The market is "bearing" again, and a list of 5 real income projects worth paying attention to

Reprinted from panewslab

02/19/2025·2MAuthor | defioasis

Edit | Colin Wu

This article is for information and does not share any financial advice only. Please strictly abide by the laws and regulations of the location.

Memecoin once attracted a lot of attention and investment with its unique cultural, humorous image and community-driven characteristics, and the mechanism of pump fun fair launch has pushed the Meme craze to a new height. But with the intensification of PvP and the rapid development of a new market, the so-called narrative logic, Meme symbols and community culture have long disappeared. Who calls for orders has become the key, and the status and background resources of the caller determine the peak that Memecoin price can reach in short-term attention, and after the emotions and attention are over, they will be in a mess. With US President Trump and CZ, founder of Binance, the largest exchange, successively "shouted orders", Memecoin's role as a carrier of pure attention game tools seems to have reached its peak, because there are people with higher status than the two. There are only a few, and many users also feel tired. As the opposite of fair launch, VCcoin has issues such as high valuation and low efficiency, sustainable projects with clear business models, real revenues and empowerment are expected to stand out in the impetuous crypto market. This article will take stock of 5 projects in the current market with strong real income and are used for empowerment.

Hyperliquid: Transaction fee income for repurchase

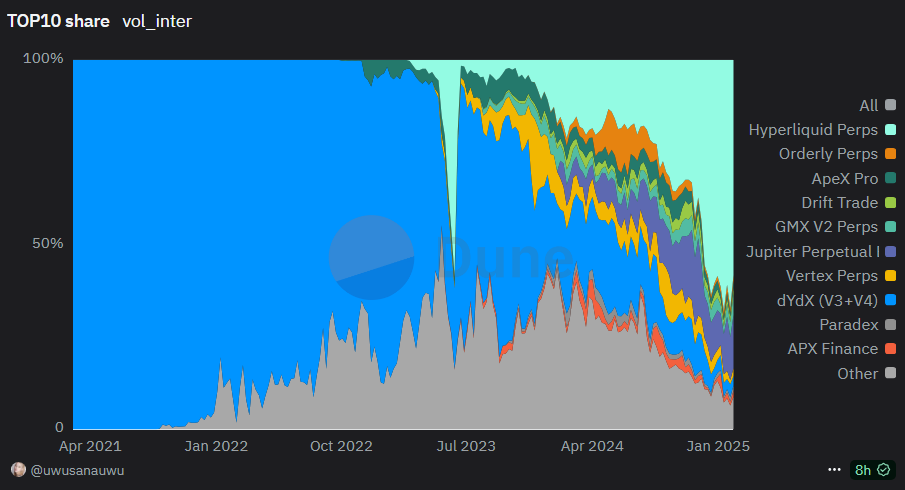

Hyperliquid is an on-chain Perpetual Contract Exchange and has launched the Dutch auction mechanism to obtain new spot seats. Hyperliquid's revenue mainly comes from contract transaction fees, HIP-1 auction fees, spot transaction fees and HLP MM PnL. Currently, Hyperliquid has become the largest derivatives exchange on the chain, with trading volume accounting for about 60% of the market share.

HYPE can be considered to have a double deflation mechanism. A portion of the Hyperliquid platform revenue (i.e., USDC fees) will be entered into the Hyperliquid Assistance Fund for HYPE-enabled repos. HypurrScan data shows that as of February 10, Hyperliquid Assistance Fund has spent about US$149 million to buy back 146.93 million HYPEs, accounting for 1.47% of the total, and has made floating profits of approximately US$194 million.

On the other hand, the supply will be reduced by destroying the HYPE in the transaction fee. The HYPE part of the HYPE/USDC spot transaction fee will be directly destroyed, which further reduces the supply in circulation. HYPEBurn data shows that as of February 10, 153,100 HYPEs have been destroyed in transaction fees.

Jupiter: More than just the diversified business system of aggregators

and 50% of the agreement revenue for repurchase

As Solana's largest DEX aggregator, Jupiter has almost no rivals in the aggregator field due to the popularity of Solana's on-chain market. DeFiLlama data shows that in the past 24 hours, Jupiter aggregation transaction volume reached US$3.224 billion, 7-8 times the number of OKX (about US$411 million).

Unlike other aggregators that started out but only made aggregator products, Jupiter is also actively expanding other businesses, including Jupiter Perp, DCA, Swap API and fiat currency channels, and the largest business revenue comes from Jupiter Perp. Although Jupiter Perp is much inferior to Hyperliquid in the multi-chain on-chain contract exchange market share, it is an absolute leader in the Solana network.

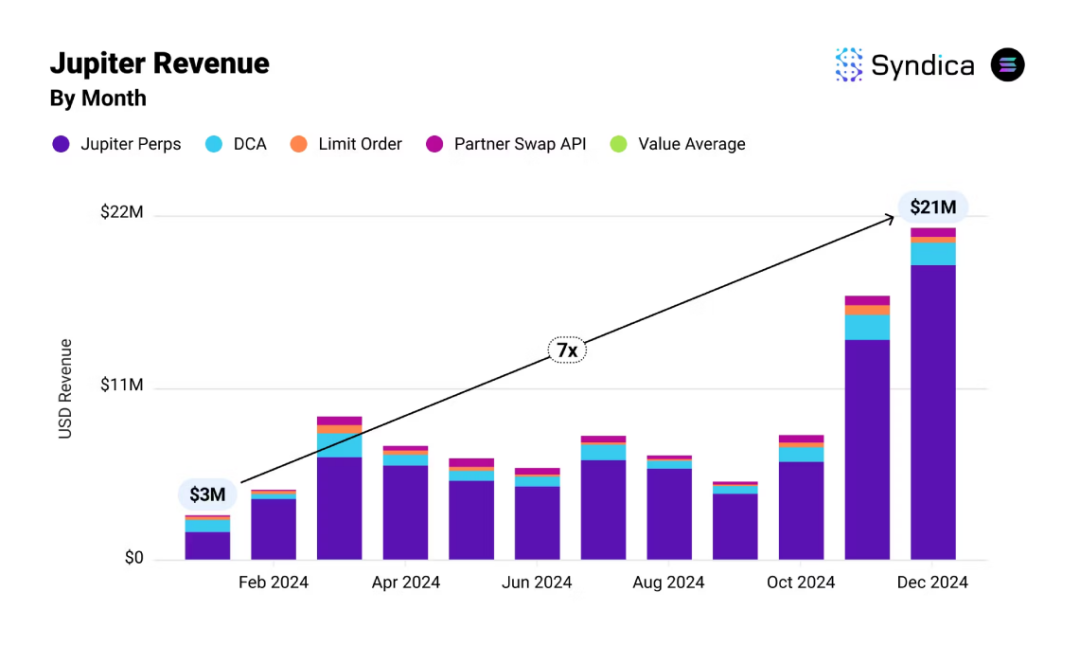

According to Syndica data, in December 2024, Jupiter's agreement revenue reached US$21 million, a record high, up more than 7 times compared with January of the same year; throughout 2024, Jupiter's agreement revenue reached US$102 million.

In late January this year, Jupiter officially announced that it would use 50% of the agreement revenue to repurchase JUP, which is equivalent to US$50.1 million per year for repurchase based on the full-year revenue in 2024.

Raydium: Solana Max DEX with 12% of each transaction fee for purchases

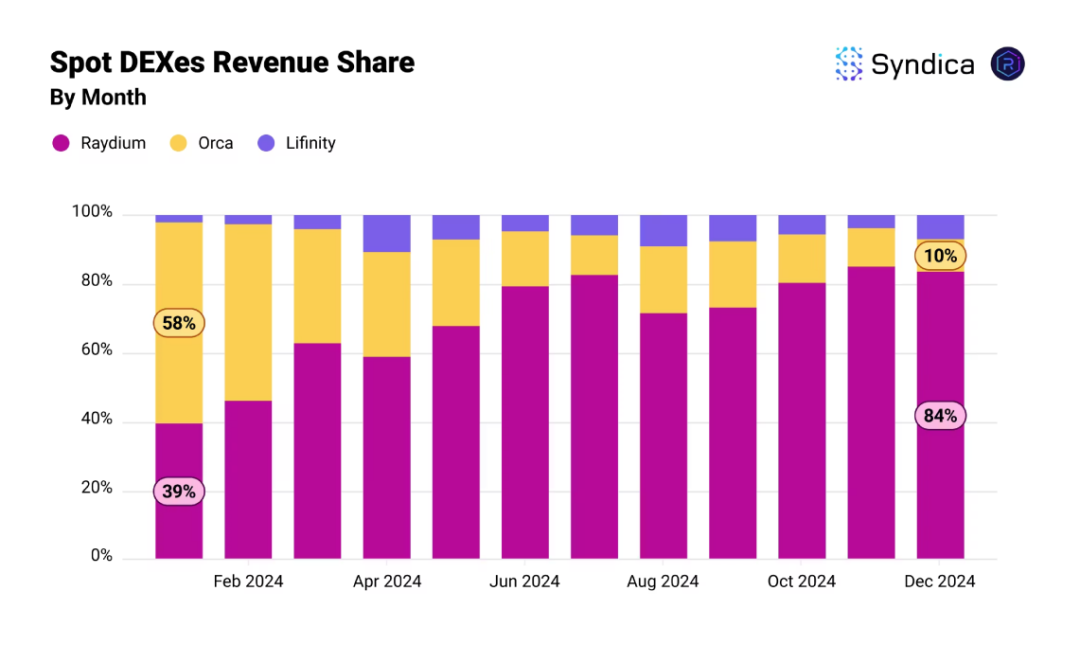

In the second half of 2024, Solana surpassed Ethereum DEX to become the most transaction-volume network on chain. Solana DEX trading volume exceeded US$630 billion in the full year of 2024, of which Raydium has an absolute leader with a market share of less than 40% at the beginning of the year to a market share of more than 80% in Q4.

Compared to Jupiter, Raydium's revenue model is much simpler. Each transaction in Raydium Pool requires a certain transaction fee. For example, the transaction fee for a standard AMM Pool is 0.25%, and the transaction fee for CLMM Pool is 0.01% - 2% in 8 different levels. Of the transaction fees collected, 84% were allocated to LP, 12% were used for RAY repurchases and 4% were taken to Treasury.

According to DeFiLlama data, Raydium captured approximately $664.4 million in 2024, equivalent to $79.728 million in fees for repurchases throughout the year.

GMX: AMM Perp represents dividends with pledge

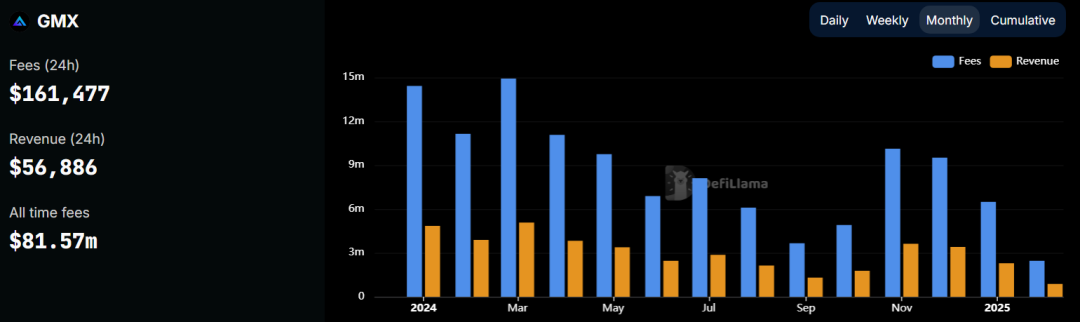

As one of the early on-chain derivatives exchanges, unlike the current mainstream order-blank model, GMX uses the automatic market maker model (AMM) for perpetual contract trading. Users provide assets (such as ETH, BTC, stablecoins) to GMX's GLP pool as a counterparty to GMX Traders. However, compared with the thin order model, AMM Perp is not suitable for running strategies and is more suitable for some low-frequency trading. Therefore, the characteristic of GMX is that its position is high but its daily trading volume is relatively low. Despite being challenged by order-thin Perp like Hyperliquid, DeFiLlama data shows that GMX still captured about $111 million in 2024, with more than $10 million in 5 months of capture.

Capturing 30% of fees from GMX V1 transactions and 27% of V2 will be rewarded for GMX stakeholders, which is calculated as full-year expenses for 2024, which is equivalent to approximately $30-33 million in fee dividends. In the current GMX circulation, 64% of GMX is pledged and is now worth approximately US$145 million.

Banana Gun: Challenged veteran TG trading robots and holders dividends

As one of the first Telegram robots to use vampire attacks, Banana Gun once captured nearly $9 million in a single month in March 2024, and once occupied more than 30% of the market share of the multi-chain network TG trading robot track . However, as the number of competitors in the TG trading robot track increased significantly, on-chain Meme trading shifted from Ethereum to Solana, and platform-type Meme trading tools such as BullX, Photon and GMGN formed a bouncer for TG Bot, Banana Gun market The share gradually dropped to 5%-10%.

Although the market share is declining, the on-chain transaction volume cake is expanding significantly. Therefore, as a veteran TG trading robot, Banana Gun, is still one of the most profitable applications in 2024. Banana Gun charges 0.5% for manual purchases and limit orders on Ethereum and 1% for automatic snipers and other chains on Ethereum. According to DeFiLlama data, Banana Gun's full-year expense revenue reached US$57.8 million in 2024.

BANANA holders entering Banana Gun via a recommendation link are only required to hold more than 50 BANAs in their wallet to automatically accumulate 40% of the distribution of Banana Gun transaction fees every 4 hours, which is equivalent to $23.12 million in 2024 revenue Allocated to the holder, in the form of ETH/SOL or BANANA, while the choice of BANANA comes from the repurchase of transaction fees in the secondary market.

Additionally, users who trade with Banana Gun receive a small amount of BANANA as a reward for cashback through Banana Bonus transactions. Letting traders become holders and letting holders become traders is the ecological circulation system Banana Gun is building for BANANA and TG Bot.

Currently, most on-chain agreements that are willing to share or repurchase agreements on the market are mostly related to asset transactions, including spot transactions, perpetual transactions and aggregation transactions, which shows that on-chain asset transactions can bring strong revenue and make the team motivated To empower, compared with the 0.02%-0.075% fee on centralized exchanges, there are many taxes on the chain that reach 1%.

jinse

jinse