering panic among users, leading to a large amount of selling of USUAL, forming a death spiral of "the deeper the fall, the faster the decline".

USUAL has been falling since reaching a high of 1.6. The project team may be

aware of the danger and believe that it has entered a death spiral. Once it

enters the falling range, we can only try our best to raise the currency price

to save the market. The most famous project of this type should be OlympusDAO

in the last bull market. At that time, there should be strong external

liquidity injection, which caused its token OHM to get out of the bimodal

shape (quoted from the opinions of some experiencers).

USUAL has been falling since reaching a high of 1.6. The project team may be

aware of the danger and believe that it has entered a death spiral. Once it

enters the falling range, we can only try our best to raise the currency price

to save the market. The most famous project of this type should be OlympusDAO

in the last bull market. At that time, there should be strong external

liquidity injection, which caused its token OHM to get out of the bimodal

shape (quoted from the opinions of some experiencers).

But we can also see from the OHM diagram that such projects often cannot escape the fate of the currency price returning to zero in the end. The project side is also clear about this, but time is profit. Someone has made an estimate, and now the Usual team With a monthly income of around US$5 million, they would have needed to weigh the pros and cons and consider whether they could keep the project alive as long as possible.

But now their actions seem to be to avoid paying real money, and only reverse the decline through gameplay and mechanism changes. In the conditional redemption, part of the income of USD0++ pledgers is divided among USUAL and USUALx holders, and the remaining 1/3 is destroyed, while USUALx is obtained by USUAL pledge.

The so-called conditional redemption is actually to empower the USUAL token, encourage more people to pledge USUAL to obtain USUALx, reduce its circulation in the market, and have the effect of under-damping the market.

However, the intention of the project party is obviously not easy to realize because there is a self-contradictory point.

Since such projects need to set aside a large proportion of token distribution to attract users as considerable staking rewards, they must be low-circulation tokens. USUAL's current circulation is 518 million, but the total amount is 4 billion. If its pledge incentive model wants to continue to operate, it must rely on a steady stream of tokens to be unlocked. In other words, USUAL's inflation is very serious. If you want 1/3 of the destruction amount to curb inflation, the proportion of USUAL collected for conditional redemption must be high enough.

Of course, this ratio is set by the project party itself. In the conditional redemption mode, the calculation formula for the amount of USUAL that the redeemer needs to pay to the Usual platform from the interest is:

Among them, Ut is the current amount of USUAL that can be "accumulated" for each USD0++; T is the time cost factor, which defaults to 180 days (set by DAO); A is the adjustment factor. Simply put, it is the official setting of a weekly redemption Amount X, if the redemption amount that week is greater than Obviously when there are too many redeemers, more Usual income needs to be paid. Both T and A are adjusted by the project party.

But the problem is that if the conditional redemption channel requires users to pay a too high proportion of Usual income, users will directly choose unconditional redemption. At this time, it is easy for the price of USD0++ to drop again until it hits the guaranteed floor price of 0.87. Coupled with the panic selling, cancellation of pledges, and loss of credibility caused by the project party’s announcement, it is difficult to say that this is a successful strategy.

However, there is also another interesting saying in the market: Usual has solved the dilemma of mining, raising and selling in DeFi by relying on its own unique method of "closing the door and beating the dog". Overall, the Usual project team’s unconditional guaranteed floor price of US$0.87 and the conditional redemption mechanism make us suspect that the Usual protocol is deliberately operating to allow large revolving loan holders to cough up their profits.

What the future holds and the issues exposed

Before the USUAL payment ratio for conditional redemption comes out, it is not easy to judge which method most users will choose and whether USD0++ can be anchored back. As for the USUAL price, it is still the same contradictory issue: the project team wants to reverse the death spiral simply by using tricks in the gameplay mechanism instead of real money, but the unconditional guaranteed bottom price of 0.87 is not low enough, and many people will choose to withdraw unconditionally rather than conditionally. If you withdraw, you won't be able to burn too much USUAL to reduce the circulation.

Beyond Usual itself, this incident exposed three more direct problems.

First, Usual’s official documents have long stated that there is a 4-year lock-in period for USD0 pledge, but the specific rules for early redemption were not explained before. Therefore, this Usual announcement did not suddenly stipulate a new rule that was never mentioned, but the market was indeed in an uproar and even panic. This shows that many people participating in DeFi protocols do not read the project documents carefully at all.

DeFi protocols are becoming more and more complex as they develop today. There are fewer and fewer simple and clear projects like Uniswap and Compound. This is not necessarily a good thing. The amount of funds users participate in DeFi is often not too small. At least the DeFi protocol should be listed on the official website. See the documentation clearly and understand it.

Second, even though the official documents have already stated it, it is undeniable that Usual sets the rules when it is set, and modifies the rules when it is set. The so-called parameters such as T and A are also in its own hands. In this process, there is neither strict resolution of DAO proposals nor inquiry of community opinions.

The irony is that officials have been emphasizing the governance attributes of USUALx tokens in documents, but there is no governance link in the actual decision-making process. It must be admitted that most Web3 projects are still in a very centralized stage. Combined with the first point, there are still quite a few problems with user asset security. We always emphasize technologies such as TEE and ZK that can better ensure asset security, but the decentralization and asset security awareness of project parties and users should also be paid attention to.

Third, the entire industry is indeed constantly evolving. Following the lessons learned from projects such as OlympusDAO and due to similar economic models, Usual began to consider reversing the trend as soon as the currency price started to trend downward. We always say that there are few real-implementation projects in web3, but the industry ecosystem as a whole is constantly developing rapidly. The previous projects are not completely meaningless, and the success or failure will be seen by latecomers. Maybe It will exist in another way in those truly meaningful projects. At this time when the market and ecology are not so prosperous, we should not lose confidence in the entire industry.

jinse

jinse