Encrypted VC relationship network map: What are the hidden rules for crypto investment

Reprinted from jinse

04/18/2025·10DAuthor: Decentralised.Co; Translation: Golden Finance xiaozou

As an asset class, venture capital always follows an extreme power law distribution. But because we are always tired of chasing the latest narrative, the specificity of this distribution has never been studied in depth. Over the past few weeks, we have developed an internal tool to track the network relationships of all crypto venture capital firms. Why do this?

The core logic is simple: As an entrepreneur, understanding which venture capital institutions often invest together can save time and optimize financing strategies. Each transaction is a unique fingerprint, and when we visualize this data, we can interpret the story behind it.

In other words, we can track key nodes in the crypto space that dominate most of the financing activities. It is like finding hub ports in a modern trade network, which is no different from the nature of merchants looking for trade strongholds a thousand years ago.

We conducted this experiment for two reasons:

First, we run a venture capital network similar to "fighting clubs" - although no one has hit each other, we rarely discuss it publicly. This network covers about 80 funds, while only 240 institutions in the entire crypto venture capital sector invest more than $500,000 in the seed stage. This means we have direct contact with one-third of market participants, and nearly two-thirds of practitioners read our content. This influence is far beyond expectations.

However, tracking the actual flow of funds has always been difficult. Sending project progress to all funds will cause information noise. This tracking tool came into being, it can accurately screen which funds have invested, which tracks they have laid out, and who their partners are.

In addition, for entrepreneurs, mastering capital trends is only the first step. What is more valuable is understanding the historical performance of these funds and their usual joint investment partners. For this reason, we calculated the historical probability of fund investment obtaining subsequent financing - but this data will be distorted in later rounds (such as round B), because project parties often choose to issue coins instead of traditional equity financing.

Helping entrepreneurs identify active investors is only the first stage. Next, we need to find out which sources of capital really have advantages. Once we obtain this data, we can analyze which funds' joint investments can bring the best results. This is certainly not Rockets science, just like no one can guarantee marriage on a first date, and no venture capital can ensure that the project enters the A round with just a check. But understanding the rules of the game in advance is just as important for financing and dating.

1. Successful architecture

We use basic logic to screen out funds with the highest subsequent financing rate of the investment portfolio. If multiple projects invested by a fund can obtain new financing after the seed round, it means that its investment strategy is indeed unique. When the invested company completes the next round of financing at a higher valuation, the book returns of venture capital will also increase, so the subsequent financing rate is a reliable indicator to measure the performance of the fund.

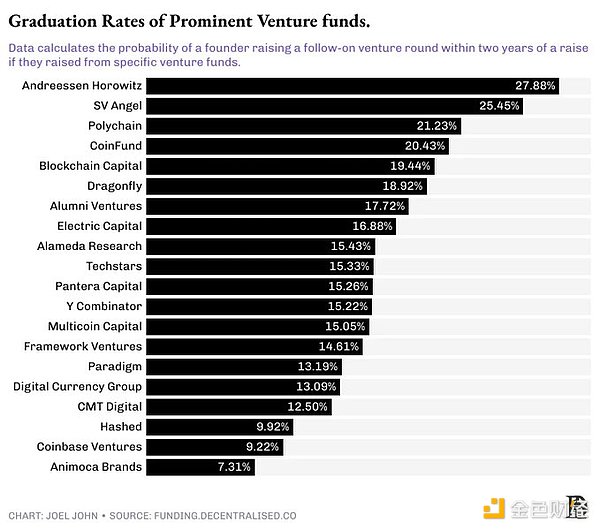

We selected the 20 funds with the largest number of subsequent financing for the portfolio to count their total investment cases in the seed stage. From this, the percentage of probability that the entrepreneur can obtain subsequent financing can be calculated. For example, a certain fund invests in 100 seed projects, 30 of which receive new financing within two years, and its "graduation rate" is 30%.

It should be noted that we strictly limit the two-year observation period. Many startups may choose not to raise funds, or to raise funds later.

Even among these top 20 funds, the power law effect is still amazing. For example, if a project that accepts a16z investment, the probability of obtaining subsequent financing within two years is 1/3 - that is, one of every three start-ups invested in a16z investment can enter the A round. Considering that the probability of the last-ranked fund is only 1/16, this result is quite impressive.

Funds ranked close to 20 on this list have a subsequent financing rate of about 7%. These numbers seem to be close, but specifically: the probability of 1/3 is equivalent to the number of points less than 3 when rolling the dice, while the probability of 1/14 is comparable to the birth of twins - this is a completely different magnitude.

No matter how much jokes are, the data truly reveals the agglomeration effect of the crypto venture capital field. Some funds can actively design follow-up financing for invested projects because they operate growth-term funds at the same time. This type of institution participates in both the seed round and the A round. When venture capital continues to raise the same project, it will usually send positive signals to investors in subsequent rounds. In other words, whether a growth-term fund is installed within a venture capital organization will significantly affect the future success probability of the invested companies.

The ultimate form of this model will be the gradual evolution of crypto venture capital into private equity investment in mature income-generating projects.

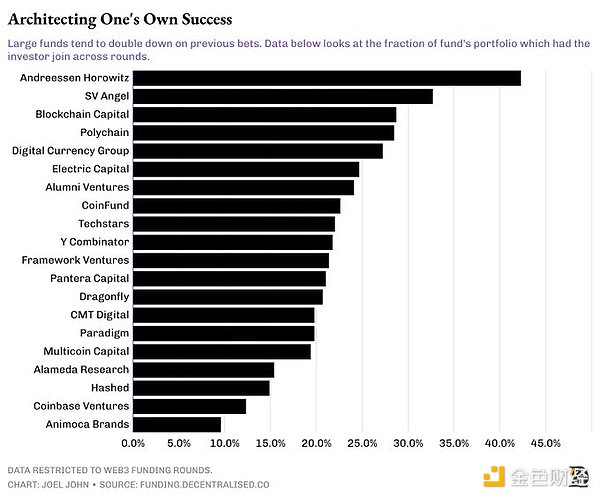

We have made theoretical remarks about this transformation. But what exactly does the data reveal? To explore this question, we counted the number of startups in the portfolio that received subsequent financing and calculated the probability of the same venture capital institution participating in subsequent rounds.

That is to say, if a company obtains seed round financing from a16z, how likely is it to participate in its A round financing?

The law soon emerged: large funds with management scale of over $1 billion tend to follow up frequently. For example: 44% of the projects in the a16z portfolio that receives subsequent financing will continue to invest; Blockchain Capital, DCG and Polychain will invest additional investments in 25% of the projects that receive renewal.

This means: it is much more important to choose investors in the seed round or Pre-Seed round because these institutions have a significant "repeated investment preference".

2. Inertial joint investment

These rules are a summary after the fact. We are not suggesting that projects that are not favored by top venture capitalists are doomed to fail—all economic behavior is essentially growth or profit, and businesses that achieve either goal will eventually receive a revaluation of value. But why not if the probability of success can be increased? If you cannot directly obtain investments from the top 20 funds, reaching the capital hub through their network contact is still a feasible strategy.

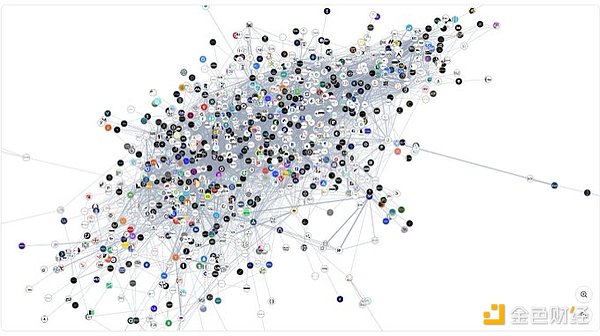

The figure below shows the network map of all venture capital institutions in the crypto field over the past decade: 1,000 investment institutions have formed a connection through approximately 22,000 joint investments. There are many choices on the surface, but it should be noted that this includes funds that have stopped operating, have not achieved returns or have suspended investment.

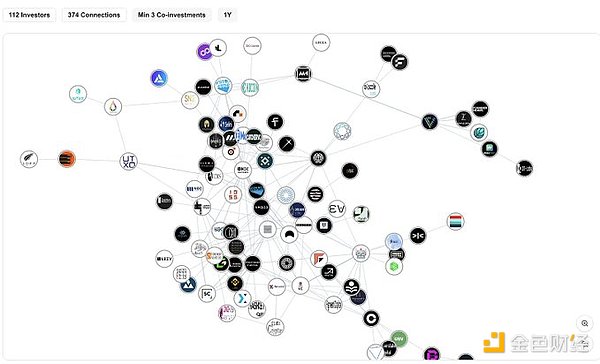

The real market structure is clearer in the figure below: only about 50 funds can make a single A round investment of more than US$2 million; the investment network participating in such rounds covers about 112 institutions; these funds are accelerating their integration, showing a strong preference for specific combined investment.

Over time, funds seem to develop stable joint investment habits. That is, funds investing in an entity tend to attract peer funds because of skills complementarity (such as technology assessment/market expansion) or based on partnerships. To study how these relationships work, we began exploring the model of co-investment among funds last year.

By analyzing the combined investment data from the past year, we can see:

Polychain and Nomad Capital have 9 shots together;

Bankless and Robot Ventures scored 9 times;

Binance, Polychain and HackVC each made 7 shots;

OKX and Animoca made 7 shots together.

The screening of leading funds for joint investors is becoming increasingly stringent:

Paradigm's 10 investments last year were jointly invested with Robot Ventures;

DragonFly invested 3 times in 13 investments, with Robot Ventures and Founders Fund;

Founders Fund joined forces with Dragonfly three of its nine investments.

This shows that the market is turning to "oligopoly investment" - a few funds bet with larger chips, and most of the joint investors are old and well-known institutions.

3. Matrix Analysis

Another research method is to use the behavior matrix of the most active investors. The above chart counts the fund relationship network with the highest investment frequency since 2020. It can be seen that: accelerators are unique, and although accelerators such as Y Combinator are frequently invested, they have very few joint investments with exchanges or large funds.

On the other hand, you will find that exchanges also have specific preferences. For example, OKX Ventures and Animoca Brands maintain a high- frequency joint investment relationship. Coinbase Ventures and Polychain jointly invested more than 30 times, and also had 24 joint investment records with Pantera.

The structural laws we observe can be summarized into three points:

*Accelerators tend to be rarely co-invested with exchanges or large funds, although they are invested frequently. This may be due to stage preference.

-

Large exchanges tend to have a strong preference for risky funds in growth stages. Currently, Pantera and Polychain dominate this.

-

Exchanges tend to cooperate with local institutions. OKX Ventures and Coinbase's preferences for joint investment targets are different, highlighting the global nature of capital allocation in the Web3 era.

Since venture capital is aggregating, where will marginal capital come from? An interesting phenomenon is the self-construction system of corporate capital: Goldman Sachs has only invested twice with PayPal Ventures and Kraken in history, while Coinbase Ventures and Polychain have invested 37 times, Pantera has invested 32 times, and Electric Capital has 24 times.

Unlike traditional venture capital, corporate capital usually targets growth- term projects with product market fit. At a time when early financing shrinks, the behavior patterns of this type of capital are worthy of continuous observation.

4. Dynamically evolved capital network

After reading Neil Ferguson 's "Platforms and Towers" a few years ago, I came up with the idea of studying networks in the field of encryption. The book reveals that ideas, products and even disease transmission is related to network structure, but it was not until we developed a financing data board that the visualization of the crypto-capital network was truly realized.

This type of data set can be used to design (and execute) mergers and acquisitions and token privatization solutions - this is the direction we are exploring internally and can also assist in business cooperation decision- making. We are looking at how to open data access to specific institutions.

Back to the core question: Can network relationships really improve fund performance? The answer is quite complicated.

The core competitiveness of a fund is increasingly determined by the ability and fund size of the screening team, rather than simply network resources. But the personal relationship between the general partner (GP) and the co-investor is indeed crucial - the venture capital sharing project flow is based on interpersonal trust rather than institutional brands. When a partner changes job, his or her relationship network will naturally move to his or her new owner.

A 2024 study validated this hypothesis. The paper analyses the 38,000 investment rounds of 100 top VCs and draws key conclusions:

*Historical joint investment does not guarantee future cooperation, and failure cases will disrupt inter-agency trust.

*The joint investment surged during the fanatical period, and funds relied more on social signals rather than due diligence in the bull market; they tended to be alone in the bear market, and funds tended to invest independently when valuations were sluggish.

*Principle of Complementary Capabilities: Homogeneous investors often predict risks.

As mentioned above, in the end, joint investment does not happen at the fund level, but at the partner level. In my own career, I have seen people jumping between different organizations. The goal is usually to work with the same person, regardless of what fund they join. In an era when artificial intelligence replaces human power, interpersonal relationships remain the basis for early venture capital.

There are still a lot of gaps in this research on crypto venture capital networks. For example, the liquidity allocation preferences of hedge funds, how growth-term investments adapt to market cycles, and intervention mechanisms for mergers and acquisitions and private equity, etc. The answer may be hidden in the existing data, but it will take time to extract the correct question.

panewslab

panewslab