TRUMP and the hyper-financialization of society

Reprinted from jinse

01/22/2025·3MAuthor: Jasper De Maere, researcher at Outlier Ventures; Greysen Cacciatore, associate researcher at Outlier Ventures; Compiler: 0xjs@金财经

Key points of this article:

-

The $Trump token embodies the convergence of politics, finance, and culture, confirming the mainstream relevance of cryptocurrencies. It emphasizes that the financialization of non-financial assets is a cultural phenomenon that reshapes the social structure.

-

Financialization, which has dominated businesses for decades through derivatives and securitization, is now spreading to individuals and culture through tokens.

-

We believe there are three drivers behind hyperfinancialization and finance becoming a core part of culture . They are:

-

Technology – The digital revolution has made financial markets accessible and innovative.

-

Education – Younger generations are the most financially literate.

-

Spirituality – In today’s zeitgeist, financial success determines personal and professional fulfillment.

-

The President of the United States issues TRUMP tokens

The net impact of the $Trump token on the broader ecosystem is unclear, and the president-elect’s launch of the memecoin just days before his inauguration is notable to say the least. It represents a momentous moment at the intersection of politics, finance and culture. It solidifies the token’s status as a new liquid asset class and a vehicle for engagement, fundraising and building influence at the pinnacle of global influence.

In addition to confirming the mainstream relevance of cryptocurrencies, this move also highlights that the increasing financialization of non-financial assets is a profound cultural phenomenon . By turning intangible concepts like identity, community and influence into tokenized assets, it demonstrates how tokens intertwine finance, technology and culture. This marks a transformative moment that redefines the fabric of society and how we engage with value.

We call this hyperfinancialization, and we explore it in detail in our recent research on the Post Web. In the post-network world, improvements in technology and financial infrastructure will enable greater financialization of personal assets, making them more liquid and profitable. This will fundamentally reshape how value is stored, captured and utilized.

not the first time

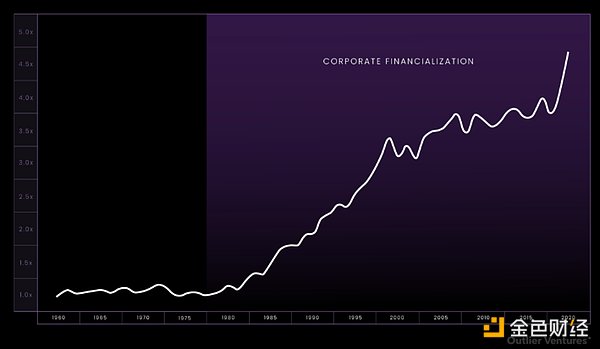

We have seen financialization happen in business before. Over the past 40 years, financialization has transformed economies by transforming corporate balance sheets into engines of speculative value. In the 1980s, deregulation and tools such as derivatives, securitization, and global credit markets enabled companies to unlock value from financial engineering rather than production. As companies increasingly use financial instruments to maximize shareholder returns, non-bank financial assets have soared from 40% to over 200% of GDP (see Figure 1). This shift marks the dawn of a new era in which the economy is driven less by tangible goods and services and more by the monetization of abstract financial assets.

Figure 1: The assets of U.S. non-bank financial institutions as a proportion of GDP

Similar to companies, individuals have a balance sheet (i.e. their property). Tokens and cryptocurrencies are now bringing financialization to the consumer level. Just like derivatives and securitization in the 1980s, innovations like tokenization and DeFi enable individuals to extract more value from their assets. However, unlike the 1980s, cryptocurrencies go further, merging finance and culture, and like memecoins, tokens can represent identity, community and participation. However, much like derivatives, these new instruments in the form of tokens come with inherent risks, which we are witnessing firsthand as the frameworks for managing these risks continue to evolve.

Spirituality, Education and Technology

The following sections in Chapter 2 of “The Post-Internet Era” set out what we consider to be the key drivers behind hyperfinancialization.

The financialization trend of daily items is becoming increasingly obvious. We call this phenomenon “hyperfinancialization”. This socio-cultural shift enables assets not traditionally considered financial, especially intangible assets, to be quantified in monetary terms and leveraged for maximum financial gain. This trend towards monetizing everyday assets will drive the adoption of blockchain technology. These assets become more economically efficient through tokenization, providing attractive returns on investment.

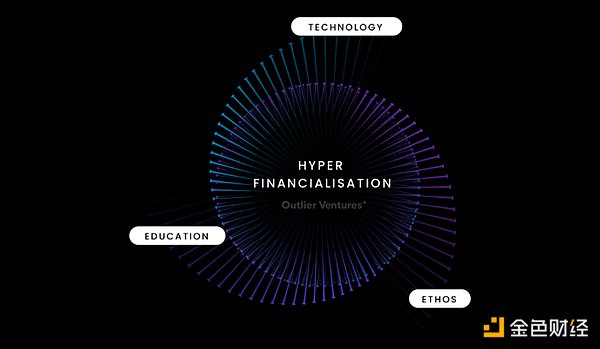

We believe there are three key drivers behind today’s hyper-financialization, namely (i) education (ii) spirituality and (iii) technology (shown below).

Figure 2: Three major driving factors of social hyper-financialization

Source: Outlier Ventures

1. Education

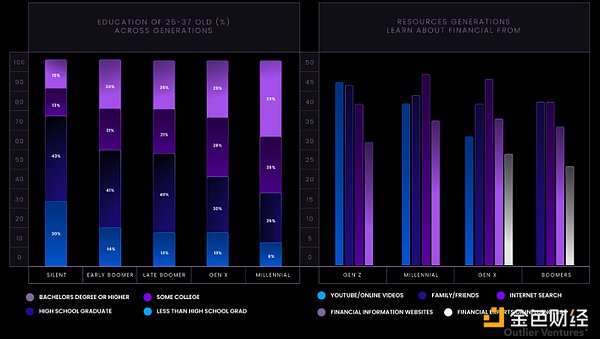

Education equips individuals with the knowledge to understand financial markets and their importance. Today’s younger generations, especially Generation Z and Alpha, are among the most financially literate in history, thanks to their early exposure to digital technology and “DIY” online resources. LLMs and agents further close the financial literacy gap, allowing individuals in any language around the world to be educated to make informed decisions about saving, investing, and managing debt or assets, which we believe is setting the stage for the rise of the “100x individual” and the global population The improvement of civilization level paved the way.

Figure 3: Left – Comparison of education levels across generations. Right – Sources of education across generations.

Source: Pew Research Center, Outlier Ventures

2. Spirit

Ethos, or the collective values of a generation, shapes the desire to participate in financial markets. In today's zeitgeist, financial success is closely linked to personal and professional achievement. Society's evaluation of financial success drives the desire to explore and participate in financial opportunities. The spirit of pursuing financial success encourages the financialization of assets owned, maximizing the financial potential of one's assets. We are entering an era of extreme capitalism, where financialization will permeate every aspect of our lives more than ever before.

3. Technology

Technology is critical, bridging the gap between financial knowledge, willingness to participate, and actionable financial opportunities. The digital revolution has made financial markets and assets more accessible, allowing individuals to participate freely. Not only are financial applications democratizing access to financial markets, but the underlying technologies are changing the types of financial products we offer and abstracting away the complexity of financial products.

Technology is changing financial markets in three interconnected ways

1. Democratic access

The democratization of financial services has changed the financial landscape, making financial tools and platforms widely available and lowering the threshold for individual and non-qualified investors. This trend promotes financial inclusion, expands market participation, and rapidly expands the addressable market for financial products.

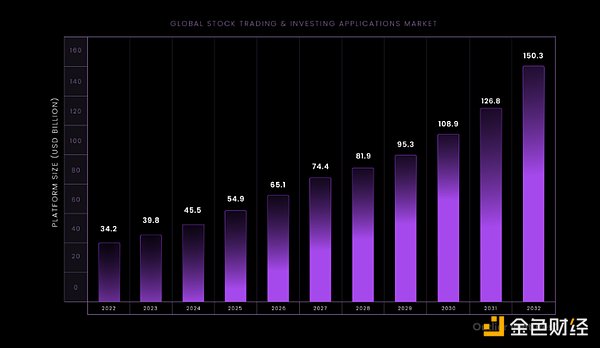

Figure 4: TAM (total addressable market size) for stock trading and investing. Growth in TAM means an increase in service activity and number of users.

Source: Vision, Outlier Ventures

2. New financial products

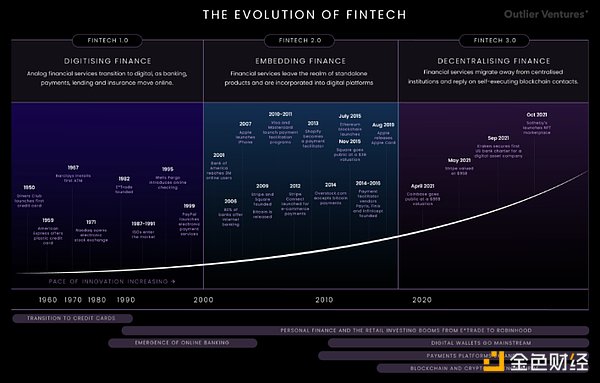

Technology gives investors access to more sophisticated services and markets. For example, blockchain-based systems unlock decentralized and tokenized finance, revolutionizing the way individuals manage financial assets. The intersection of technology and finance drives innovation in consumer finance and investment products.

Figure 5: Timeline of the evolution of fintech over the past 60 years, showing the exponential growth of financial services and products due to the development of technology.

Source: SVB, Outlier Ventures

3. Complexity abstraction

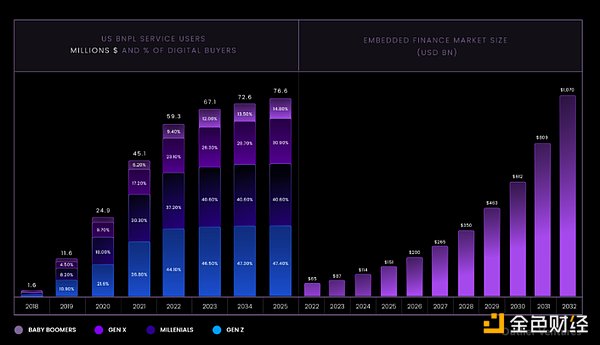

Abstraction is driving the popularity of new financial products, making consumer finance and investing more intuitive for ordinary users through technologies such as complex algorithms, robo-advisors, and AI-driven platforms. This simplification is driving rapid growth in the adoption of financial services and investment opportunities, exemplified by trends such as embedded finance and buy now, pay later. Figure 6 shows that more sophisticated products such as BNPL are being adopted primarily among the younger, tech-savvy generation.

Figure 6: Adoption of BNPL and embedded finance shows rapid adoption.

Source: Insider Intelligence, Outlier Ventures

As a result, transaction volumes in the modern economy are evolving rapidly. In addition to being hyper-financialized, society is also becoming increasingly transactional. Digitization allows for more granular transactions, thereby changing the way we pay for services. For example, as digital platforms improve payment tracking, software evolves from upfront purchases to subscription models. Distributed ledger technology is another upgrade that enables Web3 services such as DePIN to implement a pay-as-you-go model.

Hyper-financialization in the post-internet era

As hyperfinancialization accelerates in the post-internet era, addressing gaps in financial knowledge and execution will become critical. People with these two skills will participate in the economic cycle, increase wealth, and actively participate in the tokenized economy as shareholders. With the large- scale tokenization of assets, LLM and agents play a transformative role in the post-network era, creating a level playing field by equipping everyone with basic financial knowledge and participation. These tools enable individuals to manage and leverage their tangible and intangible assets, ensure broader access to economic opportunity, and mitigate wealth and knowledge gaps.

panewslab

panewslab