Microstrategy’s Bitcoin Debt Cycle: A stroke of genius or a risky gamble?

Reprinted from jinse

01/13/2025·0MAuthor: Yohan Yun, CoinTelegraph; Compiler: Deng Tong, Golden Finance

MicroStrategy co-founder Michael Saylor has adopted an aggressive Bitcoin acquisition strategy that onlookers say is either a stroke of genius or a reckless gamble.

The latter warned that MicroStrategy 's heavy reliance on volatile assets such as Bitcoin is fraught with risks. A sharp decline in the price of Bitcoin could put pressure on a company's balance sheet, exacerbating financial stress and possibly impairing its ability to repay debt or raise additional capital.

Despite the risks, Saylor remains steadfast. The American entrepreneur said he had "no reason to sell the winner".

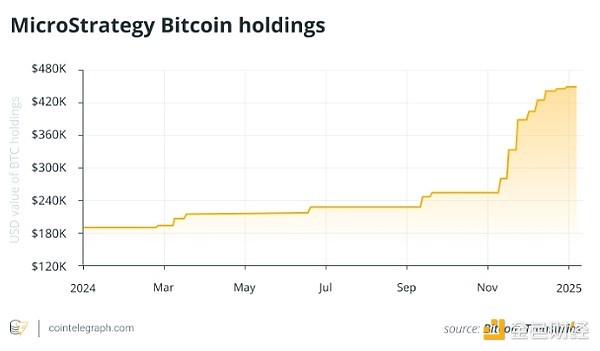

MicroStrategy is the world’s largest corporate Bitcoin holder, holding 447,470 Bitcoins at the time of publication. These huge holdings increase risks for the company and the entire Bitcoin ecosystem.

Fund MicroStrategy’s BTC purchases

MicroStrategy is nominally a business intelligence software company, but its aggressive Bitcoin accumulation means it is essentially a Bitcoin finance company.

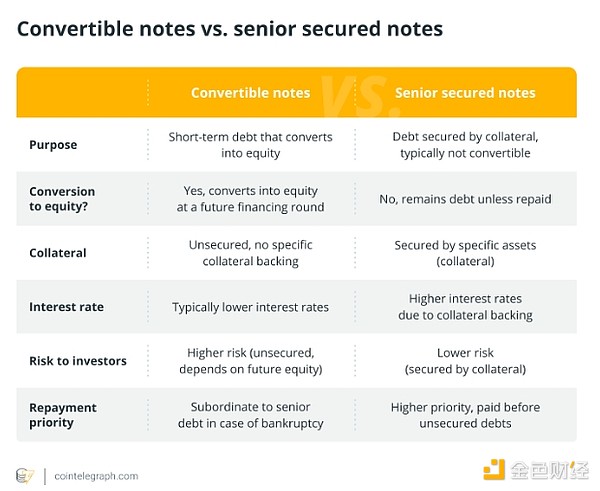

Saylor's Bitcoin buying spree began in August 2020 with a $250 million acquisition of the company's cash. He then turned to debt issuance, starting with convertible notes—debt that can be converted into equity. The notes, which often carry low interest rates, helped raise $650 million in December 2020 and subsequent issuances have raised billions more.

In June 2021, MicroStrategy issued $500 million in senior secured notes that offered a higher interest rate and were backed by the company's assets.

Most recently, on December 24, 2024, MicroStrategy proposed to increase its common shares from 330 million shares to 10.33 billion shares and its preferred shares from 5 million shares to 1.005 billion shares. The plan provides the flexibility to raise capital over time as needed, rather than issuing all new shares at once.

This is in line with the company’s 21/21 plan, which aims to raise $42 billion over the next three years – half through stock sales and half through fixed income instruments – to fund further Bitcoin purchases and explore the development of a crypto bank or Initiatives such as offering Bitcoin-based financial products.

A reckless Ponzi scheme?

David Krause, a finance professor emeritus at Marquette University, said Saylor's strategy was "inappropriate."

He warned that a sharp drop in Bitcoin prices could severely impact MicroStrategy (MSTR), eroding shareholder equity, jeopardizing debt repayments, and potentially leading to financial distress or bankruptcy, triggering a sell-off in its stock.

Krause said in a written statement: "As someone who has studied and taught corporate finance and investing for most of his career, and who served as a [chief financial officer] for more than a decade, I firmly believe that Treasury assets should Composed entirely of highly liquid and low-risk securities, such as money market instruments.”

MSTR trades essentially above the net asset value (NAV) of its Bitcoin holdings. On January 9, the company’s Bitcoin holdings accounted for 51% of its market capitalization, according to BitcoinTreasuries.net.

When MSTR trades above its Bitcoin net asset value, the company raises money through debt or equity to buy more Bitcoin. However, Kruger warned that this strategy could dilute shareholders.

In theory, this approach creates a cycle in which a company 's Bitcoin holdings boost its market position and stock price, leading to further debt issuance and the purchase of more Bitcoin.

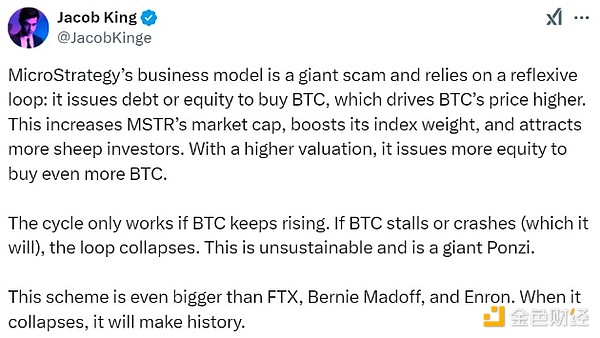

Some social media analysts liken this circular strategy to a Ponzi scheme.

Financial analyst Jacob King said: “This cycle will only work if BTC continues to rise. If BTC stagnates or collapses (which it will), the cycle will collapse. This is unsustainable and is A giant Ponzi scheme.”

Source: Jacob King

In a recent media interview, Saylor compared this approach to real estate practices in Manhattan.

“Like developers in Manhattan, every time property values go up, they issue more debt to develop more property,” he said. "That's why New York City's buildings are so tall, and it's been going on for 350 years. I call it the economy."

Kruger has been critical of MicroStrategy's reliance on Bitcoin, saying in a recent paper that it does not meet the SEC's official definition of a Ponzi scheme.

The securities regulator describes a Ponzi scheme as "an investment fraud that involves the payment of purported returns to existing investors out of funds invested by new investors."

Gracy Chen, CEO of cryptocurrency exchange Bitget, agreed with Kruger's analysis.

Unlike Ponzi schemes that rely on new investors ' money to pay returns to early investors, MicroStrategy's approach relies on market-driven appreciation in Bitcoin's value. "

Chen noted, “This strategy is more akin to de Gaulle’s challenge to the Bretton Woods system by converting dollars into gold. This is exploiting known weaknesses in modern monetary theory to profit from asset appreciation.”

Saylor’s Bitcoin blueprint is an undeniable success

As of the close of trading on January 8, MSTR shares were trading at $331.70, up approximately 2,200% since the company’s first Bitcoin purchase on August 11, 2020, when it closed at $14.44. During the same period, the price of Bitcoin increased by approximately 735%.

Whether one agrees with Saylor or not, his plan has undoubtedly boosted MicroStrategy's cryptocurrency portfolio and stock performance, allowing the company to become a member of the Nasdaq 100 Index in December.

While shareholders may face dilution, proponents argue that Bitcoin 's long- term growth potential offsets these risks. Additionally, Chen noted that MicroStrategy's convertible debt structure could serve as a protective buffer during a crisis.

" A prolonged bear market could expose the company to liquidity challenges and heightened debt management risks. However, its unsecured convertible debt structure provides some protection from immediate forced liquidation," Chen explained.

The company's approach to raising capital through stock offerings further reduces the risk of selling its Bitcoin holdings, even during a bear market. "

Bitcoin Exit Strategy

In short, MicroStrategy's mission is simple: keep buying Bitcoin.

The asset is a long-term strategic holding as a hedge against economic uncertainty and as a means to enhance shareholder value. It can also be used to obtain loans or raise funds for future business opportunities without liquidating their Bitcoins.

“It is possible to profit from Bitcoin’s massive liquidity pools,” said Alexander Panasenko, head of product management at VixiChain. “When you hold a lot of liquidity in this inflation-proof asset that actually stores value, you can make money just by holding it, borrowing against it.”

Critics, however, point out that Saylor lacks a clear exit strategy. Bitcoin maximalists believe that Bitcoin is the ultimate exit from the traditional financial system and therefore believe that Bitcoin is unnecessary.

Stock dilution remains a looming issue, but the strategy has largely benefited MicroStrategy and the broader Bitcoin ecosystem, inspiring imitators around the world.

“As long as [MicroStrategy] continues to spark discussions about the role of digital assets in the future economy, you’ll see new companies adopting it more broadly, revealing new strategies for leveraging digital assets... which is really good,” Panasenko said .

“If proposals like this involving digital assets fail, it casts a pall over the entire industry and basically sets us back.”