Wall Street bosses have "reversed" one after another, angrily criticizing Trump's tariffs as "absurd"

Reprinted from panewslab

04/11/2025·19D

Wall Street billionaires have never been used to being excluded from the decision-making circle.

But they find themselves in some kind of embarrassing situation after U.S. President Trump ignores their calls to cancel their tariff plans. These financial tycoons fear that Trump's tariff policy could endanger the U.S. economy.

As losses in the U.S. stock markets rapidly expand, corporate giants have tried various ways—making calls, sending social media, or even a serious shareholder letter—to try to change Trump’s mind.

Just the second day after Trump announced the latest round of comprehensive tariffs, CEOs of several major banks, including JPMorgan Chase Jamie Dimon, held a private meeting with Commerce Secretary Howard Lutnick through a Washington lobby arrangement.

But three people familiar with the matter said Lutnick was not convinced to change his position.

Last weekend, Trump's main donors tried another strategy, calling White House Chief of Staff Susie Wiles and Treasury Secretary Scott Bessent to lobby. According to people familiar with the matter, these efforts also ended in vain.

By Monday, hedge fund billionaires — many of whom were high-profile supporters of Trump’s second term — began to publicly express their dissatisfaction.

"The global economy is falling due to bad math calculations," hedge fund manager William A. Ackman said on X on Monday morning. "The president's advisers need to admit their mistakes by April 9 and adjust their direction before making big mistakes."

Others have joined in calling for stronger rebuttal measures.

Andrew Hall, a billionaire oil trader who criticized Trump, praised Ackman for his courage to speak out on Instagram: "At least he is willing to change his stance and point out this stupidity. Where are the other 'financial giants'? Why don't they talk?"

There are indeed a few people speaking out, although the way is more tactful. JPMorgan CEO Dimon talked about the matter in a letter to investors Monday morning, saying the tariffs could dampen consumer and investor confidence and hinder economic growth. Dimon had affirmed tariff policies in the days after Trump's election, and although this time there was no warning of a serious recession, he said the turmoil "had made many people start thinking about the possibility of an economic recession."

Laurence D. Fink, chairman of investment giant BlackRock, spoke more directly at a lunch meeting at the New York Economic Club on Monday, warning: "The economy is weakening before our eyes."

When commenting on tariffs for the first time, Fink also predicted that consumers would feel the pain caused by tariffs, and used Barbie dolls as an example to illustrate that commodity prices may rise. "Most CEOs I've talked to would say we may be in recession right now," he told attendees.

This situation shocked financiers who once could influence the decisions of the two presidents. It is particularly disturbing that during Trump's first term, he often used the rise in U.S. stocks as a measure of success. "I'm not sure Wall Street can change the president's mind," said Robert Wolf, former UBS America chairman. "But hope his donors and friends at Mar-Lago will speak out about this wrong approach."

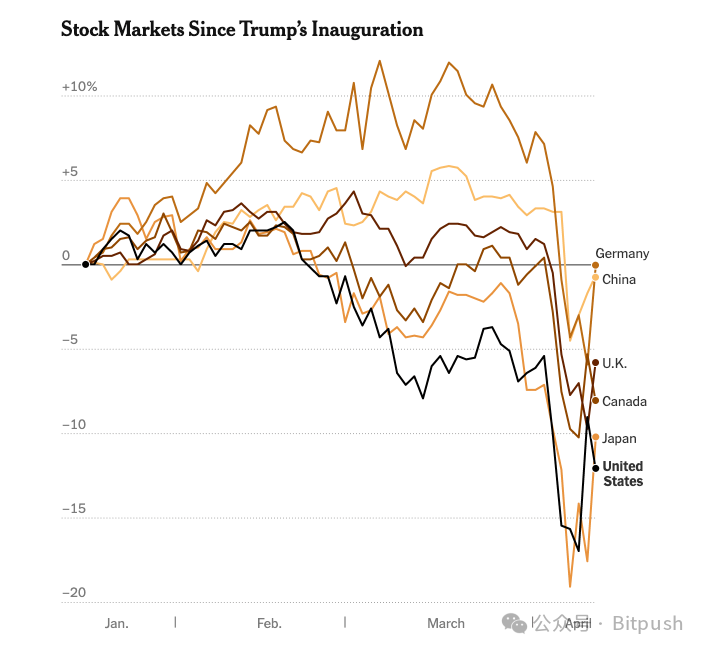

There was a brief moment on Monday morning, and Wall Street seemed to have moved Trump. A report about his plan to suspend tariffs has caused the stock market to turn from a sharp decline to a rise. But the S&P 500 eventually fell another 0.2% on the day after the White House denied the report and Trump reiterated his commitment to tariffs. The index closed on Monday down nearly 18% from its mid-February peak and was on the brink of a bear market.

Source: New York Times, data as of 4:20PM Eastern Time on April 10

"The Trump administration maintains regular communication with business leaders, industry groups and ordinary Americans, especially on major policy decisions like the reciprocal tariff action," White House spokesman Kush Desai said in a statement. "But the only special interest that guides President Trump's decisions is the best interest of the American people -- such as addressing problems caused by the long-term trade deficit."

The sale has scared Wall Street. Generally speaking, only a stable market means that businesses can continue to trade and banks can lend to businesses and consumers without worrying about default. As U.S. stocks have fallen at a rate not seen since the early days of Covid, Wall Street executives have been scrutinizing their customers and investments for early signs of a possible crisis.

A large investment bank is looking at whether it needs to reduce the value of its multi-billion-dollar loans to so-called investment-grade companies, often considered safe investments, before releasing its financial reports. Banks are scheduled to start releasing their latest earnings on Friday.

Another hot topic is the loan private equity market, which has rapidly expanded since the last major financial crisis in 2008, often involving financing for high-risk companies. Private lenders have long believed that any pressure on their systems will be under control, but these companies have never faced such a massive contraction.

While the concerns of Wall Street tycoons often seem to have nothing to do with the topics that ordinary people care about, the arguments made by financial executives to Trump include that his trade policy not only threatens the stock market but also endangers the U.S. economy.

The 2008 global financial crisis was triggered by a complex decline in the value of mortgage bonds, which eventually led to the collapse of the real estate market, and the impact lasted for many years. Many U.S. businesses rely on selling to countries that threaten to impose retaliatory tariffs.

When financiers talked to Trump administration officials in recent days, the response was that the White House focused on job reflux in industries such as manufacturing that have moved overseas. Trump administration officials said market turmoil could be a temporary disruption needed to achieve long-term change.

A well-known executive who acted as a middleman between Wall Street and Trump administration officials said he had begun telling colleagues and competitors that he would no longer try to convince Trump to postpone tariffs, but instead demanded a cut of tariffs for industries that had difficulty replacing imported goods quickly.

There are already signs that Wall Street has taken a hit. When some CEOs who met with Lutnick last week reconvened the call three days later, the focus of the discussion was not to convince Trump, but how to protect their banks from their decision-making, two people familiar with the matter said.

By Tuesday morning, even Ackman eased criticism, writing in another X post that he supported Trump's plan to use tariffs to eliminate "unfair trade practices." "But doing so without giving time to reach an agreement can cause unnecessary harm," Ackman added.

Note: This article is comprehensively compiled from the New York Times and does not represent the position of this platform.