Usual's bonds are destabilized, will the new stablecoin star fall?

Reprinted from panewslab

01/10/2025·1MBy Pzai, Foresight News

As a recent hot narrative, RWA stablecoin, backed by the natural growth of off-chain assets, has introduced a source of vitality to the stablecoin field and opened up enough room for imagination for investors. One of the representative projects, Usual, has also gained favor from the market, and TVL of over US$1.6 billion has quickly poured into it. But the project has encountered certain challenges recently.

On January 9, the liquid staking token USD0++ in its project suffered a sell-off after Usual’s announcement. In the RWA stablecoin camp, some players are also experiencing varying degrees of de-anchoring, which also reflects changes in market sentiment. This article analyzes this phenomenon.

Mechanism changes

USD0++ is a liquid pledged token (LST) with a pledge period of 4 years, similar to a "4-year bond". For each USD0 pledged, Usual will mint new USUAL tokens in a deflationary manner. And distribute these tokens to users as rewards. In Usual’s latest announcement, USD0++ will switch to a lower limit redemption mechanism and provide conditional exit options:

- Conditional withdrawal: 1:1 redemption, requiring forfeiture of part of USUAL earnings. That part is scheduled to be released next week.

- Unconditional exit: redeem at the floor price (currently set at $0.87), and gradually converge to $1 over time.

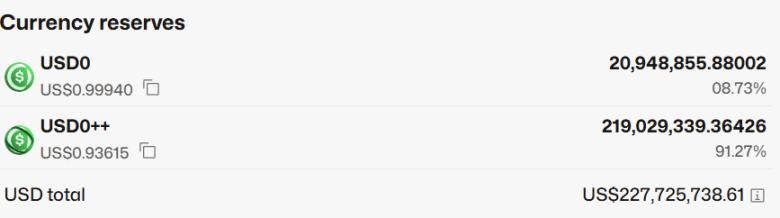

In the volatile environment of the crypto market, fluctuations in market liquidity (for example, RWA's underlying asset - U.S. Treasury bonds have been discounted in recent fluctuations) and the implementation of the overlay mechanism have poured cold water on investors' expectations, USD0/ The USD0++ Curve pool was quickly sold wildly by investors, with the pool offset reaching 91.27%/8.73%, and the USD0++/USD0 lending pool APY on Morpho also soared to 78.82%. Before the announcement, USD0++ had maintained a premium over USD0 for a long time. This may be due to the fact that USD0++ provided a 1:1 early exemption option during Binance’s pre-market trading period, maximizing airdrop benefits for users before the protocol was launched. After the mechanism was clarified, investors began to flow back into the more liquid local currency.

This incident had a certain impact on the holders of USD0++, but most of the holders of USD0++ were motivated by USUAL, held for a long time, and the price fluctuations did not fall below the floor price, which was reflected in panic selling.

Perhaps affected by this incident, USUAL also fell to $0.684 as of press time, a 24-hour drop of 2.29%.

Fluctuation gradually

From a mechanism perspective, USUAL will have a process of anchoring its income to USD0++ through USUAL tokens in the future (burning USUAL will boost the currency price, increase yields and attract liquidity backflow), while the RWA stablecoin will "pull" liquidity. In the process of "new", the role of token incentives itself is also self-evident. The mechanism of USUAL is to reward the entire stablecoin holder ecosystem through USUAL tokens and anchor them while maintaining stable gains. In a volatile market, investors may need more liquidity to support their positions, further exacerbating the volatility of USD0++.

In addition to Usual, another RWA stablecoin Anzen USDz has also experienced a long-term de-anchoring process. After October 16 last year, the token continued to experience a wave of selling, possibly due to the impact of airdrops, and once fell below $0.9, weakening the Potential earnings for investors. In fact, the Anzen protocol also has functions similar to USD0++, but the overall pledge scale is less than 10%, which has limited impact on selling pressure. Its single pool liquidity is only US$3.2 million, which is far inferior to the nearly US$100 million USD0 liquidity in a single pool in Curve. Sexually generous.

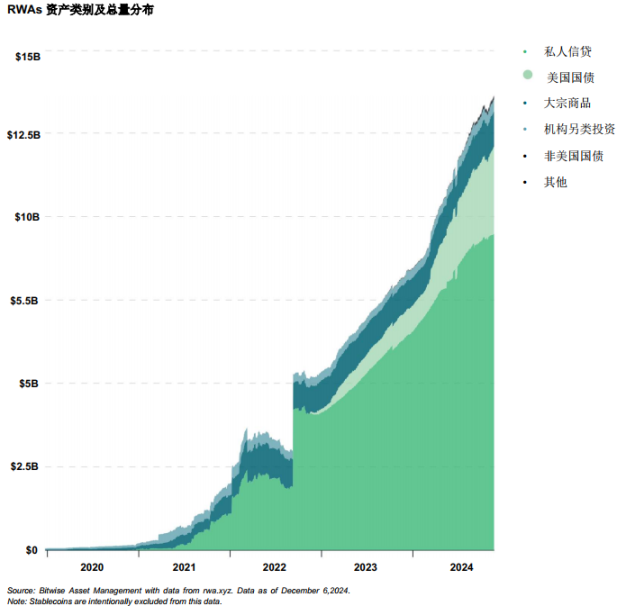

In terms of business model, RWA stablecoin also faces many problems, including how to balance the relationship between token issuance and liquidity growth, how to ensure the growth of real income and synchronization with the chain, etc. According to Bitwise analysis, most of the assets of RWAs are U.S. Treasury bonds, and the single asset distribution has also caused stablecoins to be partially impacted by U.S. Treasury bonds. How to resist them through mechanisms or reserves has become a direction worth thinking about.

For stablecoin projects, they seem to have once again fallen into the cycle of “mining, selling, and withdrawing” during the DeFi Summer period. Although this model can attract a large number of users and capital inflows through high token incentives in the short term, it does not essentially Solving the problem of long-term value creation of the protocol will easily lead to the continued decline of token prices due to excessive selling pressure, ultimately damaging user confidence and the healthy development of the project ecosystem.

To break this cycle, project parties need to focus on the long-term construction of the ecosystem and gradually build a diversified and sustainable stablecoin ecosystem by developing more innovative products, optimizing governance mechanisms, and strengthening community participation, rather than relying solely on short-term incentives. Attract users. Only through these efforts can stablecoin projects truly break the cycle of “mining, selling, and withdrawing” and bring users tangible real income and strong liquidity endorsement, thereby standing out in the fiercely competitive market and achieving long-term development.