The Secret Gold Mine of Stablecoins: How to Profit from U.S. Treasury Bonds and Interest Rates?

Reprinted from chaincatcher

04/19/2025·9DOriginal title:How Stablecoins Profit From US Debt & Interest Rates

Original author: Three Sigma

Original translation: zhouzhou, BlockBeats

Editor 's note: This article explores how stablecoins such as USDT and USDC generate billions of dollars in revenue by investing reserves in U.S. Treasury bills, which are closely related to Fed interest rates. If interest rates drop to zero, their profitability may plummet. As USDC demonstrated in the 2023 Silicon Valley Banking Event, fiat-backed stablecoins face regulatory challenges and risk of decoupling, while algorithmic stablecoins like USDe rely on crypto-native yields, which makes them less sensitive to interest rate changes. Tether’s $20 billion equity secured a decades-long runway, but Circle’s $1.68 billion revenue and limited liquidity in 2024 make it vulnerable to only 18-25 months of sustainability.

The following is the original content (to facilitate reading comprehension, the original content has been compiled):

1. The transformation of cryptocurrency to stability

Initially, Bitcoin was seen as an alternative to traditional currencies, a decentralized, borderless, censor-resistant form of currency. However, due to its high volatility (significant price volatility), gradually evolved into speculative assets and store of value, and the high transaction costs of blockchain, it is no longer suitable as a daily payment tool or a stable store of value.

This limitation has prompted the rise of stablecoins. Stablecoins are designed to maintain fixed value, often pegged to the US dollar, providing transaction stability and efficiency that Bitcoin cannot achieve.

The development of the crypto ecosystem reflects a pragmatic transformation. Although Bitcoin’s initial ideal was to replace traditional currencies, the demand for stability has enabled stablecoins (usually backed by traditional assets) to be widely used and become the backbone of the entire ecosystem.

These stablecoins serve as bridges between the traditional financial markets in the real world and the crypto ecosystem. On the one hand, they promote the popularization and application of cryptocurrencies, and on the other hand, they have also aroused people's doubts about the ideal of crypto decentralization. For example, stablecoins like Tether (USDT) and USD Coin (USDC) are issued by centralized institutions, whose reserve assets are stored in traditional banks, which is believed to have made some kind of compromise between ideas and reality.

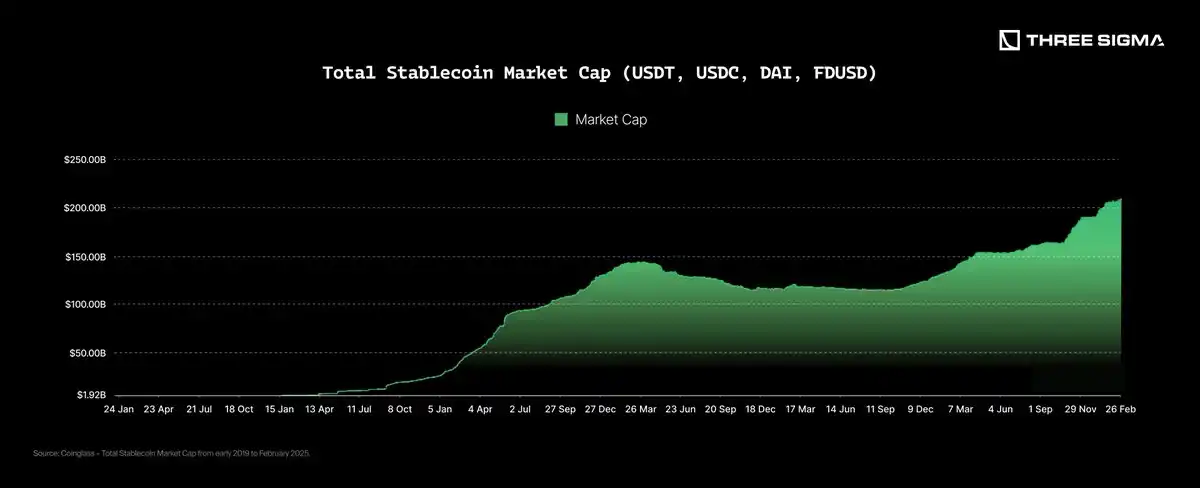

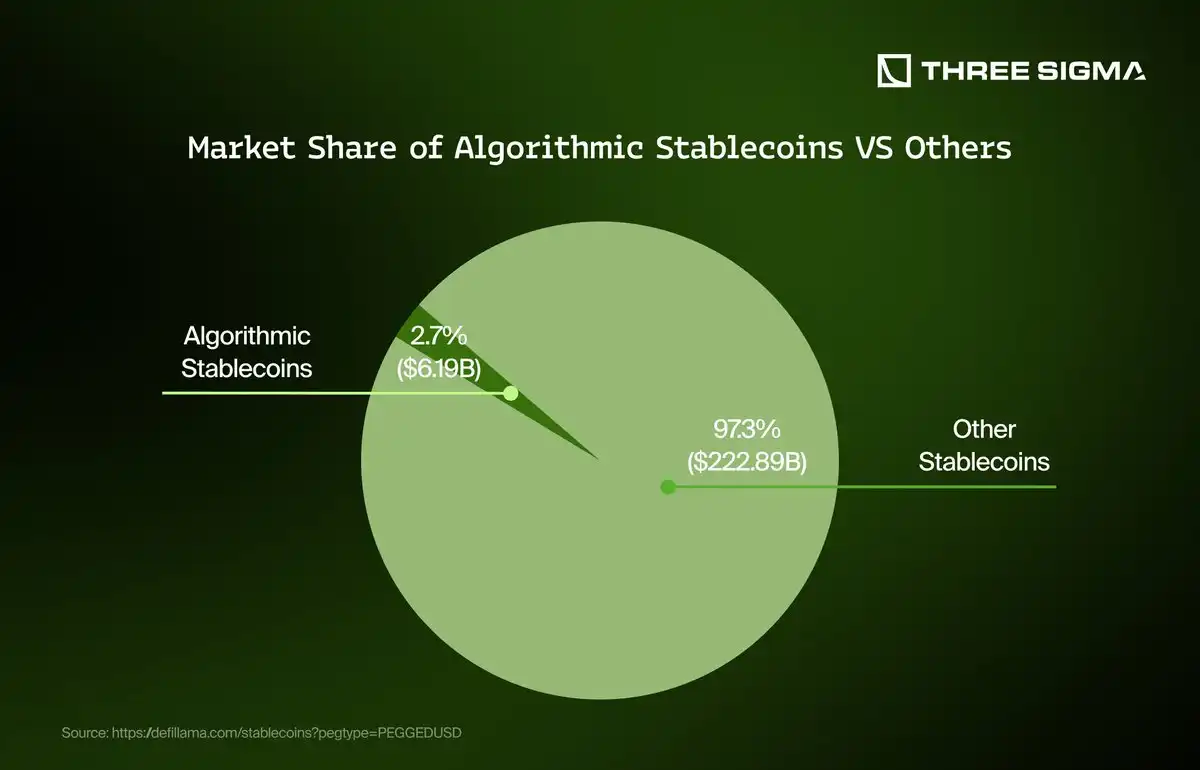

The adoption of stablecoins has risen dramatically over the years. In 2017, their total market capitalization was less than $3 billion, and by March 2025, it had grown to about $228 billion. Stablecoins now account for about 8.57% of the entire crypto market and are an important tool for risk aversion during transactions, cross-border payments and market turbulence.

This growth trend highlights the role of stablecoins as a key bridge connecting traditional financial markets and the crypto world. A chart from Coinglass clearly shows the steadily and dramatically growing market value of major stablecoins from the beginning of 2019 to the present.

What is a stablecoin?

A stablecoin is a cryptocurrency designed to keep its value stable by pegging its price to some external asset, such as fiat currency or commodity. For example, Tether (USDT) and USD Coin (USDC) are both stablecoins pegged to the US dollar 1:1. The goal of stablecoins is to provide the advantages of digital currencies (such as fast, borderless transactions on blockchains), but does not have the risk of violently volatile price in Bitcoin.

Stablecoins strive to maintain price stability by holding reserve assets or adopting other mechanisms, making them more suitable as a means of store of value in daily trading tools or crypto markets. In fact, most mainstream stablecoins achieve price stability through a mortgage mechanism, that is, every stablecoin issued requires equal value to support reserve assets.

To ensure the stability and credibility of stablecoins, clear regulation is required. At present, the United States has not yet issued comprehensive federal legislation, mainly relying on state-level rules and some proposals that are still under review; the EU has implemented strict reserve and audit requirements through the MiCA framework; Asia has shown a diversified regulatory strategy: Singapore and Hong Kong have implemented strict reserve requirements, Japan allows banks to issue stablecoins, while China has basically banned stablecoin-related activities. These differences reflect the trade-off between "innovation" and "stability" across the country.

Despite the lack of a unified global regulatory framework, the use and popularity of stablecoins are still growing steadily year by year.

Why are they released?

As mentioned earlier, the initial purpose of stablecoins is to provide users with a reliable digital asset for payment or as a store of value pegged to major global currencies, especially the US dollar. But their issuance is not for public welfare, but a highly profitable business opportunity, and Tether is the first company to discover and take advantage of this opportunity.

Tether launched USDT in 2014, becoming the first stablecoin and also created an extremely profitable business model, especially from the perspective of "per capita profit", which is one of the most successful projects in history. Its business logic is very simple: Tether issues 1 USDT for every USD it receives, and the user destroys the corresponding amount of USDT when redeems the USD. The US dollar received is invested in secure short-term financial instruments (such as U.S. Treasury bonds), and the resulting income belongs to Tether.

Understanding how stablecoins make money is the key to mastering the economic logic behind it.

Although the business model of stablecoins looks pretty simple, Tether has no control over its main source of income—the interest rates set by central banks, especially the Federal Reserve. Tether can make considerable profits when interest rates are high; but profitability drops significantly when interest rates are low.

Currently, the high interest rate environment is very favorable for Tether. But what happens if interest rates fall again in the future, even close to zero? Will algorithmic stablecoins also be affected by interest rate fluctuations? Which type of stablecoins may perform better in such an economic environment? This article will further explore these issues and analyze how the stablecoin business model adapts to the ever-changing macroeconomic environment.

2. Types of stablecoins

Before analyzing the performance of stablecoins under different economic conditions, it is crucial to understand the operating mechanisms of different types of stablecoins. While the common goal of all stablecoins is to maintain stable value pegged to real-world assets, each stablecoin responds to interest rate changes and overall market environment. Below we will introduce several major stablecoin types, their mechanisms, and their responses to different economic changes.

Fiat-backed Stablecoins

Fiat-backed stablecoins are the most well-known and widely used stablecoins at present. In essence, they are "tokenized" the US dollar in a centralized manner.

Their operating mechanism is very simple: whenever the user deposits USD 1, the issuer will mint a corresponding stablecoin; when the user redeems USD, the issuer destroys the corresponding tokens and returns the same amount of USD.

The profit model of fiat-backed stablecoins is mainly hidden behind the scenes. Issuers invest users’ deposits in various short-term and secure financial instruments, such as Treasury bonds, secured loans, cash equivalents, and sometimes allocate higher volatility assets, such as cryptocurrencies (such as Bitcoin) or precious metals. The income generated by these investments constitutes the issuer's main source of income.

However, high returns are also accompanied by considerable risks. One of the main persistent challenges is compliance issues. Governments in many countries have rigorous scrutiny of fiat-backed stablecoins, citing that they are essentially equivalent to issuing "digital currencies" and therefore must comply with strict financial regulatory regulations.

Although most stablecoin issuers have successfully dealt with regulatory pressures and have not encountered serious business disruptions, major challenges still occur from time to time. A notable example is the European MiCA (Crypto Asset Market) Regulation, which recently prohibits USDT (Tether) from circulation in certain markets because it does not meet its strict regulatory requirements.

Another major risk is "depeg risk". Stablecoin issuers usually invest a large amount of reserve assets into various investment tools. If a large number of users apply for redemption of tokens at the same time, the issuer may have to sell these assets quickly, which may cause huge losses. This situation may trigger a chain reaction similar to a "bank run", making it difficult for issuers to maintain the token pegging relationship with the US dollar, and may even lead to bankruptcy.

The most prominent case occurred in March 2023, involving USDC (issued by Circle). At that time, Silicon Valley Bank (SVB) went bankrupt, and rumors quickly spread that Circle had a large amount of reserves stored in SVB, which caused market concerns about whether Circle's liquidity and USDC could maintain its linkage. These panics caused USDC to temporarily deank. This incident highlights the risks when stablecoin reserves are deposited in centralized banks. Fortunately, Circle solved the problem within a few days, restored market confidence and re-stabilized USDC's hook.

Currently, the two most important fiat-backed stablecoins on the market are USDT (Tether) and USDC (Circle).

Commodity-backed stablecoins are an innovative category in the stablecoin ecosystem that issue corresponding digital tokens by collateralizing tangible physical assets (usually precious metals such as gold and silver, or commodities such as oil and real estate).

The operating mechanism of this type of stablecoins is similar to that of fiat currency-supported stablecoins: for each unit of physical goods deposited, it is convenient to mint an equal value token. Users can usually redeem these tokens as physical goods themselves, or equivalent cash, at which time the corresponding tokens will be destroyed.

The issuer's revenue source mainly comes from the token's minting (creation) and redemption (destruction) handling fees. For example, Pax Gold (PAXG) charges a small fee when handling the creation and destruction of tokens, although Paxos does not currently charge storage fees for gold it holds. In addition, issuers may also make profits by providing services for transactions and exchanges between tokens and US dollars or physical goods.

Similarly, Tether Gold (XAUT) revenue also comes from fees related to redemption and delivery. If the user redeems the XAUT token as a physical gold bar, or exchanges the gold for cash through Tether, the relevant fee will be charged. For example, during the redemption process, a 25 basis point (0.25%) fee will be charged at the gold price, and if physical delivery is selected, a freight will also be charged. If the user chooses to sell the redeemed gold bars in the Swiss market, an additional 25 basis points will be charged.

However, such stablecoins are also at risk, especially the volatility of the commodity prices themselves, which may affect the stable peg of the token. In addition, compliance issues are also a major challenge. Commodity-supported stablecoins are often subject to strict regulatory requirements and must have transparent and secure custody arrangements.

The most successful commodity-backed stablecoins on the market currently include Paxos' Pax Gold (PAXG) and Tether's Tether Gold (XAUT), both supported by gold reserves, providing investors with convenient digital commodity exposure.

In summary, commodity-supported stablecoins connect traditional commodity investment and digital finance, provide investors with stability and physical asset exposure, and also emphasize regulatory compliance and transparency.

Crypto-backed stablecoins are an important category in the stablecoin system, which maintains a stable value pegged to fiat currency (usually the US dollar) through cryptocurrencies as collateral. Unlike fiat or commodity-supported stablecoins, these tokens rely on smart contract technology to build a transparent and automated system.

The basic mechanism is that users lock crypto assets (usually over-collateralized) into smart contracts, thereby minting stablecoins. The over-collateralized design can buffer the price fluctuations of crypto assets and ensure that the stablecoins can maintain their set anchor value. When users redeem stablecoins, they return stablecoins of equivalent value. After the system destroys the tokens, they release the crypto assets that were originally collateralized.

The profit model of crypto-supported stablecoins mainly includes:

Charge interest from users who lend stablecoins;

Liquidation fees are charged for users whose mortgage assets are below the liquidation line;

The governance mechanism rewards set in the agreement are used to incentivize coin holders and liquidity providers.

Represented by DAI (now known as USDs), it is issued by MakerDAO (now renamed SKY). It is mainly collateralized by crypto assets in the Ethereum ecosystem. MakerDAO's revenue sources include charging stability fees (interest) to users who lend USDs, and fines when liquidation is triggered. These costs jointly support the stable operation and sustainable development of the agreement.

Another example is the HONEY stablecoin issued by Berachain, which is currently mainly collateralized assets with USDC and pYUSD. HONEY's revenue sources include redemption fees: Berachain charges a 0.05% handling fee when a user redeems HONEY and retrieves his mortgaged assets (USDC or pYUSD).

Although these stablecoins are classified as "crypto-backed", most of them are actually like wrapped stablecoins that support stablecoins, such as USDC. Although the initial goal was to rely entirely on native crypto assets as collateral to maintain stability, in practice, it is still very difficult to achieve true stability without relying on fiat stablecoins.

Of course, such assets also have inherent risks. For example, price fluctuations in underlying crypto assets can pose major challenges - such as triggering large-scale liquidation during sharp declines, which may break the anchoring mechanism of stablecoins. In addition, smart contract vulnerabilities or protocols are attacked, which can seriously threaten the stability of the entire system.

In summary, crypto-backed stablecoins like USDs and HONEY play an important role in providing decentralized, transparent and innovative financial solutions. However, although nominally crypto collateral, they often rely heavily on fiat currency stablecoins in reality, which requires a more complete risk management mechanism to maintain their resilience and credibility.

Treasury-backed stablecoins are a type of stablecoins supported by government bonds (especially U.S. Treasury bonds). These stablecoins are usually pegged to the US dollar. While providing stable value, they can also provide passive income to holders through the interest income of the underlying treasury bonds. Therefore, they are more like a profit-based investment token, combining the stability and financial nature of traditional stablecoins.

For example, Ondo's USDY (USD earnings token) is known as a tokenized note backed by short-term U.S. Treasury bonds and bank demand deposits. Its goal is to provide stablecoins-like convenience for non-U.S. individual and institutional investors, while providing high-quality returns denominated in US dollars. After an investor purchases USDY, the funds are used to purchase US Treasury bonds and partially deposited into the bank, and the interest generated is distributed proportionally to the token holders. USDY is a "bearing asset", which means that it will passively increase as the interest on the underlying asset is generated, and the value of the token increases over time.

Another example is Hashnote's USYC (USD Earnings Coin), which is the on-chain statement of Hashnote's short-term income fund (SDYF), investing in short-term US Treasury bonds and participating in the repurchase and reverse repurchase markets. USYC's return level is linked to the short-term "risk-free interest rate", while combining the speed, transparency and compositional advantages of blockchain, while minimizing risks in agreement, custody, supervision and credit. Users can exchange USYC for USDC or PYUSD on the same day (T+0) or the next day (T+1), and cast directly on the chain, the process is atomized and instant. Like USDY, USYC is also a "earnings asset", which passively accumulates returns through the interest generated by underlying assets.

Although these stable coins have the dual advantages of stability and profitability, they also have some risks:

· Regulatory Risk: Since such assets are usually targeted at non-US users to avoid regulatory requirements in the United States, future policy changes may bring uncertainty;

·Customer risk: It is necessary to rely on the issuer to properly manage and hold underlying assets;

·Liquidity risk: When market fluctuations are severe, users' redemption requests may be limited;

·Counterparty risk: Especially in repurchase agreements, if the counterparty defaults, it may lead to losses;

·Macroeconomic risks: If interest rates change, it may affect the overall return level.

This type of token is often classified into a new category that is rapidly developing - "Treasury-backed crypto".

Algorithmic stablecoins are stablecoins that rely on economic mechanisms and market incentives, rather than maintaining stable value entirely with traditional assets such as fiat currency or treasury bonds. Such models usually maintain anchor exchange rates (such as pegged to the US dollar) through supply and demand adjustment mechanisms, but often face challenges in extreme market environments. The fundamental problem is the high reliance on sustained market confidence and effective incentive structures, which are prone to failure during severe stress.

USDe, issued by Ethena, is a new "algorithm-like" stablecoin that uses a hybrid model. It maintains stability through the "Delta neutral hedging mechanism", that is, holding crypto assets such as BTC and ETH as collateral, while establishing equal amounts of short positions in the derivatives market to hedge the price fluctuations of underlying assets, thereby maintaining a stable anchorage with the US dollar. USDe achieves a 1:1 full mortgage, which is more capital-efficient than an over-collateralized model. In addition, Ethena also incorporates liquid stablecoins such as USDC and USDT into its reserves to enhance the efficiency of liquidity and hedging strategies.

Despite multiple innovations, algorithmic stablecoins face significant risks: market instability, extreme volatility or liquidity crises can all interfere with their mechanisms to maintain anchoring. Moreover, the dependence on derivatives brings opponent risks and execution risks, making the system vulnerable to external shocks.

While new models like USDe try to mitigate these problems through structured hedging and diversified reserves, their long-term stability still depends on the overall liquidity situation and the ability to maintain effective operations in adverse market environments.

3. Current mainstream stablecoins

When it comes to stablecoins, USDT and USDC are undoubtedly the dominant forces in the market, both of which are centralized liquidity pillars and occupy a centralized position in the crypto market. They have a similar structure: they are all issued by centralized entities, are completely supported by fiat currency reserves, and are widely integrated in major exchanges and financial platforms.

USDT is issued by Tether and has the largest market share and is known for its deep liquidity and wide adoption, especially in high-frequency trading environments. USDC, issued by Circle, is positioned as a more compliant and transparent option, and is more favored by institutions and businesses seeking a regulatory-friendly environment. Although the two differ slightly in details, their core functions are consistent: providing a stable, trusted digital dollar that supports the operation of the entire crypto ecosystem.

In contrast, there are USDS, DAI and USDe, which represent the decentralized forces corresponding to the stablecoins supported by fiat currencies, although their degree of decentralization varies. DAI and USDS are essentially derived from the same system - MakerDAO (now renamed Sky). Among them, USDS is an evolutionary version of DAI and a key link in Sky's long-term planning.

DAI is historically more decentralized, relying on excess crypto assets to maintain its anchor exchange rate; while USDS reflects Maker's trend of transformation towards a more structured and strategic direction, focusing on efficiency first rather than blindly pursuing pure decentralization.

At the same time, USDe is also an important decentralized stablecoin competitor, but takes a completely different path. Unlike the excess collateral and governance mechanism of the Maker model, USDe introduces a revenue generation structure, using its collateral assets to bring additional benefits to coin holders.

USDT

When discussing stablecoins, USDT naturally became the dominant force, playing an important role as a centralized liquidity pillar in the crypto market. USDT issued by Tether has the largest market share and is known for its deep liquidity and wide adoption, especially in high-frequency trading environments. It provides a stable and trustworthy digital dollar that supports the operation of the crypto ecosystem and becomes the main medium for trading pairs, arbitrage opportunities and cross-exchange liquidity. Its wide acceptance cements its role in the fields of centralized and decentralized finance.

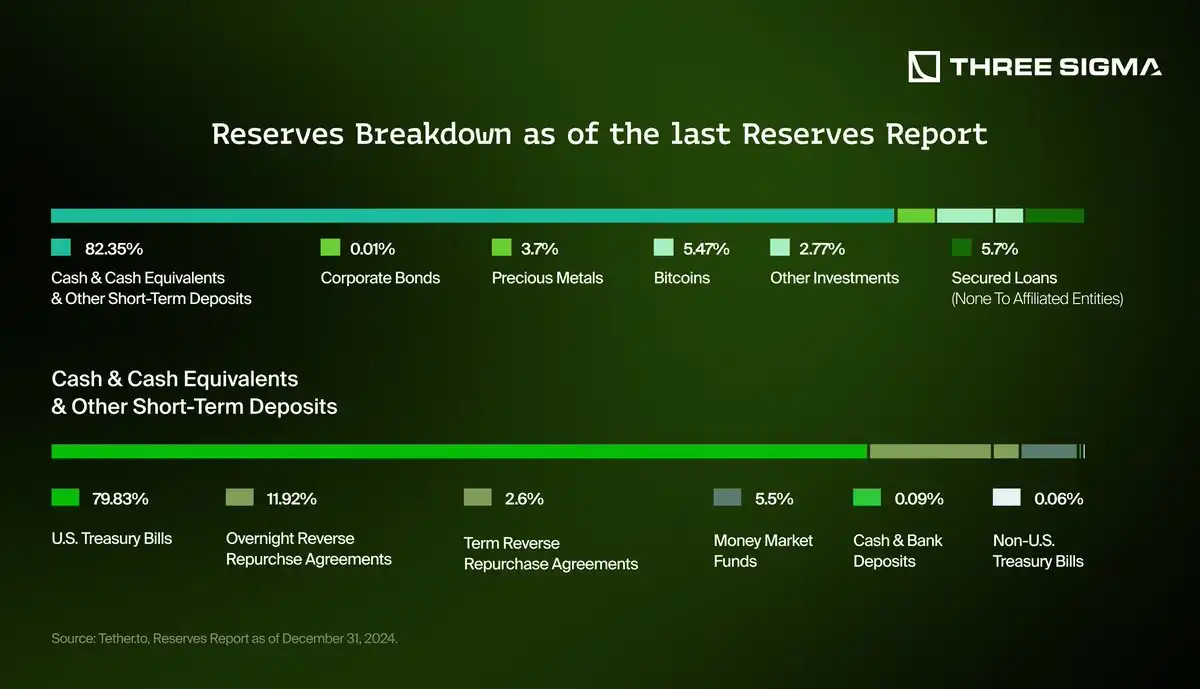

Tether's revenue comes primarily from its massive reserve assets management, which guarantees every USDT token issued. These reserve assets mainly include cash equivalents such as U.S. Treasury bonds, commercial paper, short-term deposits, money market instruments, and corporate bonds. By strategically allocating these reserves, Tether is able to accumulate interest and investment income, making a significant contribution to its revenue.

In addition, Tether occasionally participates in transactions in short-term lending and other financial instruments, further diversifying and enhancing its revenue stream. Tether also earns additional revenue through token issuance, redemption processes and transaction fees on various blockchain platforms.

Below is its latest reserve report, clearly showing that over 80% of its reserves consist of cash, cash equivalents and other short-term deposits, of which about 80% are dedicated to Treasury bonds.

Essentially, Tether's revenue depends primarily on interest rates set by central banks, especially those of the U.S. Federal Reserve system, because the appreciation of most of its reserve assets is directly related to these rates. Higher interest rates can significantly increase Tether's returns from its reserves, while lower interest rates can significantly reduce its revenue potential.

Importantly, unlike some other stablecoins, all revenue generated by Tether is retained by the issuer itself and is not allocated to USDT token holders. This is different from earning stablecoins, which distribute returns directly to holders, highlighting a key difference in the stablecoin business model.

Historical income trends

Historically, Tether’s revenue trajectory has been closely linked to global interest rate trends. During the period of low interest rates between 2019 and early 2022, Tether's revenue growth was relatively moderate, mainly due to its reliance on conservative investment strategies and limited returns.

However, starting from mid-2022, Tether's revenue has grown significantly as major central banks actively raise interest rates in response to inflation. Monthly income increased nearly tenfold from June 2022 to early 2025, underlining the high sensitivity of Tether's revenue sources to macroeconomic changes and monetary policy decisions. This trend demonstrates the effectiveness of Tether's revenue model in a rate hike environment.

Still, income is not entirely dependent on interest rates. Even with interest rates falling, Tether is likely to achieve revenue growth as long as USDT supply increases significantly. Larger supply means more managed assets, which can compensate for lower yields, thereby maintaining or even increasing overall revenue.

USDC

USDC, issued by Circle, is one of the most trusted centralized stablecoins on the market. Known for its compliance and transparency, it is widely used in decentralized finance, institutional payments and cross-chain applications. Its presence on multiple blockchains enhances its composability and ecosystem coverage.

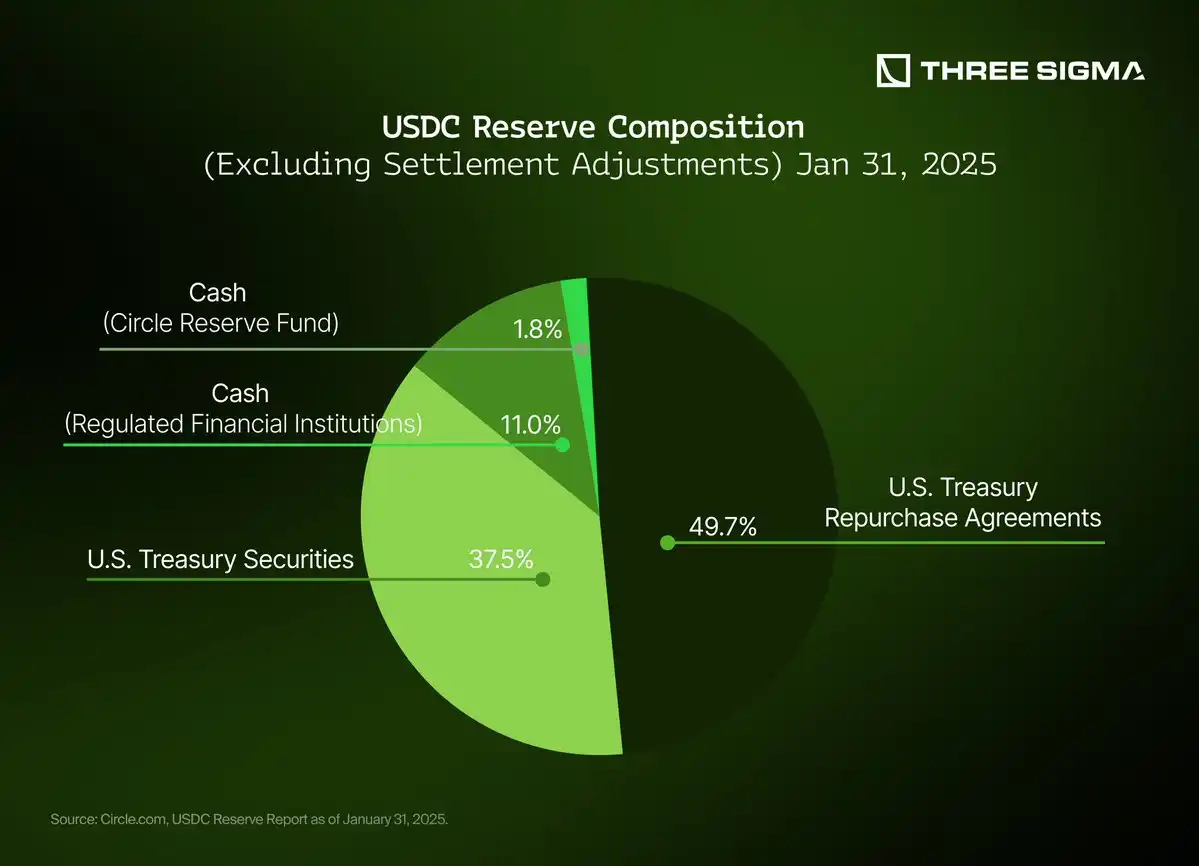

A key feature of USDC is Circle's strict reserve structure and public disclosure. As of January 31, 2025, USDC had over US$53.2 billion in circulation and was fully supported by a reserve of US$53.28 billion certified by an independent accounting firm. These reserve funds are divided into the following parts:

Circle Reserve Fund: A government money market fund holding $47.26 billion in U.S. Treasury bonds and buyback agreements.

Separate bank accounts: Hold an additional $6.02 billion in regulated financial institutions.

Circle earns income by managing these reserve assets, relying primarily on interest income from U.S. Treasury and overnight loan arrangements. Despite structural similarity to Tether's model, Circle is unique through its funding structure, representing USDC holders with 100% interest in reserve fund. This not only provides a clearer regulatory separation, but also may make future product integration more flexible.

Unlike decentralized alternatives, USDC does not directly distribute the benefits to users. Instead, revenue belongs to the issuer, with priority given to simplicity, compliance and capital preservation.

Historical income trends

Circle's revenue trajectory is closely linked to the overall interest rate environment, as its conservative investment strategy focuses primarily on short-term government debt.

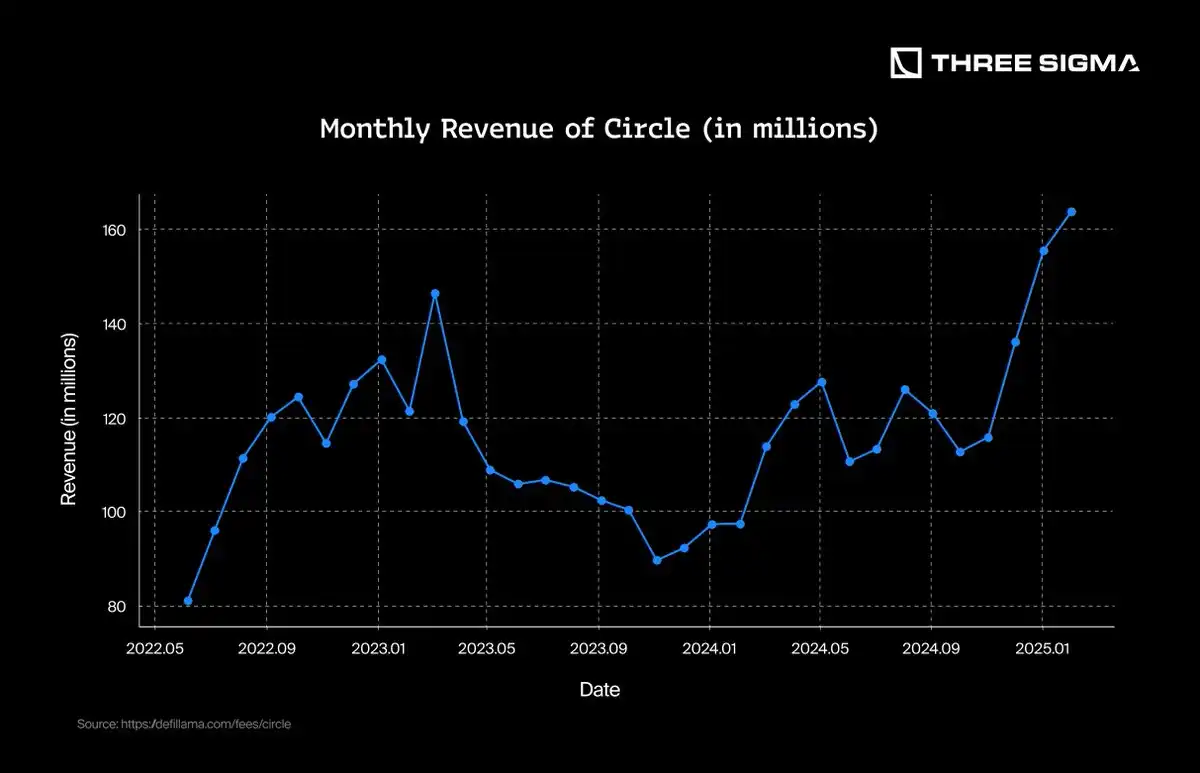

In 2022, Circle's revenue grew steadily as the U.S. Federal Reserve raised interest rates and peaked at $146.5 million in March 2023. However, later that year, pressure from competitive stablecoins, blockchain reliability issues (especially on Solana), and reputation volatility associated with banking partners led to a gradual decline in revenue. By the end of 2023, monthly revenue had dropped to less than $90 million.

In 2024, with reduced redemption volumes, rebounding cryptocurrency activity and a continued high interest rate environment, Circle’s revenue began to recover, with revenue rebounding to $126 million in August and ending the full year with strong momentum. In February 2025, Circle set its highest monthly revenue record, reaching $163.7 million.

This trend highlights the resilience of USDC and the close relationship between stablecoin income model and monetary policy. Circle's continued recovery emphasizes its ability to maintain user trust and liquidity dominance in the market cycle.

USDS/DAI (SKY)

USDS is the current evolution of DAI, the first major decentralized stablecoin issued by MakerDAO, aiming to provide censorship-resistant alternatives to assets endorsed by traditional fiat currencies. Although they both belong to the Maker ecosystem, there are structural differences in collateral models and target use cases.

DAI is an overly collateralized stablecoin backed by a mixed collateral of cryptocurrencies, RWAs and stablecoins. Users deposit DAI through Maker Vaults such as ETH, stETH or USDC to mint DAI to ensure that they are always fully collateralized. This design makes DAI highly risk-resistant, but also limits its scalability.

USDS, on the other hand, represents the evolution of MakerDAO to a more traditional financially compatible stablecoin. While USDS is still over-collateralized, it adopts a structured reserve approach, including tokenized short-term U.S. Treasury bonds. This aligns it with institutional needs, becoming a competitor for stablecoins such as USDT and USDC, while maintaining MakerDAO's decentralized governance model.

The transition from DAI to USDS reflects the shift to wider institutional adoption. While DAI was initially a crypto-native stablecoin, mainly backed by decentralized assets, USDS optimized its collateral structure by introducing more RWA, especially U.S. Treasury bonds.

In addition, USDS enhances stability through a direct convertible mechanism, making it easier to maintain anchoring to the US dollar. Unlike DAI's early reliance on external DeFi incentives, USDS was designed from the outset to provide built-in benefits through DSR, making it more attractive in both DeFi and TradFi environments. This structure is in line with the increasingly popular RWA earnings DeFi strategy in 2025.

Transparency is the basis of Sky ecosystem design. It is not only a tool to maintain an anchoring mechanism, but also a prerequisite for building trust, attracting institutional participation and responsible capital allocation. In an environment where billions of dollars of assets are managed, users and institutions require a clear view of where these funds are stored, how they are used, and the endorsement of the system.

Therefore, Sky provides a publicly available real-time dashboard that clearly demonstrates the endorsement, diversification and benefits of USDS. But transparency alone cannot stabilize the currency, and anchoring is maintained through over-collateralization, risk management asset allocation and protocol-level mechanisms.

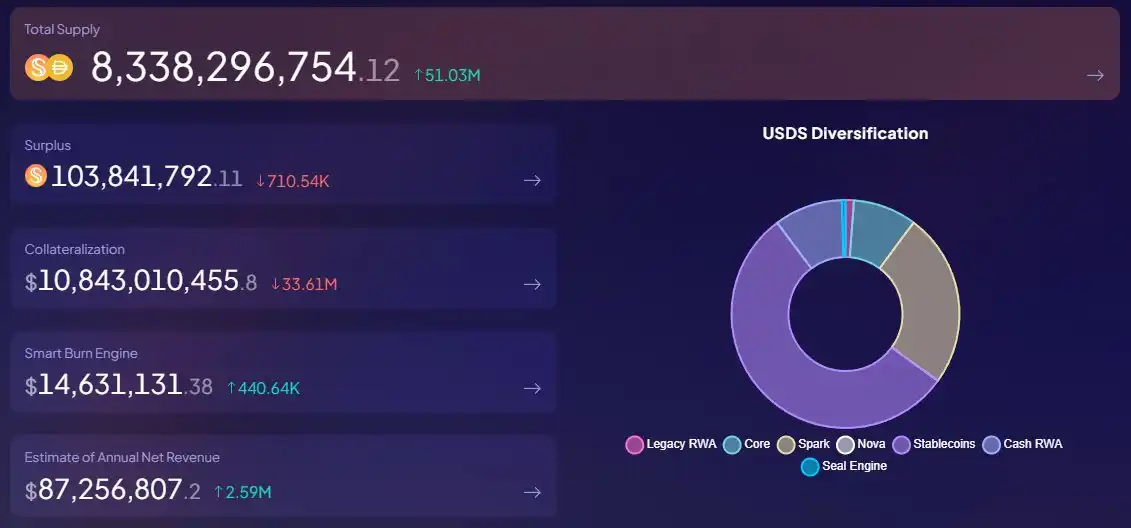

USDS always maintains more collateral than issuance. As of now, USDS has a total mortgage base of more than $10.8 billion and supply is approximately $8.3 billion, ensuring that there is sufficient buffer to deal with market volatility or redemption. Its collateral is distributed in several key sources:

Stablecoin (54.8%): Mainly supported by the LitePSM module, it is an anchor stability module that allows 1:1 redemption between DAI and USDC to support USDS anchoring.

·Spark (24.7%): Sky’s lending and liquidity agreement, minting USDS with high-quality, earnings-generating collateral.

·Cash RWA (9.7%): Fully held on BlockTower Andromeda, a strategy for investing in short-term U.S. Treasury bonds, providing low-risk real-world returns.

·Core (9%): Sky's over-staking Vault system, where users use assets such as ETH and stETH to mint USDS under strict mortgage thresholds.

Together, these mechanisms ensure that USDS remains stable, over-collateralized, and are supported by a range of liquid assets that generate returns, while transparency ensures that anyone can verify this at any time.

Historical income trends

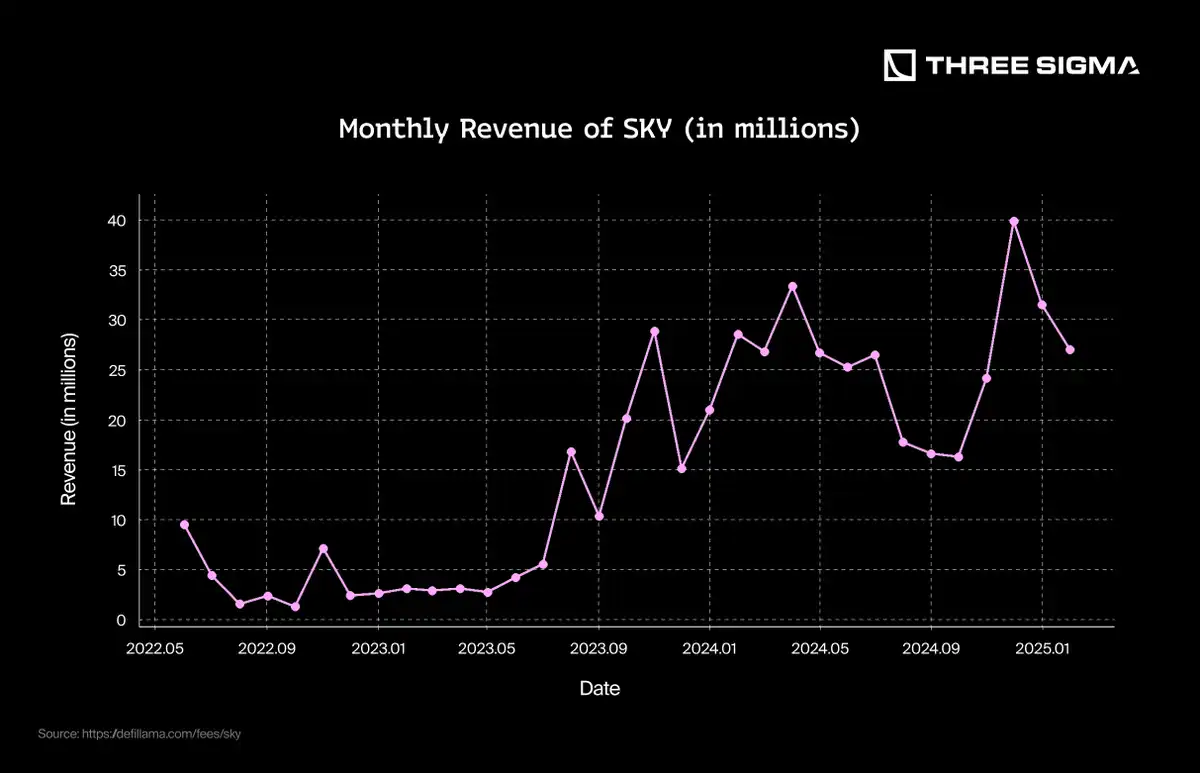

The chart above shows the accumulated revenues of the Sky agreement from mid-2022 to early 2025. Despite steady growth in revenues over the early months, revenue growth has accelerated significantly by the end of 2023 with the expansion of DeFi integration, increased adoption of USDS, and deeper engagement with real-world assets such as short-term U.S. Treasuries, coincided with the beginning of rising interest rates. By the beginning of 2025, cumulative revenues had exceeded $500 million, reflecting Sky's ability to capture benefits in crypto-native and institutional strategies while scaling sustainably.

USDe

USDe is a delta-neutral synthetic dollar stablecoin that uses a synthetic dollar structure maintained by perpetual futures, developed by Ethena Labs. Unlike traditional stablecoins backed by fiat currencies or over-staked crypto assets, USDe maintains its peg to the US dollar through an automated hedging strategy. This makes it fully supported, scalable and censor-resistant. Ethena also offers sUSDe, a USDe version with income, that earns rewards through liquid pledged assets and capital rate arbitrage in futures markets.

Since its public release in early 2024, Ethena has expanded rapidly, reaching $6 billion in supply in ten months, making USDe the third largest dollar-denominated asset in the crypto space. It has also become a fundamental component of DeFi, integrated in major protocols such as Pendle, Morpho and Aave, and its adoption has driven significant growth. In addition to DeFi, USDe has also penetrated CeFi and is currently integrated as margin collateral on about 60% of centralized exchanges, surpassing the USDC balance on Bybit in less than a month.

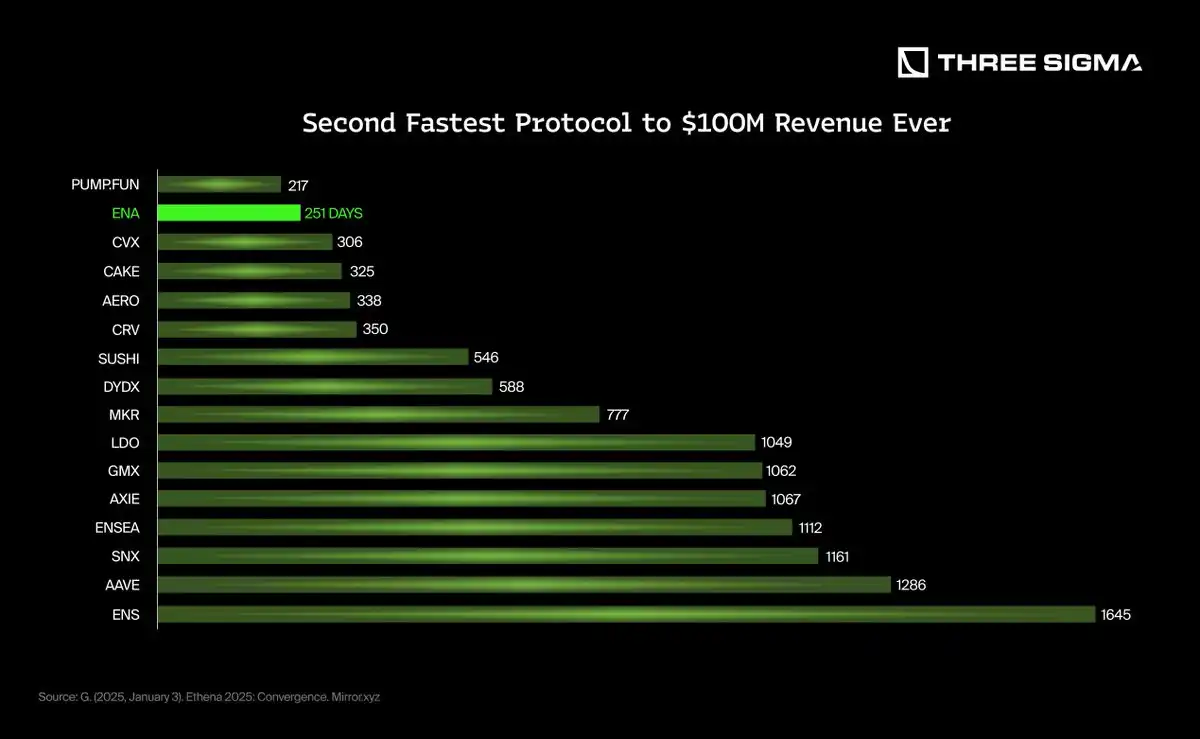

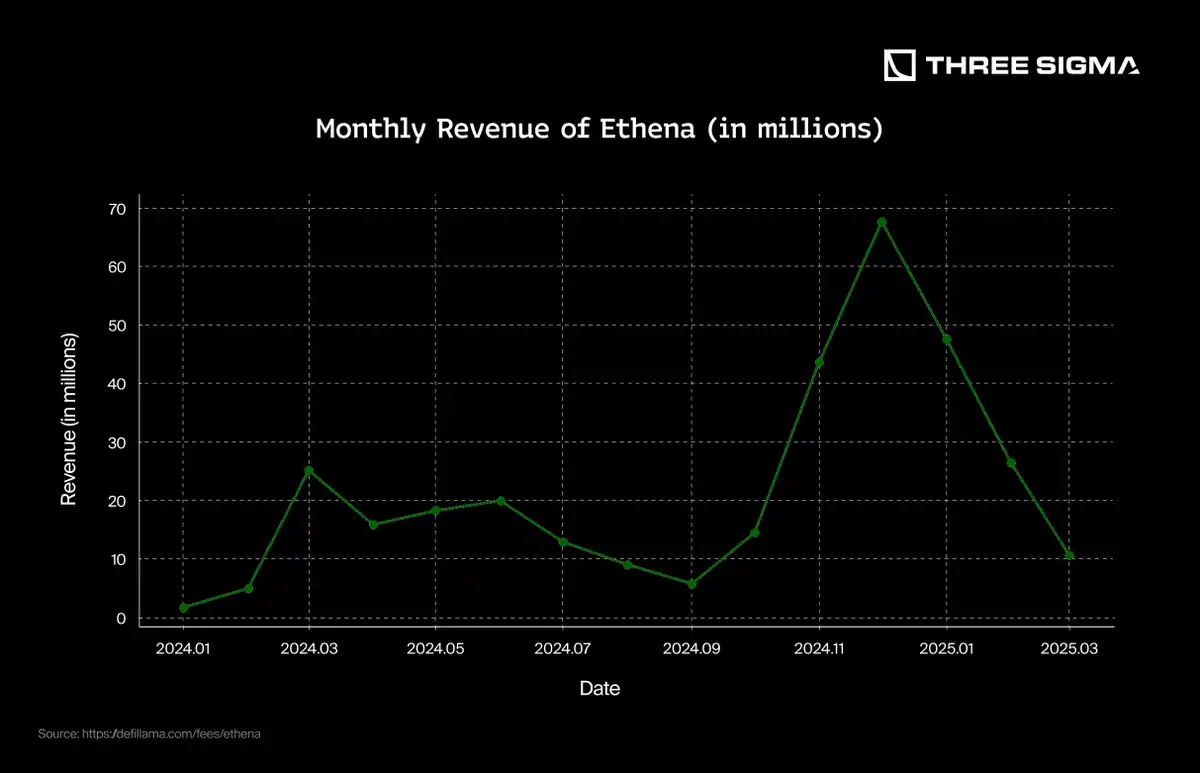

If we have a deeper understanding of revenue, Ethena is no less than that, becoming the second dApp in history to reach $100 million in revenue (after Pump.fun), a milestone achieved in 251 days. In 2024, Ethena became the dominant force in DeFi, with assets accounting for more than 50% of Pendle TVL, about 30% of Morpho TVL is tied to Ethena-related assets and becoming the fastest growing new asset on Aave, reaching $1.2 billion in deposits in just three weeks.

The next phase of Ethena is defined by Convergence and aims to achieve the convergence of DeFi, CeFi and TradFi through USDe. By introducing iUSDe, a packaged version of sUSDe, designed for institutional adoption, Ethena plans to offer a high-yield, crypto-native dollar product tailored for asset managers, private credit funds and exchange-traded products. By connecting capital flows and interest rates between various financial systems, Ethena positioned USDe as the cornerstone of the developing digital dollar field.

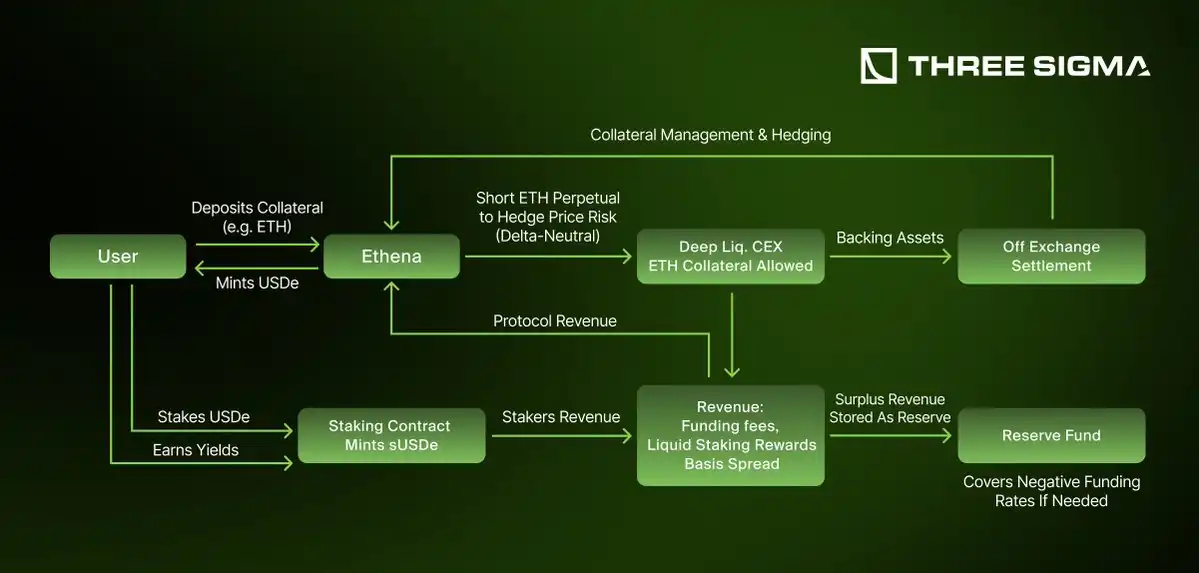

How does USDe work?

USDe maintains its stability through the delta-neutral hedging strategy to ensure its value is not affected by market volatility. When a user casts USDe, the collateral received by Ethena can include ETH, BTC, LSTs, USDT, USDC, SOL, etc. To neutralize price risk, Ethena opens a short position in perpetual futures for each collateral received. For example: If the collateral is ETH, Ethena will short ETH perpetual futures.

This mechanism ensures that any price fluctuations in collateral will be hedged by the corresponding futures positions. If the collateral increases, short positions will lose money, but will be compensated by the collateral appreciation. On the contrary, if the collateral price falls, short positions will make a profit, offsetting the depreciation of the collateral. This mechanism ensures that USDe remains stable and is not affected by market volatility.

Unlike other synthetic stablecoins, Ethena does not use additional leverage, only uses leverage naturally applied by derivative exchanges to evaluate collateral. This minimizes liquidation risks and ensures that every short position is backed 1:1 by assets.

To enhance security, Ethena's supported assets remain on-chain and are hosted through an off-site settlement system to reduce counterparty risk. Ethena never transfers control of assets to derivatives platforms completely, but is used only to provide margin for its short hedging positions, ensuring decentralized and transparent asset management.

Ethena generates revenue by capturing a portion of the benefits generated by its delta-neutral strategy, including:

Fund rate arbitrage: Ethena makes a profit when the fund rate of perpetual futures is positive.

Liquid pledge reward: pledge proceeds generated by pledged LSTs, part of which is retained by Ethena.

Base profit: Ethena benefits from the efficiency differences between spot and futures markets.

Agreement Fees: A portion of the total return is used to reserve funds and agreement vaults to ensure long-term sustainability.

While USDe's delta-neutral strategy minimizes exposure to price volatility, it remains vulnerable to capital interest rate fluctuations, market imbalances and counterparty risks. If the interest rate of funds is negative for a long time, Ethena's reserve fund will absorb losses, but long-term negative interest rates may put pressure on the system.

Liquidity crises or extreme fluctuations may cause temporary disconnection if the spot and futures markets deviate.此外,依赖中心化交易所进行对冲会引入对手方风险,但Ethena 通过将资产保持在链上并进行场外结算来减轻这一风险。

历史收入趋势

Ethena 于2024 年2 月19 日向公众开放,允许用户通过存入稳定币铸造USDe,并将其质押为sUSDe 以赚取收益。在不到一年的时间里,协议累计收入超过3.2 亿美元,成为DeFi 历史上最迅速的盈利曲线之一。

2024 年上半年收入的稳步增长反映了USDe 供应量的持续增加以及在DeFi 和CeFi 平台上的广泛采用。然而,收入的急剧加速始于2024 年10 月,这与以下因素的发生相吻合:

USDe 和sUSDe 集成进入主要的借贷市场,如Aave 和Morpho。

市场波动性增加带来了资金利率套利机会的激增。

新的机构产品如iUSDe 的推出,将Ethena 的影响力扩展到TradFi 领域。

到2025 年第一季度,协议的累计收入突破3 亿美元,尽管仅上线不到15 个月,Ethena 已经跻身加密领域收入生成前列。这一快速增长表明市场需求强劲,并验证了USDe 的delta-neutral 模型的可持续性。

然而,在2024 年末达到峰值后,2025 年第一季度的月度收入出现了急剧下降。这一下降与资金利率套利机会的减少相关,主要交易所的永续期货资金利率趋于正常化。随着波动性的降低和更中性化的资金环境,Ethena 的主要收入来源之一暂时减弱,突显出该模型对市场条件的敏感性。

4. 利率与收入的相关性

利率对稳定币的影响是其收入表现中最具决定性的因素之一。如前所述,稳定币通过各种机制产生收入,包括带息储备、市场套利和其他收益生成策略。由于许多稳定币持有的资产会受到利率变化的影响,因此它们的收入潜力通常会受到宏观经济条件的影响。

为了更好地理解这种关系,我们通过将收入除以供应量来调整收入。这种归一化处理使得比较更为准确,因为稳定币供应量的增加自然会导致更大的潜在收入生成。通过关注每单位供应的收入,我们可以隔离利率波动对稳定币盈利能力的直接影响。

USDT

深入的图表分析生动地展示了Tether 收入与利率波动之间的正相关关系。历史图表将Tether 的季度收入与利率变化进行对比,显示出明确的同步性,突显了收入对利率调整的近乎即时反应。

这些可视化表现有效地强调了Tether 收入对利率环境的敏感性,为未来潜在表现场景提供了预测性洞察。它们突出了主动财务和储备管理策略的重要性,以减轻与利率波动或下降周期相关的收入风险。

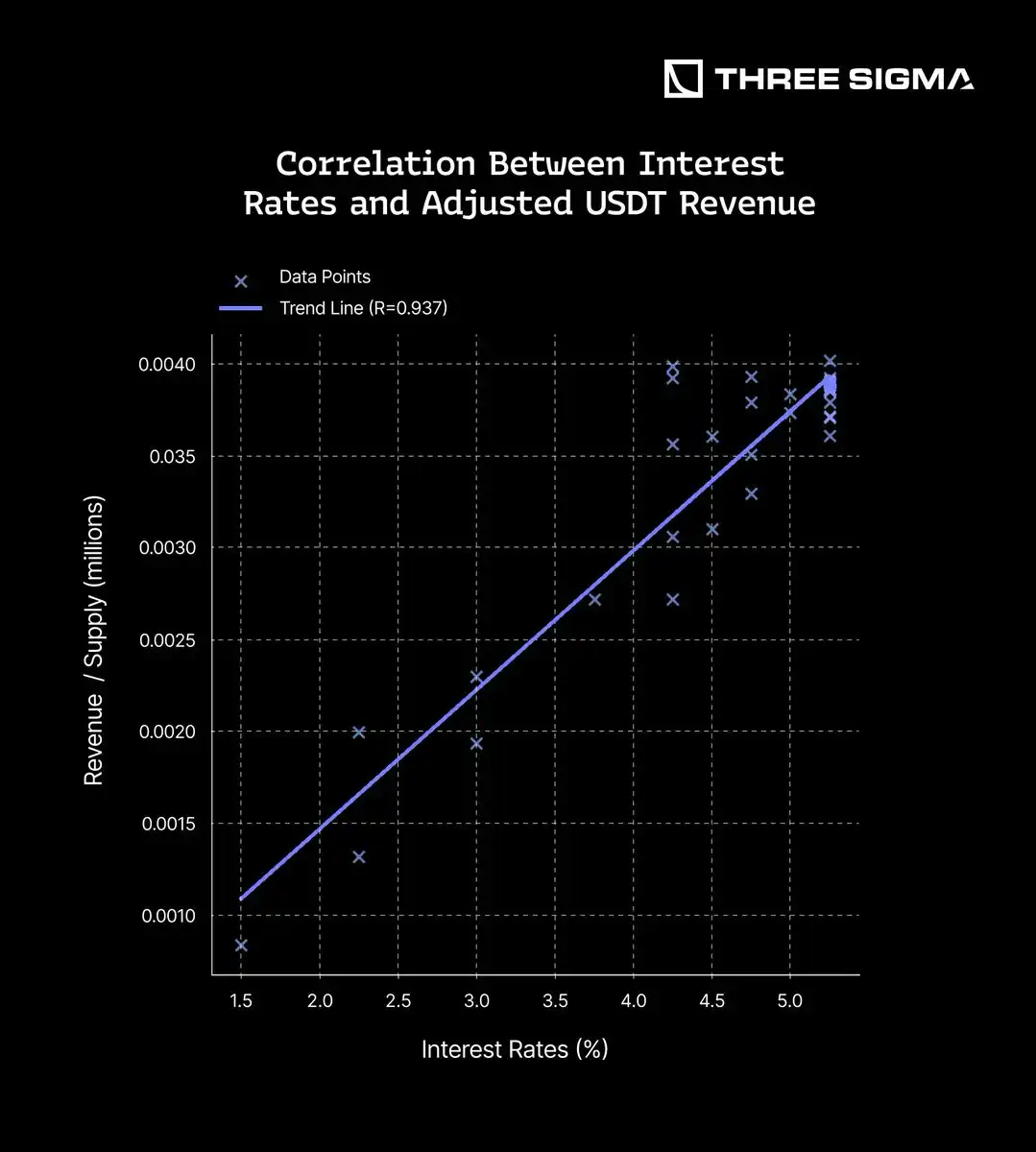

下图展示了利率与调整后的稳定币收入之间的相关性。每个图表都展示了每单位稳定币供应(纵轴)与利率(横轴)之间的关系变化。

图表进一步突显了利率与USDT 调整后每单位供应收入之间的强正相关关系(R = 0.937)。这表明,随着利率的上升,USDT 的每单位供应收入也随之增加,反映出USDT 在美国国债投资中的收益增长。随着利率上升,这些国债的收益率提高,直接影响USDT 的整体收入。

这一相关性突显了USDT 如何有效地管理其储备资产,从而在不断变化的经济条件下获益,特别是在高收益环境中。它反映了USDT 灵活的金融策略及其在利率上升时表现出色的定位,增强了其经济稳定性和作为可靠数字资产的角色。如前所述,100% 的相关性是不可能的,因为80% 的储备以现金和国债形式持有,其中80% 专门配置在国库券中。

USDC

USDC 的经济实力体现在战略储备管理上。随着利率上升,USDC 从其在美国国债中的大量持有中获益,这些国债提供更高的回报。USDC 将75%-80% 的储备投资于国债,不仅维持了稳定性,还随着债券收益率的提高生成额外的收入。与利率波动的直接关联使USDC 能够在利率上升的环境中获益,进一步巩固其作为收益生成稳定币的地位。

趋势线显示了强正相关关系(R = 0.889),表明随着利率的上升,USDC 每单位供应的收入相应增加。这与预期一致,因为像其他储备支持的稳定币一样,USDC 从高收益资产(如美国国债)中获得收益。

这一相关性突显了USDC 优化储备和适应经济变化的能力。它还强调了储备支持的稳定币如何利用利率上升来增强收益生成,进一步巩固了它们在数字资产生态系统中的角色。

虽然这一相关性较强(R = 0.889),但低于USDT 的相关性,原因在于储备组成的差异。USDT 将更大部分的储备(大约80%)维持在短期美国国库券中,这些国库券对利率变化高度敏感。相比之下,USDC 的储备更加多元化,只有37.5% 的储备在国债中,近50% 的储备用于回购协议,而这些回购协议对利率波动的反应较为间接。这种多元化的方式增强了流动性和稳定性,但也稍微削弱了利率上调对收益的直接影响,从而导致相关性较弱。总结来说,USDT 与USDC 收入的直接对比突显了储备组成和收益策略的影响。

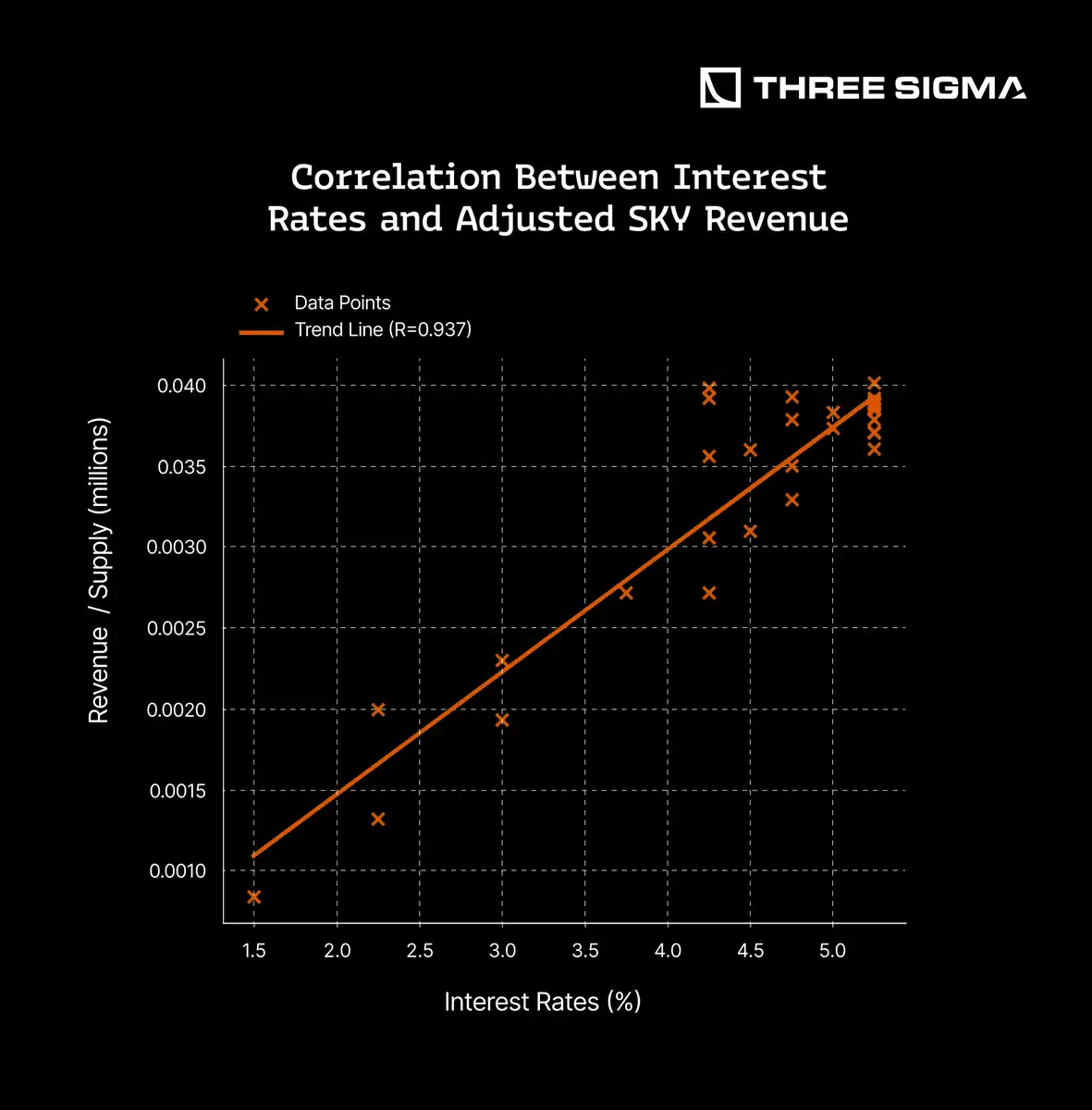

SKY(DAI/USDs)

SKY 的经济实力体现在战略储备管理上。随着利率上升,SKY 稳定币(USDS 和DAI)从其对收益资产的暴露中获益。

与USDC 和USDT 传统上由机构储备支持不同,DAI 历来依赖于加密货币抵押资产,如ETH。然而,2022 年10 月,MakerDAO 开始将DAI 储备的很大一部分配置到美国国债和其他现实世界资产(RWAs)中,以捕获更高的收益。截至2023 年7 月,DAI 超过65% 的储备与RWAs 挂钩,使其收入对利率波动更为敏感。这一转变使DAI 的行为与机构稳定币更为接近,直接从利率上升中获益。

正如预期的那样,DAI 储备组成的变化导致了利率与SKY 稳定币每单位供应收入之间的强正相关关系(R = 0.937)。数据证实,较高的利率有助于增加收入生成,进一步印证了SKY 稳定币现在的表现类似于收益优化的机构稳定币。

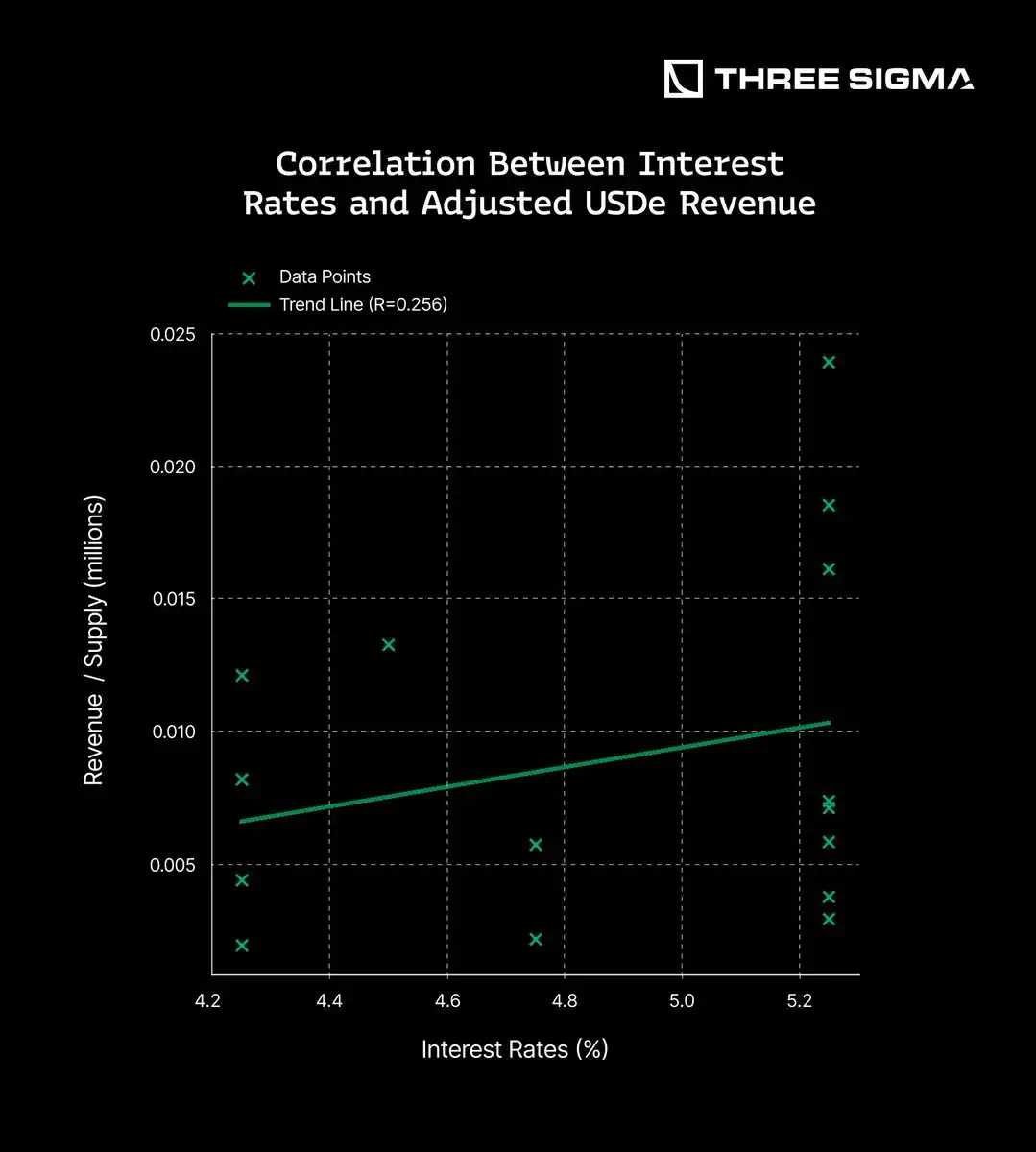

USDe

USDe 的收入模型主要基于永续期货市场中的资金费率套利,而非像美国国债这样的传统带息资产。正如我们所见,其对冲策略涉及在永续期货中持有空头头寸,通过在未平仓合约中出现不平衡时从多头交易者支付的费用中获利。

当多头头寸的需求增加时,资金费率上升,使得持有多头头寸变得更加昂贵,同时为空头交易者(包括USDe)提供了收益机会。然而,这种收入模型不太直接受到传统利率变化的影响,而是更多依赖于市场波动性、交易者的头寸和加密市场的整体杠杆需求。

趋势线显示出较弱的正相关关系(R = 0.256),表明尽管较高的利率可能对USDe 的收入产生一定影响,但这种关系并不是特别强。

这与预期一致,因为USDe 的收入模型主要由永续期货市场的状况驱动,而非利率变动。资金费率和杠杆需求在收入生成中的作用远大于传统的利率上调。

这一相关性突显了USDe 的收益依赖于交易者行为,而非直接暴露于现实世界的利率变化。尽管较低的利率可能鼓励加密市场中的更大风险承担和杠杆使用,USDe 的盈利能力仍然与永续期货交易中的资金费率不平衡密切相关。

5. 利率降至0% 的影响

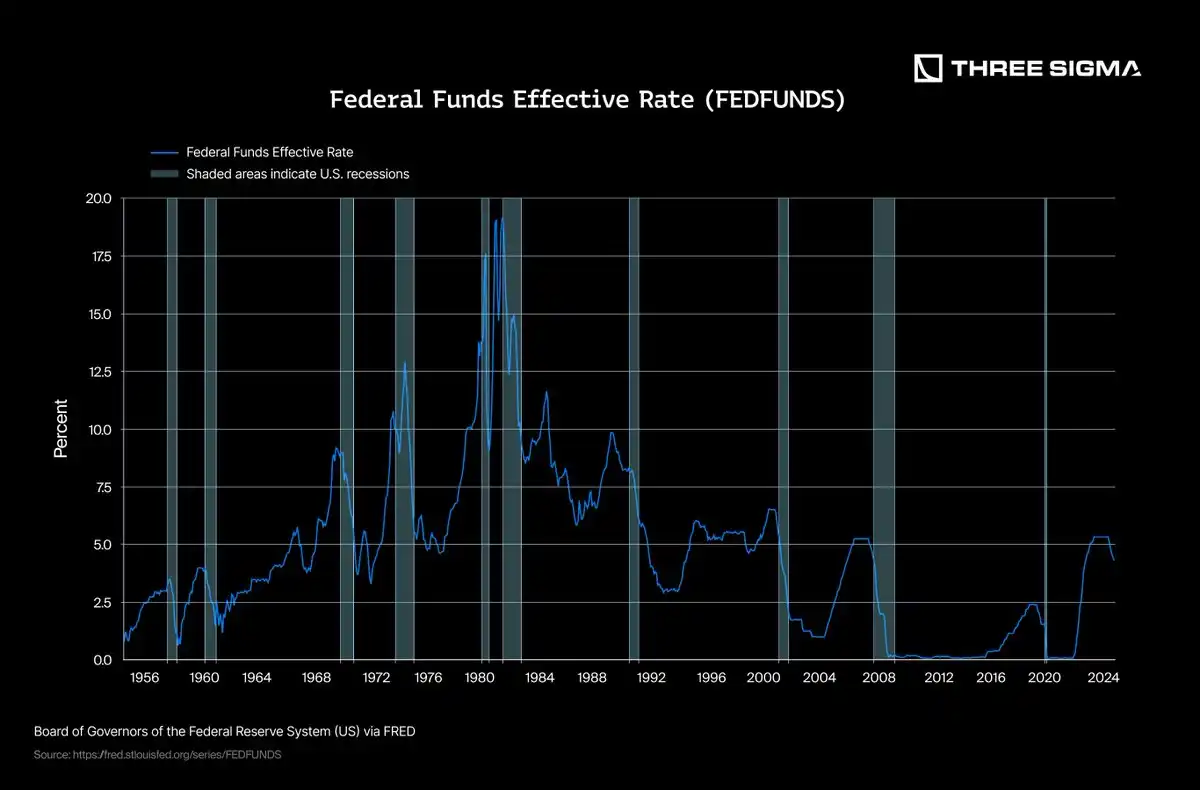

interest rate

利率代表借款的成本,或者反过来,代表借出或存入资金所获得的回报。中央银行,如美国联邦储备系统,设定基准利率(例如联邦基金利率)以管理经济增长、控制通货膨胀和稳定金融系统。较低的利率通常会鼓励借款,刺激经济活动,但也可能助长通货膨胀。

相反,较高的利率会抑制借款,减缓经济扩张,但有助于抑制通货膨胀压力。历史上,利率会根据经济周期和危机波动剧烈,通常在经济衰退期间(例如2008 年金融危机、COVID-19 大流行)接近零,而在通货膨胀时期(例如疫情后2022-2024 年)则会大幅上升。利率波动直接影响国库券(T-Bills)和债券的收益率,这对依赖这些投资回报的稳定币发行者至关重要。

历史利率

最需要关注的利率是美国联邦储备系统设定的利率,特别是联邦基金利率,因为美元作为主要储备货币的全球主导地位以及其对国际金融市场的广泛影响。美国利率的变化对全球经济活动、货币估值、投资流动和借款成本产生重大影响,因此成为全球金融稳定性的重要基准。

历史图表清晰地展示了几个主要的利率周期,包括1980 年代初期为应对通胀而创下的历史高利率,随后利率稳步下降,进入过去二十年的低利率环境。2008 年金融危机尤其迫使利率接近零,以刺激经济复苏。

具体来说,在上一轮利率周期(2010-2020 年),美联储将利率保持在历史低位(接近0%)长达一段时间,直到2015 至2018 年经济逐步复苏时才开始逐步上调。然而,2020 年初COVID-19 大流行的爆发再次促使利率大幅下调至接近零水平,旨在应对经济放缓,确保流动性,并稳定金融市场。

利率与收入的相关性比较

正如我们之前讨论的,某些稳定币的收入模型高度依赖于利率,而其他则有结构将其与这些波动隔离。

提供的数据清晰地证明了这一区别。USDT、USDC 和SKY 的相关性都很高(R ~0.89–0.94),这突显了它们对现行利率的显著依赖。它们的收入主要来源于传统投资,如国债,使得它们在利率接近零的情况下面临较大的风险,这会严重影响其盈利能力。

与之形成鲜明对比的是USDe,其相关性明显较弱(R = 0.256),反映了其完全不同的收入生成方式。USDe 的收入主要来源于加密市场的机制,如永续期货资金费率套利和质押收益,而非传统的、受利率影响的资产。

总之,这些数据强烈表明,法币支持和国债支持的稳定币(如USDT、USDC 和SKY)在低利率环境下面临相当大的风险。相反,像USDe 这样的算法稳定币,凭借其替代性的收入策略,展示了更强的韧性,并且可能在利率下降时成为投资组合中的战略性分散工具,提供相对的稳定性.

利率降至0% 的情景

在利率回到0% 的情景下,稳定币的影响差异显著,这取决于它们的收入模型和资产配置:

Tether

由于USDT 主要通过传统的金融资产(如国库券)产生收入,利率降至0% 将极大地减少其收入来源,严重影响盈利能力。然而,Tether 在替代投资上的战略性多元化,包括加密货币(BTC、ETH)和贵金属,可能会部分缓解这种影响。然而,这些替代资产带来了更高的波动性和风险,可能无法完全弥补丧失的利息收入,从而可能削弱其整体市场地位。

2024 年,Tether 维持了非常低的运营费用,得益于50 名以下员工的精简结构、最小的行政开销以及自USDT 代币的交易费用普遍涵盖了这些事务性费用。法律和监管费用也相对较低,今年没有重大罚款,相比之下,2021 年曾向纽约总检察长支付了1850 万美元的罚款。

财务方面,Tether 在2024 年结束时保持了强劲的储备,超出USDT 持有者义务的储备约为71 亿美元,总股本约为200 亿美元。鉴于其保守的年度运营费用(可能低于1 亿美元),即使未来收入完全归零,Tether 也能维持运营超过70 年,显示出其卓越的财务稳定性和几乎无限的运营空间。

Circle

Circle 最近向美国证券交易委员会提交了S-1 注册声明,表示计划在纽约证券交易所上市,股票代码为「CRCL」。

2024 年,Circle 报告的总收入约为16.8 亿美元,比2023 年的14.5 亿美元增长了16%。值得注意的是,这些收入中超过99% 来自储备收入,主要是从支持USDC 的资产上赚取的利息。2024 年,公司的净收入约为1.56 亿美元,较前一年的2.68 亿美元大幅下降,这主要是由于运营和分销费用增加。

2024 年的运营费用总额约为4.92 亿美元,其中大部分用于员工薪酬(2.63 亿美元)、一般行政费用(1.37 亿美元)、IT 基础设施(2700 万美元)、折旧和摊销(约5100 万美元)、营销费用(1700 万美元)以及数字资产损失(400 万美元)。此外,Circle 还承担了约10.1 亿美元的分销和交易成本,其中约9.08 亿美元支付给了主要分销合作伙伴Coinbase。

截至2024 年12 月31 日,Circle 持有7.51 亿美元的现金和现金等价物,另有2.94 亿美元的其他流动性投资,总可用流动性约为10.45 亿美元。在估算公司在零收入情景下的财务可持续性时,重要的是区分这两类资产:

7.51 亿美元的现金和现金等价物代表了高流动性、可立即使用的资金——适合进行保守的财务可持续性估算。仅基于此,并假设当前的年度运营费用为4.92 亿美元,Circle 的财务可持续期约为18 个月。

如果包括全部10.45 亿美元的流动性(现金和其他流动资产),并假设这些额外资产可以随时使用且没有限制,那么财务可持续期可以延长到约25 个月。

更保守的方法仅关注现金等价物,以避免依赖可能流动性较差或受限的资产。然而,如果Circle 能够毫无问题地利用更广泛的流动性池,它将拥有更大的灵活性。

在长期零利率环境下,Circle 对来自储备的利息收入的高度依赖可能会显著影响其收入来源。如果未能有效多元化收入来源,公司的盈利能力可能会受到不利影响,可能需要进行战略性调整,例如修改费用结构或探索新的投资途径。

SKY 在0% 的利率环境下,Sky 协议(前身为MakerDAO)确实面临着重大挑战,尤其是在其收入来源和财务可持续性方面。该协议依赖于美国国债、ETH 质押奖励和DeFi 收入,这意味着完全没有利息可能会大大影响其收入。

收入来源面临压力:

稳定性费用和借贷需求:随着借贷需求减少,DAI 贷款的稳定性费用可能会下降。此下降再加上美国国债和其他债券的收益减少,可能会加剧协议的财务压力。

DeFi 资金费用:在低利率环境下,交易者可能不太愿意进行杠杆操作,这将导致DeFi 活动的资金费用减少。

历史上,Sky 协议已经通过调整像Sky 储蓄利率(SSR)等参数,表现出了对低利率环境的适应能力。例如,SSR 最近被下调至4.5%,从2025 年3 月24 日起生效,以与当前市场条件对接。

Sky 协议的总资产价值约为2.2 亿美元,包含以下内容:

1.01 亿美元的DAI – 稳定

8220 万美元的SKY 代币– 波动

3640 万美元的MKR 代币– 波动

24.3 万美元的stkAAVE – 波动

47 万美元的ENS – 波动

这2.2 亿美元的总价值结合了DAI 等流动性资产和SKY、MKR 等波动代币,后者的价值可能会根据市场条件波动。流动性资产是协议运营最易用的资金来源,而波动代币则是更具战略性的资产类别,受市场波动影响。

运营周期是Sky 协议在不产生新收入的情况下,基于当前资产和年度运营支出的时间长度。协议的年运营支出估计为3500 万美元。 The calculation formula is as follows:

如果只考虑流动性资产(DAI):运营周期= 1.01 亿美元÷ 3500 万美元= 2.89 年

如果考虑当前价格下的总资产(流动性+波动资产):运营周期= 2.2 亿美元÷ 3500 万美元= 6.29 年

在0% 利率的情况下,Sky 协议的财务可持续性主要依赖于SKY 和MKR 等波动性资产的价值,这些资产的波动可能会影响总的运营周期。然而,仅根据DAI 系统的盈余,Sky 协议可以在不产生额外收入的情况下维持约2.89 年的运营。如果考虑整个资产池(包括流动性和波动性资产),Sky 可以大约维持6.29 年的运营,假设市场没有其他重大变化。

作为一个历史上展现出适应能力的协议,Sky 协议可以调整费用结构,并在资产配置上做出战略性调整,以应对长期低利率环境。

Ethena 如果美联储将利率降至0%,几个因素可能会影响USDe 保持和增加收益的能力。较低的利率降低了借贷成本,使得杠杆操作对交易者和投资者更具吸引力。在传统市场中,这通常会推动资本流入风险较高的资产,因为固定收益工具的回报减少,促使投资者寻求其他地方的更高回报。这个动态同样适用于加密市场,较低的利率环境通常会导致资本流入比特币和以太坊等加密货币。

随着更多流动性进入市场,交易者更倾向于在加密资产上采取杠杆多头头寸,期待价格继续上涨。这在永续合约市场中创造了不平衡,多头需求超过空头需求。因此,资金费率上升,使得持有多头头寸的成本更高,而做空的交易者则受益,例如USDe 策略所采用的方式。

然而,这种好处并非没有潜在风险。如果利率长期维持在低位,USDe 的收益可能最终稳定下来,甚至下降,因为市场参与者会调整策略以适应新的常态。这种调整可能表现为减少杠杆或改变交易策略。此外,虽然低利率环境最初通过永续合约资金费率支持USDe 的收益生成,但这些条件的长期稳定可能会激励投资者行为的转变,转向当前产生最高收益的资产以外的其他资产。

从协议层面来看,Ethena 在财务上处于有利位置。该项目已通过风险投资和代币销售筹集了超过1.2 亿美元,并维持着一个约6100 万美元的储备基金,可以通过链上钱包0x2b5ab59163a6e93b4486f6055d33ca4a115dd4d5 验证。这个储备基金在负收益环境下充当缓冲,支持USDe 的稳定性。Ethena 还采用精简的团队,估计年运营费用为200 万至500 万美元,即使协议收入显著缩水,项目也能维持多年运营。

总之,虽然低利率环境为USDe 在短期内保持吸引力提供了独特的机会,但其长期可持续性依赖于市场活动和波动性的持续性。尽管如此,Ethena 强大的储备金位置和低燃烧率为其提供了坚实的财务缓冲,确保协议能够在长期低收益期内稳定运营,而不会影响其核心稳定性。

6. Conclusion

稳定币的生态系统与宏观经济动态,特别是利率密切相关。正如本分析所示,在利率降至0% 的情境下,各种稳定币模型的表现和可持续性存在显著差异。

最受影响的:

USDC

几乎完全依赖于美国国债的收益,在没有有效分散化的情况下,其商业模式在长期低利率环境中变得结构脆弱。高运营成本和相对有限的财库储备进一步限制了Circle

的长期运营能力。

显著受影响但更具韧性:

USDT 和SKY

也会面临可观的收入压缩,因为它们依赖于有息资产。然而,它们都具备一定的缓冲。Tether(USDT)持有大量财库盈余,运营成本极低,并且部分投资于多样化资产(例如比特币、黄金),使其在零利率条件下拥有更长的财务运作期。

SKY(USDS/DAI)同样面临收益下降的风险。然而,它通过DeFi 原生机制(如协议费用、加密货币抵押品清算和智能合约借贷)保持了多元的收入来源,从而提供了更大的运营灵活性。此外,协议还可以依靠治理代币销售来覆盖费用,正如过去周期所证明的那样。

影响最小/最具适应性:

Ethena(USDe)凭借其以市场驱动的加密原生收入模型脱颖而出,不依赖有息工具。相反,Ethena

通过永续期货资金费率、质押奖励和市场低效捕捉价值。在0% 利率的世界里,USDe

甚至可能因杠杆和投机增加而受益,使其成为少数能够在其他稳定币收缩时蓬勃发展的项目之一。

然而,从长远来看,持续的低利率环境可能导致市场条件转为中性或看跌,可能会减少Ethena 的盈利能力。事实上,当资金费率对空头变得强烈负面时,协议甚至可能面临短期损失。

这项对比分析强调了一个关键洞察:收入多元化不再是可选的,而是至关重要的。在利率可能回到历史低位的世界里,过度依赖传统金融工具的稳定币发行人面临显著的盈利下降风险。那些拥有灵活加密原生收入引擎的协议,特别是像USDe 这样的协议,可能不仅能够渡过难关,甚至能变得更强大。

最终,稳定币市场的可持续性将不仅仅由挂钩稳定性或市场接受度决定,更取决于跨经济体制的韧性。那些通过产品创新、多元化抵押物或收益机制进行适应的协议,将定义下一代数字美元。

最后值得指出的是,Circle 和Tether 可能已经在为一个低利率收益的世界做准备。它们每一个都在积极构建或参与自己的区块链基础设施:Circle 正在建设Cortex,Tether 则有Plasma。这些努力似乎旨在多元化其服务提供,并可能开辟超越财库收益的新收入来源。

此外,Circle 的IPO 宣布恰逢我们研究结束时。公开的细节与我们识别的脆弱点和战略方向高度契合,特别是需要通过新事业实现多元化和扩展。IPO 可能既是一次流动性事件,也可能是向更侧重服务和基础设施的商业模式转型的标志。

最后,不禁让人猜测,Circle 是否还藏有一张王牌?它是否悄悄地在为成为数字美元的官方发行方做准备?虽然没有正式公告确认这一点,但这样的举措肯定符合其以监管为先的策略和与美国的合作伙伴关系。谁知道呢。

Web3 成功的秘诀只需一步之遥——不要让别人领先,让你还在迷茫中徘徊。

panewslab

panewslab